SHANGHAI, Jul 14 (SMM) – China has taken a leading position in global new energy industry despite source starvation; mining and battery sectors are highly concentrated in the global new energy value chain, while smelters and material producers, who are in the middle of the value chain, are less concentrated and suffer from thin gross profits and overcapacity, said Racket Hu, vice president of SMM.

Speaking at the 5th China International Nickel Cobalt Lithium Summit in Ningbo, Zhejiang province on July 13, Hu explained the opportunities and challenges facing China's new energy industry, and expected that grim consequences from extensive growth will trigger a shift to more prudent investment.

China became a big producer of smelting products and battery material after rapid capacity expansion, but capacity utilisation ratio has been below overseas levels for an extended period, Hu cited SMM surveyed data.

Extensive growth has also led to heavy capital investment but low return, a rich variety of products but of weak technical structure.

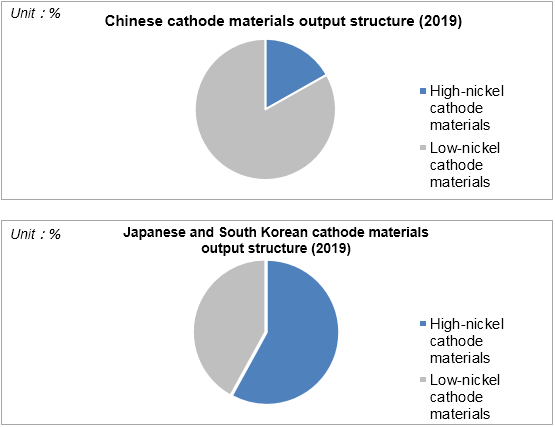

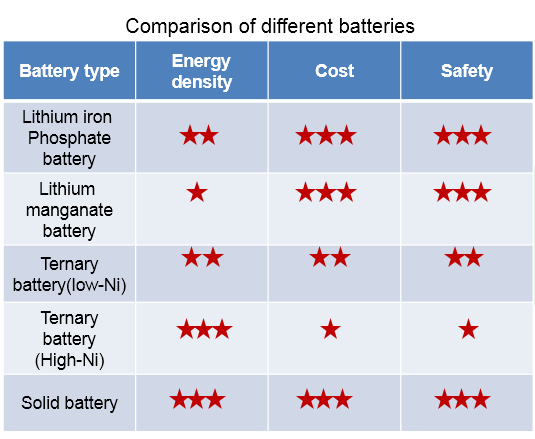

Although China has rich varieties of cathode materials, the proportion of high-nickel materials with higher technical barriers is still far lower than that of Japan and South Korea, said Hu.

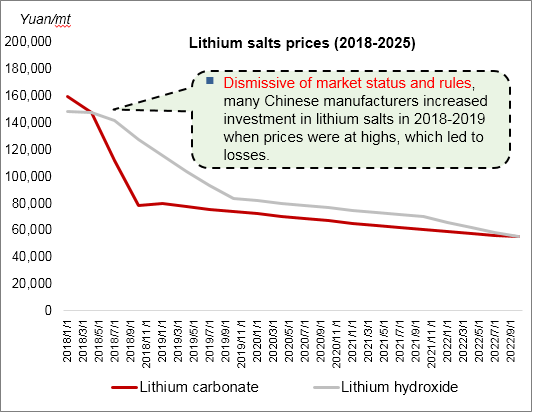

Some enterprises ignored rules of market development, investing blindly to expand production, and economic losses were caused as a result.

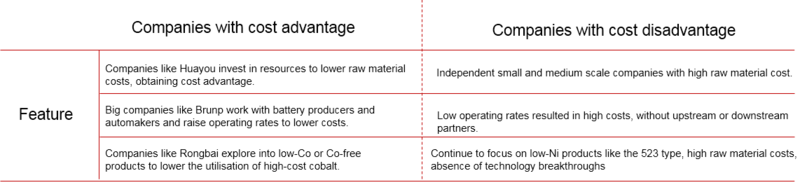

Hu suggested that companies can enhance their competitiveness through cost advantages and technology-driven development, so as to take advantage of the opportunity to win the future.

To be specific, companies can lower cash costs by investing in raw materials and expanding scale.

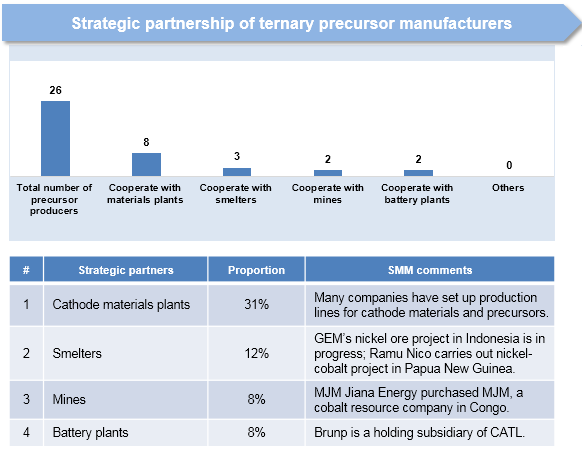

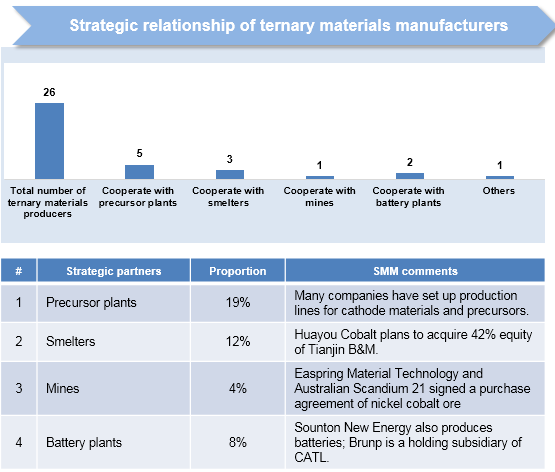

Manufacturers of ternary materials and precursors prefer to partner with enterprises in the industry chain to enhance competitiveness.

Hu believed that future competition will not be between enterprises but between value chains.

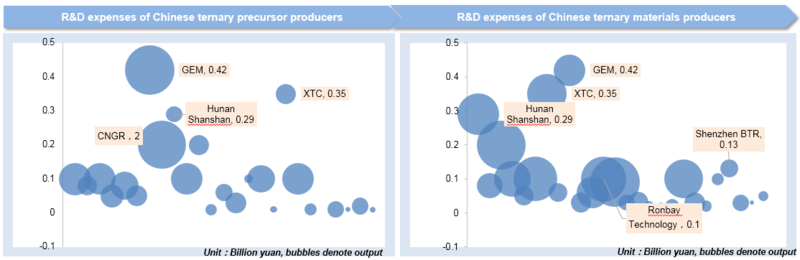

The research and development funds are an important guarantee for long-term operation of materials plants. Ternary precursor and materials plants usually use 3-6% of their revenues as R&D expenses.

Generally, output is directly proportional to R&D funds. Among precursor producers, GEM has invested the most in research and development and has the largest output. XTC and Hunan Shanshan have relatively high R&D funds but lower output as precursor is not their main product.

The research and development cost of ternary materials is slightly higher than that of precursors. GEM, XTC and Hunan Shanshan have the largest investment in research and development, and they have at least two cathode material products.

Ronbay Technology and BTR are two typical enterprises focusing on high-nickel ternary materials, and their R&D costs are similar.

According to incomplete statistics, the total capacity of future projects at European lithium battery plants will reach nearly 500 Gwh, most of which will be commissioned during 2020-2025.