SMM7: at the "2020 (Fifth) China International Nickel-Cobalt-Lithium Summit Forum" and China International New Energy Lithium Materials Conference held by SMM, Liu Yanlong, secretary-general of China Chemical and physical Power Industry Association, analyzed the development status of lithium-ion battery industry in 2019 and looked forward to the development trend of lithium-ion battery market in 2020.

Development status of Lithium Ion Battery Industry in 2019

Lithium ion battery

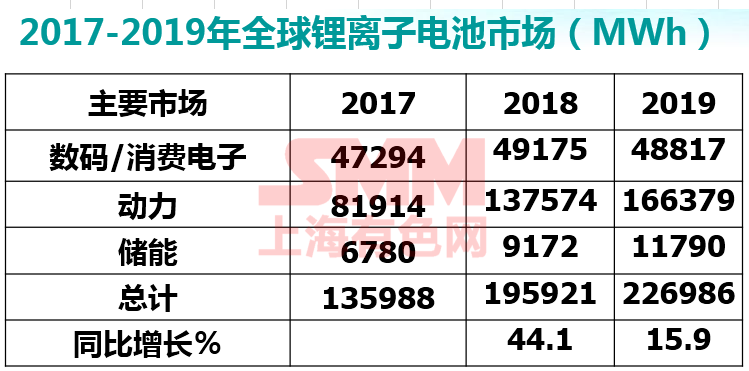

Liu Yanlong said that global lithium-ion batteries are mainly produced by Chinese, Japanese and South Korean companies, accounting for more than 95% of global demand. Lithium-ion batteries are mainly used in areas such as digital consumer electronics, new energy vehicles and energy storage. The digital market mainly includes mobile phones, notebook computers, tablet computers, wearable devices, mobile power sources, etc.; the power market mainly refers to electric passenger cars, electric buses, electric bicycles, power tools and so on; energy storage market mainly refers to new energy storage, communication base station energy storage, industrial and commercial energy storage, household energy storage and so on. In 2017, digital accounts for 34.8%; power accounts for 60.2%; and energy storage accounts for 5%. In 2019, digital accounts for 21.5%; power accounts for 73.3%; and energy storage accounts for 5.2%.

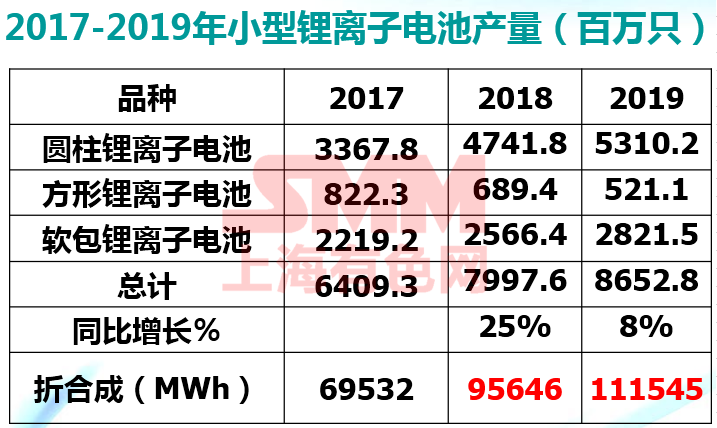

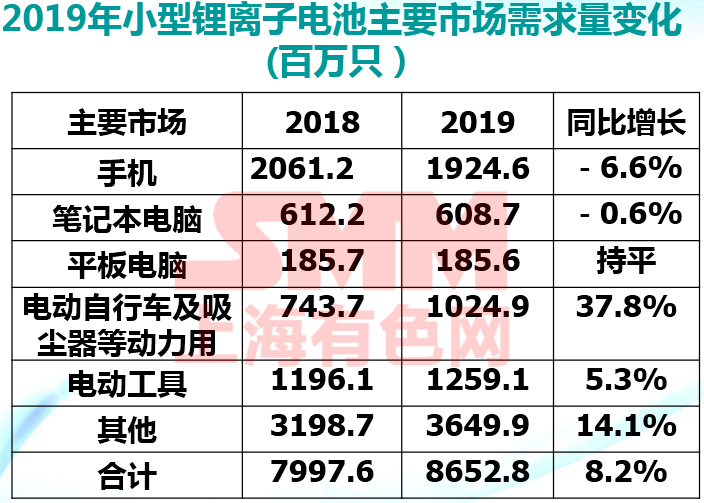

Small lithium-ion batteries mainly refer to cylindrical lithium-ion batteries, small square batteries and small soft-package batteries, which are mainly used in mobile phones, notebook computers, tablet computers, wearable devices, mobile power supplies, power tools, vacuum cleaners, household energy storage and electric vehicles. The market for small lithium-ion batteries grew by 8% in 2019 compared with the same period last year. Among them, lithium-ion batteries for mobile phones decreased by 6.6%, the top five mobile phone manufacturers were Samsung, Huawei, Apple, Xiaomi and Oppo, soft package batteries accounted for 84.9%, square batteries accounted for 15.1%. Lithium-ion batteries for notebooks fell slightly by 0.6%. The top five manufacturers were Hewlett-Packard, Lenovo, Dell, Apple and Acer;, accounting for 75.3%, square batteries and cylindrical batteries accounting for 17% and 7.7%, respectively. Lithium-ion batteries for tablets are the same as in 2018, with the top five manufacturers Apple, Samsung, Microsoft, Lenovo and Amazon; accounting for 98.2 per cent of soft package batteries, 1.6 per cent of square batteries and 0.2 per cent of cylindrical batteries.

Power lithium-ion batteries such as electric bicycles, vacuum cleaners and e-cigarettes increased by 37.8%. Among them, there are 629.5 million lithium-ion batteries for electric bicycles, with the top three international brands of electric bicycles Bosch, Yamada and Panasonic accounting for 23.7% and Chinese brands accounting for 42.4%. There are 294.5 million lithium-ion batteries for vacuum cleaners, of which the main brands are Dyson and Electrolux account for 42%. There are 100.9 million lithium-ion batteries for e-cigarettes, of which the main brands are Philip Morris, BAT and JT, accounting for 89.5%.

Lithium-ion batteries for power tools and garden tools increased by 5.3%, all of which were cylindrical lithium-ion batteries. Of these, 1.1669 billion lithium-ion batteries were used for power tools, an increase of 6 per cent over the same period last year. The top five power tool brands are Stanley Black & Decker, TTI, Makita, Bosch and Hilti. The number of lithium-ion batteries used for garden tools was 92.2 million, down 8% from the same period last year. The main brands are Stihl and Husqvarna.

Lithium-ion batteries for other uses increased by 14.1%. It mainly includes lithium-ion batteries for electric vehicles (main TESLA)-60%, household energy storage-5.5%, mobile power supply-4.7%, game consoles-2.3%, UPS-1.4%, electric razors / electric toothbrushes-1.3% and so on. Cylindrical batteries account for 79.5%, soft package batteries account for 18.1%, and square batteries account for 2.7%.

New energy vehicle

Global sales of new energy vehicles (including HEV) were about 4.358 million in 2019, an increase of 7.2 per cent over the same period last year. Of this total, EV and PHEV sold 2.21 million vehicles, up 10 per cent from a year earlier. The global market penetration of new energy passenger vehicles (EV and PHEV) increased from 2.1 per cent in 2018 to 2.5 per cent in 2019. China has become the world's largest market for new energy vehicles for five years in a row. From the perspective of monthly sales, since September, global sales of new energy vehicles have shown a downward trend of "four consecutive declines".

According to the statistical certificate data of our power battery application branch, the output of new energy vehicles in China totaled 1.176 million in 2019, down 3.5% from the same period last year. From the performance of new energy vehicles in 2019, the phenomenon of subsidy dependence is more obvious. Since the end of the transition period of the new subsidy policy in June, the output of new energy vehicles showed a downward trend of "six consecutive declines" in the second half of the year. According to Shanghai Insurance, sales of new energy vehicles totaled 955000 in 2019, down 9.1 per cent from a year earlier.

From the perspective of segment, the sales of new energy passenger vehicles accounted for 88.0% of the total sales of new energy vehicles in 2019, and decreased by 6.1% compared with the same period last year, which is lower than the overall market level.

As for fuel cell vehicles, sales of passenger cars and special-purpose vehicles both achieved rapid growth, up 207.0% and 368.4% respectively over the same period last year.

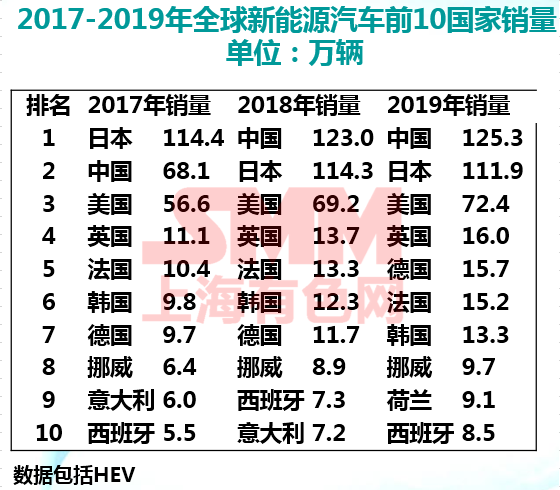

From the perspective of the national region, China still tops the list in 2019, with sales of 1.253 million vehicles. Among the top ten countries, except China, Japan, the United States and South Korea, all are European countries.

From the perspective of model route, at present, China, the United States, Europe and other models are basically focused on the routes of EV, PHEV and FCV. In addition, China, Norway, the Netherlands and other EV models accounted for more than 60% of sales. 、

From the technical route, at present, China, the United States, Europe and other car companies basically focus on the EV, PHEV route. Japanese car companies mainly gather HEV.

Installed capacity of lithium-ion battery

According to the statistics of China Chemical and physical Power Industry Association, the installed capacity of global power lithium-ion battery is 112.6GWh in 2019. Among them, the installed capacity of five power battery enterprises in Japan and South Korea is 50.4 GWH, accounting for 44.8%. The installed capacity of Chinese enterprises is 62.2 GWH, accounting for 55.2%. The top 10 Chinese enterprises have installed 54.65GWh.

In 2019, there were 79 power battery enterprises for new energy vehicles in China, 13 fewer than in 2018, and the installed capacity of power batteries was 62.2 GWH, an increase of 9.3% over the same period last year. Power battery industry reshuffle further intensified. Compared with the top 10 in 2018, Beijing National Energy and Carney New Energy fell out of the top 10, while the other eight power battery companies remained stable in the top 10, while SAIC and Xin Wanda entered the top 10, and the head competition pattern was relatively stable.

In terms of battery types, the installed capacity of ternary batteries in 2019 was 40.5GWh, accounting for 65.2 percent, an increase of nearly 7 percentage points over 2018; lithium iron phosphate batteries installed 20.8GWhs, accounting for 33.4 percent, down nearly 6 percent from 2018; and the installed capacity of other battery types was 0.9GWh, accounting for 1.4 percent.

98% of the ternary batteries are equipped on passenger cars with an installed capacity of 39.6GWh. Lithium iron phosphate and lithium manganate are mainly equipped with passenger cars, with installed capacity of 13.8GWh and 0.4GWhh respectively, accounting for 66% and 78% of their respective installed capacity respectively.

Characteristics of power battery industry: significant improvement in market concentration

Since 2016, the power lithium-ion battery industry has experienced structural overcapacity. With the deep adjustment of national policy, the concentration of power battery industry will continue to increase.

The installed capacity of the top 20 enterprises in 2016 was 83.1%, and the installed capacity of the top five enterprises accounted for 64.5%.

In 2017, the top 20 enterprises installed 32.09 billion WH, accounted for 87%; the top five enterprises installed 22.343 billion WH, accounted for 60.5%.

In 2018, the top 20 enterprises installed 52.23 billion WH, accounting for 91.8%; the top five enterprises accounted for 73.6% of the installed capacity. The top two accounted for 61.3%.

The installed capacity of 59.482 billion WH, in the first 20 enterprises accounted for 95.7% in 2019; the installed capacity of the top five enterprises accounted for 79.6%, and the first two accounted for 68.3%.

In 2019, various enterprises are facing multiple pressures such as a sharp decline in subsidies, an increase in energy density and the lower threshold of battery life, and a tight capital chain. The market has entered a stage of rapid reshuffle, and the degree of concentration has been further improved. Second-and third-tier echelon enterprises are facing greater financial pressure, and many enterprises have gradually given up the power battery business of new energy vehicles and turned to small power markets such as power tools and electric bicycles.

The safety of power battery should be paid great attention by enterprises.

The high nickel and low cobalt content of ternary cathode materials has obvious advantages in increasing battery energy density and reducing material cost, but the problems of safety and stability are more prominent. Due to the high technical barrier of high nickel ternary cathode materials, the requirements of preparation process, equipment and production environment are much higher than ordinary ternary materials, domestic high nickel ternary materials still need to overcome a number of technical problems.

According to incomplete statistics, there were at least 40 spontaneous combustion accidents of new energy vehicles in China in 2018. In 2019, a total of 33700 new energy vehicles were recalled in China, and 6520 vehicles were recalled because of the hidden danger of spontaneous combustion, accounting for 19.3% of the total recall, indicating that the current safety performance of new energy vehicles is not optimistic.

Both enterprises and relevant regulatory agencies must be highly vigilant against the safety accidents of new energy vehicles to prevent the butterfly effect and deal a fatal blow to the development of the industry.

The proportion of ternary power battery continues to increase.

From the perspective of market demand, passenger cars will be the main force for the growth of new energy vehicles in the future. Due to the guidance of subsidy policy and the high-density characteristics of ternary battery itself can better meet the needs of the new energy passenger car market, from the data of domestic mainstream battery manufacturers, ternary battery has become the focus of the development of battery technology. High nickel ternary material battery is generally favored by the industry, attracting the positive layout of many power battery enterprises. Ternary battery enterprises focus on the research and development of high-nickel ternary battery, and the technical route is advancing rapidly from NCM523 system to NCM622, NCM811 and NCA. The proportion of three yuan increased from 58.2% in 2018 to 65.2% in 2019.

The new subsidy policy introduced this year maintains the overall stability of the technical index system in accordance with the principles of advanced technology, reliable quality and guaranteed safety, and promotes enterprises to further improve the technical level, safety and reliability of their products. The threshold requirements for most technical indicators will remain unchanged in 2020, remain stable in principle from 2021 to 2022, and be appropriately adjusted according to technological progress and industrial development.

After the adjustment of subsidy policy in 2020, lithium iron phosphate battery, ternary battery and lithium manganate battery will have their own application fields and development space.

Subsidize the slope to urge the whole industry to reduce costs

The withdrawal of subsidies is an inevitable trend, but due to the large decline of subsidies in 2019, the sales of new energy vehicles have declined. In order to promote automobile consumption, the executive meeting of the State Council on March 31 decided to extend the subsidy policy for the purchase of new energy vehicles due at the end of this year for two years.

The cost pressure caused by the gradual withdrawal of subsidies will be transmitted to the upper reaches of the power battery industry chain. battery enterprises need to deal with it in many dimensions, such as technology product development and transformation, supply chain management, cash flow control and so on. Some poorly managed enterprises will break their capital chains and be forced to withdraw from the market or be merged.

The willingness of power battery enterprises to reduce costs in the short term is very strong, and they will "reduce costs" by pressing prices to upstream diaphragms, electrolytes, negative electrodes, positive electrodes, and other "cost reduction" measures, as well as increase energy density, standardization, large-scale production and other "efficiency" measures to make up as much as possible. Enterprises with specific cost advantages and quality advantages will win in the competition!

Development trend of Lithium Ion Battery Market in 2020

Power and energy storage are the main markets for the growth of lithium-ion batteries.

In the next few years, the market for traditional applications of lithium-ion batteries such as mobile phones, laptops and tablets will remain stable, with overall single-digit growth. The new energy vehicles, electric bicycles, power tools and other power markets and energy storage for various uses will be the fastest growing market for lithium-ion batteries, mainly depending on the demand of the Chinese and European markets, with an average annual growth rate of double digits.

The new crown epidemic that spread around the world this year will have a certain impact on the global lithium-ion battery market in the short term: first, it has a huge impact on the supply chain of battery production and major application markets, and second, it has an obvious suppressing effect on consumer demand. Travel blockades and surging unemployment across countries have reduced consumer confidence, leading to a reconsideration of spending priorities for basic goods, which has a direct impact on sales in different markets for lithium-ion batteries.

Because of the new crown epidemic, more people stay in Canada, more students take online classes or less commuters take public transport, demand for tablets, laptops and electric bicycles will increase, and demand for power tools and garden tools will decrease.

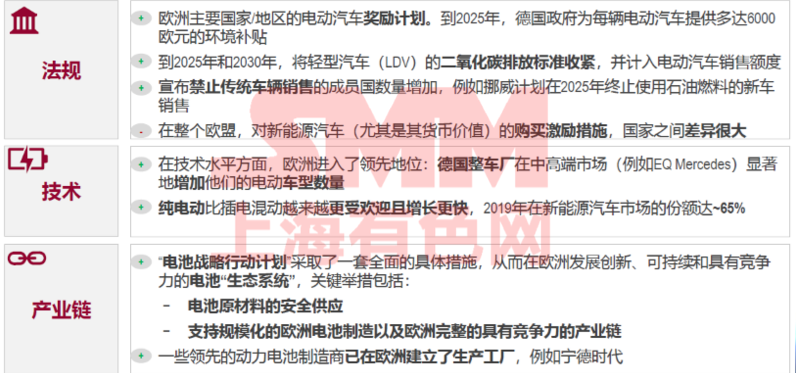

Stringent emission standards in Europe will speed up the electrification of car companies

As Europe pays attention to global warming, it promotes the transformation from traditional European vehicles to new energy vehicles. European countries have introduced and increased subsidies for the purchase and use of new energy vehicles, which has promoted the development of European new energy vehicle market. On December 11, 2019, the European Commission announced the European Green Agreement on climate change in Brussels, proposing that Europe will take the lead in achieving "carbon neutralization" in the world by 2050, that is, net carbon dioxide emissions will be reduced to zero. Only Volvo, Toyota and Renault-Nissan meet the new CO2 emission standards of 95g/km to be implemented by the European Union in 2021, which will make many car companies face huge fines, and electrification will be the best solution to meet the requirements.

Development trend of European Electric vehicle Market

The development of electric vehicles in Europe is positively affected by government regulations. The goal of the EU government is to increase the sales of electric vehicles and establish a battery industry chain. Sales of new energy vehicles in Europe reached 564200 in 2019, up 38.6% from 407000 in 2018. The outlook for the European new energy vehicle market is encouraging, but it may also be affected by the coronavirus. BNEF expects sales of new energy vehicles in Europe to grow by 50% in 2020, with more than 800000 vehicles.

Various New policies in China will accelerate the Promotion of New Energy vehicles

1. A few days ago, the equipment Industry Department of the Ministry of Industry and Information Technology issued the "New Energy vehicle Industry Development Plan (2021-2035)" (draft for soliciting opinions). As a programmatic policy for the new energy vehicle industry, the plan points out the direction for the development of China's new energy vehicles in the next 15 years.

The plan points out that after 15 years of continuous efforts, the key core technologies of new energy vehicles have made major breakthroughs, integrated development is coordinated and efficient, pure electric vehicles have become the mainstream, fuel cell commercial vehicles have been applied on a large scale, and highly self-driving intelligent network-connected vehicles are becoming more and more popular, and China has entered the automotive industry of a powerful country in the world.

By 2025, the competitiveness of new energy vehicles will be significantly improved, with sales accounting for 20% of the total car sales in that year. The average fuel consumption of new passenger cars will be reduced to 4.0L big 100km, and the average power consumption of new passenger vehicles will be reduced to 11.0kWh/100km.

By 2030, new energy vehicles will form a competitive advantage in the market, with sales accounting for 40% of the total car sales in that year, and the energy consumption of new cars will reach the highest level in the world.

Affected by the new crown epidemic and the decline of subsidies, China's new energy vehicle sales in 2020 are expected to be 5% lower than in 2019, with a minimum of 1 million vehicles.

2. The revised policy of "parallel Management measures for average fuel consumption of passenger vehicle Enterprises and points for New Energy vehicles" issued by five ministries and commissions on June 15, 2020 defines the integral proportion requirements for new energy vehicles from 2021 to 2023, which are 14%, 16% and 18%, respectively.

According to the requirements of this ratio, it can basically guarantee the realization of the planning goal of "by 2025, the average fuel consumption of new passenger cars will reach 100 km and 4 litres, and the proportion of production and sales of new energy vehicles will reach 20% of the total number of vehicles."

The introduction of the double points policy will promote overseas (especially European) traditional car companies to step up the layout of electric vehicles in China, the contest between joint ventures and independence will be staged again in the field of electric vehicles, and domestic core parts suppliers will usher in historic opportunities for development. The double-point policy is a "double-edged sword", which will effectively promote the expansion of the total scale of new energy vehicles, but the market space of independent brands of new energy vehicles will be greatly compressed. The greater the implementation of the double points policy, the greater the degree of space compression for independent brands.

The global smartphone market may plummet and Chinese manufacturers' market share expands.

According to IDC's recent forecast, consumer spending will fall as a result of the new crown pneumonia epidemic, and global smartphone shipments are expected to fall nearly 12% year-on-year to 1.2 billion units in 2020. The travel blockade and the surge in unemployment have reduced consumer confidence and become the main factors affecting sales.

The 5G replacement trend will be the catalyst for the recovery of smartphone sales, playing a vital role in the recovery of the global smartphone market in 2021, and sales growth is expected to resume in the first quarter of 2021.

At present, China is the world's largest smartphone market, the Chinese economy has restarted, and factories have basically returned to normal production, so IDC expects only a single-digit decline in smartphone shipments in China in 2020. The market for Chinese mobile phone brands will continue to expand.

The demand of electrochemical energy storage burst for lithium-ion battery expands rapidly.

In the rising energy Internet, due to a large number of access of renewable energy and distributed energy in the large power grid, combined with the widespread application of microgrid and electric vehicles, electrochemical energy storage technology will be a vital link to coordinate these applications. Energy storage link will become the key node of the whole energy Internet, and the rise of energy Internet will significantly stimulate the demand for energy storage.

With the promotion of the reform of the global energy structure, on the power side, industrial and commercial energy storage, household energy storage and other application scenarios gradually mature; on the generation side, the rapid progress of wind power, photovoltaic and other renewable energy technology, the cost is reduced, the economy of power generation is significantly improved, and the installed capacity of renewable energy is growing rapidly. With the continuous decline of the cost of lithium-ion battery, gradually approaching the economic inflection point of the application of energy storage system, the energy storage market has great potential for future development.

In the next three years, the market for lithium-ion batteries for energy storage will grow at an average annual rate of 30%.

There is a huge demand for lithium-ion batteries in communication base stations.

With the gradual rise of 5G network in the world, it is expected that the construction speed of communication towers will be faster from 2020 to 2025. By 2025, the number of communication towers is expected to increase to 13 million, basically achieving 5G network coverage in major cities around the world. It is expected that the global market demand for lithium-ion batteries in base stations will reach 60GWh in 2025.

In the first half of 2020, the collection of 5G base stations announced by China's three major operators involved a total of 520000 5G base stations: 270000 by China Mobile, and 250000 by China Telecom and China Unicom. Strive to reach 600000 5G base stations by the end of 2020. Under the guidance of the general direction of the new infrastructure, provincial and municipal local governments have announced local 5G construction plans, which will build a total of 800000 in 2020.

The battery technology of various hybrid vehicles should be paid attention to after the subsidy is cancelled in 2020.

With the rapid development of pure electric vehicles and plug-in hybrid vehicles at home and abroad, hybrid vehicles, especially micro-hybrid vehicles and other energy-saving vehicles have also been developed rapidly in the world. In order to meet the increasing requirements of various countries for automobile energy saving and emission reduction, to achieve the functions of reducing fuel consumption, promoting fuel efficiency and CO2 emission reduction, and to meet the needs of all kinds of customers for vehicle performance-to-price ratio, micro-hybrid vehicles are speeding up the development to light-mixed vehicles. Light hybrid vehicles require batteries to provide higher energy or even power. Therefore, the vehicle 48V power supply system is getting accelerated development and application, and it is another expanded application field and development opportunity for lithium-ion batteries that may show advantages.

FAW, SAIC, Changan, BAIC, Jianghuai, Geely and other enterprises have listed 48V electric drive technology as a more feasible technical route to develop passenger cars with 48V battery system. Remarkable progress has been made in the research, production and application of 48V batteries at home and abroad.

Development and demand of power battery

High-performance, low-cost new lithium-ion batteries and new system batteries are the main development direction of new energy vehicle power batteries.

New lithium-ion battery: using high-voltage / high-capacity cathode materials, high-capacity anode materials and high-voltage electrolyte to replace the existing lithium-ion battery materials, the battery cost, specific energy and energy density have obvious advantages. it will greatly improve the economy and convenience of new energy vehicles, and key problems such as durability, environmental adaptability and safety need to be solved.

The new battery system, including lithium-sulfur battery, lithium-air battery and all-solid-state battery, is expected to have lower cost and higher specific energy, and is still in the development stage of basic research.

The new lithium-ion battery will be commercialized in 2020 and practical in 2030.

The research and development of new lithium-ion batteries and new system batteries, improving the intelligent manufacturing level of power batteries, and improving the verification and testing methods and standard system are not only the development needs of energy-saving and new energy vehicles in our country, but also the key task of the development of power batteries in our country. it's urgent.

Development goal of power battery

The development of power battery in China is roughly divided into three stages, with the following objectives:

2020: the stage of technological upgrading. The industrialization of new lithium-ion batteries has been realized. The intelligent manufacturing of power battery has been realized, the product performance and quality have been greatly improved, and the cost has been significantly reduced. The economy of pure electric vehicle is basically the same as that of traditional gasoline vehicle, and plug-in hybrid electric vehicle has entered the stage of popularization and application.

2025: the stage of industrial development. Remarkable progress has been made in the battery technology of the new system. The development of power battery industry is in line with the international advanced level, forming several large power battery companies with strong international competitiveness.

2030: the mature stage of the industry. The battery of the new system is practical, the unit specific energy of the battery is more than 500Wh/kg, and the cost is further reduced.

Conclusion

In the next five years, there will be a huge global demand for lithium-ion batteries. New energy vehicles are the largest application market for lithium-ion batteries, which can quickly replace lead-acid batteries and Ni-MH batteries in electric bicycles, low-speed electric vehicles, power tools, energy storage and other fields.

The market demand for power lithium-ion battery is huge, but the competition in the industry is becoming increasingly fierce, the integration of the industry is continuing, and the market will be further concentrated to the leading enterprises. The next three to four years will be the most difficult period for the upstream and downstream enterprises of the power battery industry chain, especially in the pressure of cost reduction, upstream and downstream enterprises will face unprecedented challenges, which requires the cooperation of the whole industrial chain to tide over the difficulties. enterprises should expand their scale rapidly and occupy market share through the comprehensive advantage of product performance-to-price ratio. Power battery enterprises should put quality and safety in the first place, and only those manufacturers with strong technology accumulation, sufficient financial support, cost-effective products and rapid response to the market can take the lead in the fierce market competition in the future. win the market.

Enterprises should seize the opportunities of Belt and Road construction and international production capacity cooperation, set up international R & D institutions, actively carry out overseas layout, and promote industrial cooperation to transfer to the high-end links of the industrial chain, such as cooperative R & D and brand cultivation. accelerate integration into the global market.