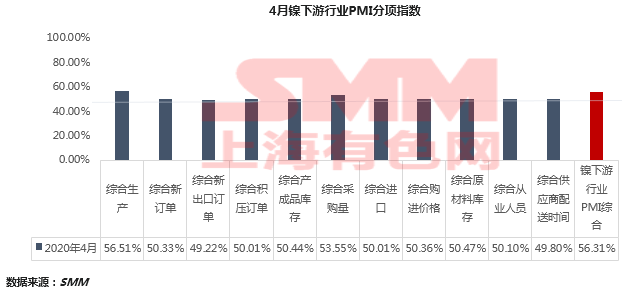

SMM4, March 29: nickel downstream industry PMI composite index final value of 51.76% in April 2020, down 4.55 percentage points from March 2020, still higher than the rise and fall line.

The comprehensive production index is lower than the previous month, but still higher than the rise and fall line, the production tends to be stable.

The comprehensive production index in April was 56.51%, 6.36% lower than that in March, and still higher than the rise and fall line. Domestic enterprises have basically got rid of the impact of the epidemic in terms of production, and have further recovered compared with March. Stainless steel industry production index 56.95%, stainless steel plant operating rate has increased steadily, production reduction only occurred in individual enterprises, most enterprises are still higher than March, according to the established scheduling; electroplating industry due to the late start of the year, after entering April, electroplating enterprises are still making orders before the Spring Festival, so the operating rate has not dropped sharply. The alloy casting industry has basically resumed work in an all-round way, and some alloy casting enterprises in Hubei Province have also produced normally, but some large enterprises are still running at about 80% of the production capacity release rate, so the production instruction has only increased slightly compared with March.

Composite new order index down month-on-month higher than the rise and fall line in April order performance is still good

The composite index of new orders for April was 50.33%, down 10.82% from March. Stainless steel industry new order index 50.67%, orders continue to recover, but most of them are caused by traders "reservoir" storage, to make up for the previous concentrated outbreak of demand delayed by the impact of the epidemic, downstream actual recovery growth rate is general; The index of new orders in the electroplating industry fell to 44.3 per cent as export orders were affected because the overseas epidemic had not yet been effectively controlled, and companies said they had fallen short of expectations in April. The index of new orders in the battery industry was 47.74%, with some traditional battery companies getting worse and production declining slightly, mainly related to the decline in battery demand in the consumer digital sector; in other industries, including printing, nickel wire and nickel mesh, the export order index was affected to a certain extent, falling to 43.15%.

Comprehensive raw material inventory index returns to the normal reserve of enterprises above the rise and fall line

The composite raw material inventory index for April was 50.47%, up 7.65%. As the business situation of enterprises in various industries gradually returned to normal, nickel prices also hit bottom, the procurement behavior of enterprises also returned to normal, and appropriate replenishment, raw material inventory index returned to the normal level. The raw material inventory index of stainless steel industry is 50.29%, which is mainly related to the continuous increase of import supply of large stainless steel plants, while the performance of domestic nickel raw materials is relatively stable.

Integrated product inventory index rebounds to above the rise and fall line marginal improvement of enterprise inventory problem

The composite product inventory index for April was 50.44%, up 4.59%. The recovery of the product inventory index is mainly due to a slight easing of the inventory problem in the stainless steel industry. Stainless steel industry product inventory index 50%, although the market inventory has declined, but the steel mill has also borne a lot of inventory pressure, the whole industry storage problem is still deadlocked, it is worth affirming that, even if we do not consider the centralized compensation of demand, in the current higher output, at least stainless steel will not accumulate, the inventory problem is more caused by the early accumulation.

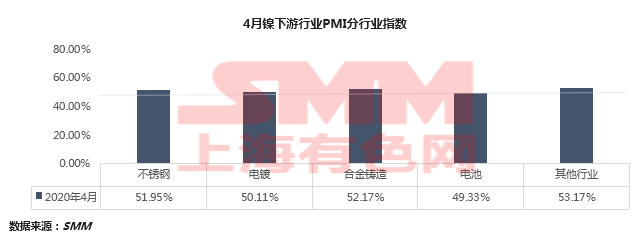

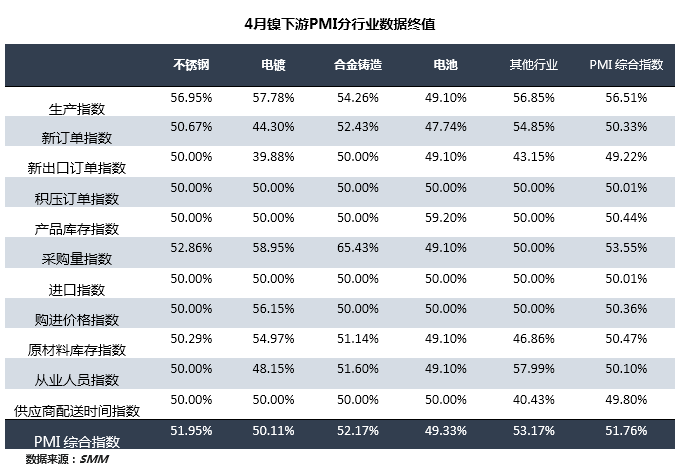

Overview of sub-industry

PMI sub-index of nickel downstream sub-industry in April 2020

The detailed values are shown in the following table:

Stainless steel industry

The final value of the PMI composite index for the stainless steel industry in April was 51.95%, down 4.29% from the end of March, but still above the rise and fall line. Benefiting from the remarkable results of anti-epidemic in China, all walks of life have basically returned to normal, and the stainless steel industry has also continued to recover in terms of production and shipment this month. The production index is 56.95%, the operating rate of stainless steel plant is steadily increasing, the production reduction only occurs in individual enterprises, and the output of most enterprises is still higher than that in March, according to the established scheduling; the new order index is 50.67%, and the orders continue to recover, but most of them are caused by the reserve storehouse of the "reservoir" of traders, to make up for the concentrated outbreak of demand delayed by the epidemic in the early stage, and the actual growth rate of the lower reaches is general. Product inventory index 50%, although the market inventory has declined, but the steel mill has also borne a certain inventory pressure, the whole industry to see the warehouse problem is still deadlocked, it is worth affirming that, even without considering the centralized compensation of demand, in the current higher output, at least stainless steel will not accumulate, the inventory problem is more caused by the early accumulation; Purchase volume index 52.86%, also continue to be higher than the rise and fall line, in the stable production of steel plants themselves are still considerable, and nickel raw material prices are also out of the bottom, the replenishment rhythm of steel mills is relatively normal; raw material inventory index 50.29%, this part is mainly related to the continuous increase in imports of large stainless steel plants, and the performance of domestic nickel raw materials is relatively stable.

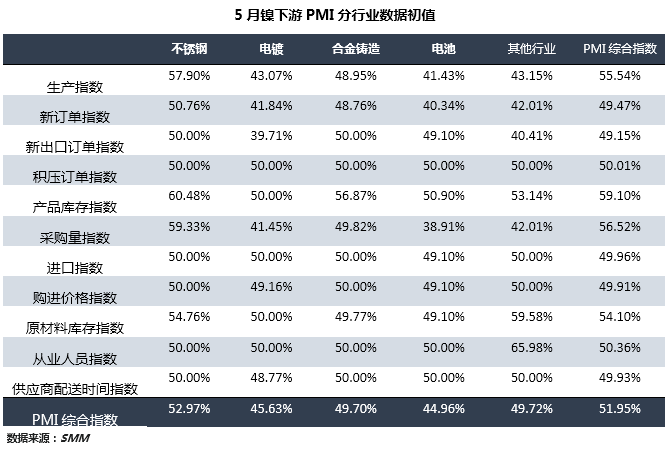

The PMI composite index of stainless steel industry in May was 52.97%, up 1.01% from the end of April. For May, most stainless steel enterprises hold positive expectations in the general direction. On the one hand, domestic demand continues to release, no matter how strong the demand recovery is, it is an important support for the stable operation of stainless steel enterprises at present. On the other hand, the export market of stainless steel is relatively low, and the severity of the overseas epidemic has not been fully transmitted directly to China for the time being, and only a few steel mills say that their orders have been seriously affected. Overall, due to the severity of the epidemic overseas, the market is not as good as expected, but it has not yet fallen into a pessimistic situation. Production index 57.90%, except for a few routine maintenance manufacturers, most steel mills say that production will continue to remain high, but also do not rule out the case of poor orders to reduce production flexibly; new order index 50.76%, although higher than the rise and fall line, but the current sales order pressure is heavier, May order task is basically barely completed, the time node is still slower than the normal level in previous years; The purchasing volume index is 54.76%. It is expected that the demand for nickel procurement will be released actively in the context of the high scheduling of steel mills and the improvement of recent profits.

Electroplating industry

In April, the final value of PMI comprehensive index of electroplating industry was 50.11%, which was 5.38% higher than the expected value, slightly higher than the rise and fall line. The production index was 57.78% higher than expected, and the new order index fell to 44.30%. According to corporate feedback, due to the late start of construction after the year, electroplating enterprises are still making up orders before the Spring Festival in April, so the operating rate has not declined significantly. As the overseas epidemic has not yet been effectively controlled, orders involving exports have been affected, and companies have indicated that they did not expect to receive orders in April. The employment index was cut to 48.15%, and some electroplating factories said there were no clear plans for layoffs, but there had been a marked tightening of new jobs.

In May, the initial value of PMI comprehensive index of electroplating industry is 45.63%, which is expected to be below the rise and fall line. The production index was 43.07%, and the new orders index was 41.84%, both of which fell significantly, mainly due to a further decline in industry expectations for new orders. According to an electroplating company related to auto parts, enterprises have reduced their revenue expectations by 40% according to the volume of orders, and the load of each production line will also be reduced by 40% in May and June. Although the state has introduced some policies to help enterprises tide over the difficulties together, but some employees said that they still can not see significant results in the short term. Since most of the electroplating industry is based on sales, raw material inventory, and finished product inventory will not change much, so the index remains at 50%. However, the employment index, or due to the pressure on companies, will continue to decline.

Alloy industry

In April, the final value of PMI index in alloy industry was 52.17%, which was 12.48% lower than the expected value, but still higher than the rise and fall line. Among them, the production index is 54.26%, and the new order index is 52.43%, both of which are better than last month. At present, the industry has basically resumed work in an all-round way, and some alloy casting enterprises in Hubei Province have also produced normally, but some large enterprises are still running at about 80% of the production capacity release rate, so the production instruction has only increased slightly compared with March. The situation of new orders has not yet recovered, some alloy foundry companies said that although raw material prices have rebounded, but the sales prices of finished products have not improved, in addition to some long-term orders need to be maintained, will also push off low-profit orders. In terms of purchasing volume and raw materials, due to the trend of stabilizing and rebounding nickel prices throughout April, enterprises mostly purchase on demand, and the willingness to prepare goods is weak, so the index has only been slightly improved.

The initial value of the PMI comprehensive index of the alloy industry in May is 49.70%, which is expected to be 2.47% lower than the end of April, lower than the rise and fall line. Some buyers said that in accordance with the current sales-to-production model, the operating rate or due to the order is not ideal and there is a certain retreating slope. The production index fell to 48.95% and the index of new orders fell to 48.76%. Although domestic consumption power is gradually recovering, but whether the product sales price can pick up, or will affect the willingness of enterprises to accept orders. At the same time, the product inventory index rose to 56.87% as expected.

Battery industry

The PMI composite index for the battery industry in April was 49.33 per cent, slightly below the rise and fall line and down 12.33 per cent from the previous month. The performance of the battery industry in April was slightly weaker than in March, mainly related to the traditional battery industry. New energy battery companies were flat in all aspects in April and March, and were in a normal state after coming out of the epidemic. Production index 49.10%, new order index 47.74%, most enterprises stable production, but limited by the scale of demand, there is no room for further expansion, traditional battery enterprises order worse, production decreased slightly, mainly related to the decline of battery demand in the field of consumer digital; Product inventory index 59.20%, the recovery degree of production is higher than the recovery commitment of downstream demand, from the point of view of the whole industry, the inventory days of manufacturers have a small increasing trend; the purchasing volume index is 49.10%, for raw materials, downstream manufacturers are still purchasing on demand.

The PMI composite index of the battery industry in May was 44.96%, which continued to decline from the end of April and was lower than the rise and fall line. The production index is 41.43%, and the new order index is 40.34%. The battery industry's expectations in May were worse than in April, and the impact of the decline in overseas demand gradually spread to domestic companies; in addition, the power battery industry chain is longer, and the process of transmission of the auto industry recession to the upstream industry continues to ferment. As a result, the battery industry is not optimistic about late orders, and so far there has been no additional attractive stimulus for new energy vehicles in China. Raw material inventory index 49.10%, most enterprises said according to the order situation on-demand purchase of raw materials.

Other industries

The final value of the PMI composite index for other industries in April was 53.17%, up 2.85% from the end of the previous month, above the rise and fall line and higher than the forecast value of 48.99%. In other industries, including nickel wire, nickel screen and printing industry, in April, enterprises gradually resumed work and production, and the previous backlog of orders due to the epidemic was released. The production index was 56.85% above the rise and fall line, and the export order index was slightly affected, falling to 43.15%.

Although the domestic epidemic situation has been brought under control, demand has gradually improved, and enterprises have resumed normal production, but the overseas epidemic has spread. Due to the delayed release of previous orders in April, production has not been significantly affected. Orders in May are more difficult to continue, and the impact on export and foreign trade is significant. The order volume has been greatly reduced, and it is expected that the initial value in April will be 49.72%, which will return to the rise and fall line.

Initial value of nickel downstream PMI in May:

The initial value of PMI in the lower reaches of nickel in May was 51.95%, which was 0.18% higher than that of the end of April.

If you have any suggestions, please contact the SMM Big data-Nickel team:

SMM Big data-Nickel Liu Yuqiao

Tel: + 86-21-5166 6804

SMM Big data-Nickel Zhao Ming

Tel: + 86-21-5166 6780

SMM Big data-Nickel Li Chuntian

Tel: + 86-21-5166 6817