SMM, October 17, this morning, the non-ferrous metals market rose and fell each other, by noon, Shanghai lead rose 1.06%, Shanghai aluminum, Shanghai tin rose more than 0.3%, Shanghai nickel fell 3.55% in the morning with the night low.

On aluminum, Rio Tinto said in its July-September quarterly report on Wednesday that it expected aluminium production to be low in the previous production guidance range in 2019 and that its alumina and bauxite production would be lower than previously forecast. Rio Tinto produced 789000 tonnes of aluminium in the third quarter, down 3 per cent from a year earlier and 2 per cent from the second quarter. This mainly reflects lower-than-planned production at the ISAL smelter in Iceland, Kitimat in British Columbia and Becancour in Canada. At the same time, alumina production fell to 7.7 million tons in 2019 from a previous forecast of 8.1 million-8.4 million tons. Alumina production in September was 1.83 million tons, down 7 per cent from a year earlier and 3 per cent from a month earlier. On the bauxite side, Rio Tinto produced 13.8 million tonnes of bauxite in the third quarter of this year, up 9 per cent from a year earlier and 3 per cent month-on-month. However, the company still lowered its production forecast for 2019 to 54 million tons from 56 million tons to 59 million tons.

On the copper side, BHP Billiton (BHP Group Ltd) said on Thursday that copper production reached 430000 tons in the first quarter of fiscal 2020, recovering from supply disruptions in Australia and Chile and up 5 per cent from a year earlier. Separately, on Wednesday, the Peruvian government authorized armed forces and police to intervene to lift the ban on access to one of the country's largest copper mines, after (MMG Ltd), the owner of China Minmetals, said it might have to stop production at the mine.

On the nickel side, according to the official determination of the China Seismological Network, a magnitude 5.4 earthquake occurred on the Philippine island of Mindanao at 20:09 Beijing time on October 16 (20:09 local time on October 16), with a focal depth of 10 km and a epicenter of 6.82 degrees north latitude and 125.10 degrees east longitude. For the local nickel mine, according to SMM, the Philippine nickel mining area from the earthquake occurred in Mindanao area has a certain distance, there is no significant impact for the time being.

On the black side, the black system is generally low today, and market expectations are still declining. Iron ore fell 2.86%, compared with a 0.16% rise in coking coal by midday. News came today that Vale and China Baowu Iron and Steel Group Co., Ltd. signed a strategic project agreement in Brazil on October 16 in the areas of iron and steel smelting, logistics and basic metals, in order to deepen and expand cooperation between the two sides. According to the agreement, the two sides will explore the potential for the continuation of strategic joint ventures and study strategic projects related to international basic metals. The two sides will also explore opportunities for cooperation in logistics and supply chains to effectively transport and receive the world's highest quality iron ore products. "Vale and China Baowu sign strategic project agreement to deepen and expand cooperation

Crude oil tumbled 4.45 per cent to 444.7 yuan a barrel, having fallen as much as 5 per cent earlier in the afternoon. The American Petroleum Institute ((API)) reported Wednesday that API crude oil stocks rose by more than 10 million barrels and recorded growth for five consecutive weeks, but gasoline and refined oil stocks continued to decline. API reported that US crude oil inventories rose 10.5 million barrels to 432.5 million barrels in the week to October 11, the biggest weekly increase since February 2017, and analysts expected an increase of 2.772 million barrels. Cushing stocks increased by 1.6 million barrels. After the release of API data, the United States and cloth oil plate after the short-term decline, supply-side pressure surged with the data.

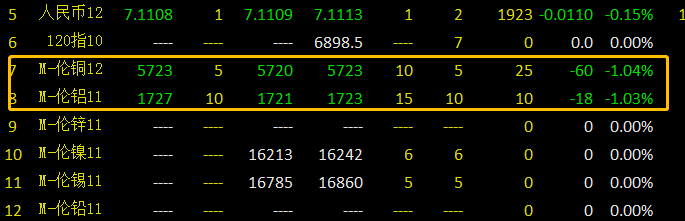

截止11时45分,港交所新推出的LME金属迷你期货报价显示:

Today's stock

Lead: Guangdong market South China lead 17050 yuan / ton, the average price of SMM1# lead up 50 yuan / ton quotation; lead price rose rapidly, recycled primary price difference further opened to 400-500 yuan / ton, downstream priority to buy recycled refined lead, so the primary lead market transaction is flat. Henan Yuguang, Wanyang and other smelters mainly to long single transaction; Jinli 16930 yuan / ton, the average price of SMM1# lead discount 70 yuan / ton quotation. Lead prices quickly upward, downstream wait-and-see-based, market transactions continue a light trend. Other areas such as: Hunan Shuikoushan 16900-16950 yuan / ton, the average price of SMM1# lead discount 100 to 50 yuan / ton quotation (traders); Hunan Jingui 16850 yuan / ton, the average price of SMM1# lead discount 150 yuan / ton; Jiangxi copper industry 17020 yuan / ton, the average price of SMM1# lead rose 20 yuan / ton; Anhui bronze crown 17050 yuan / ton, the average price of SMM net rose 50 yuan / ton; Yunnan small factory 16650-16700 yuan / ton, the average price of SMM1# lead discount 300-350 yuan / ton. Lead prices are rising rapidly, downstream consumption is light, and overall transactions are in the doldrums.

Zinc: the mainstream transaction of zinc in Shanghai was 18840-18950 yuan / ton, and that of Shuangyan and Huize was 18850-18960 yuan / ton; that of zinc was 110-120 yuan / ton in November; that of Shuangyan and Huize was 120-130 yuan / ton in November; that of Shuangyan and Huize was 120-130 yuan / ton; that of Shuangyan and Huize was 18770-18880 yuan / ton. Shanghai Zinc 1911 narrow shock in the morning, and then again by the short down, the first trading session in the morning closed at 18775 yuan / ton. In the first trading session, with the end of the meeting, the shippers' mood resumed, and the average price of ordinary brand zinc ingots on SMM was 5-10 yuan / ton, which rose 110-120 yuan / ton to the 1911 contract. In the second trading session, the zinc price continued to weaken, and the holder maintained the rising price of 110-120 yuan / ton on the 1911 contract. With the end of the lead and zinc meeting, the trading market began to be active, downstream enterprises bargain replenishment, but still maintain in the rigid demand inventory, the overall shipper shipment sentiment is greater than the receiving sentiment.

Guangdong zinc mainstream transaction in 18720-18800 yuan / ton, Shanghai zinc 1911 contract reported in the discount water 20-30 yuan / ton, Guangdong market than Shanghai stock market discount maintained at 160 yuan / ton from 160 yuan / ton to 140 yuan / ton. Refinery normal shipment, the market supply circulation is more abundant, the morning quotation of the holder is concentrated in the 11 contract discount 20 yuan / ton, but the consignee is willing to receive the goods in 11-30 yuan / ton, the market transaction is slightly deadlocked. Entering the second trading period, market transactions focused on the discount of 11 contracts around 30 yuan / ton, some low-cost sources of goods traded in the vicinity of 11 to 40 yuan / ton, the market transaction was slightly boosted, and the trading of traders improved significantly. Overall, the transaction in Guangdong City today is better, traders are willing to receive goods actively, downstream every drop to make up for the warehouse, transactions are better than yesterday. Yi Qilin, Cishan, Tiefeng, Mengzi mainstream transactions in 18720-18800 yuan / ton near.

The mainstream transaction of zinc ingots in Tianjin market is 18850-20360 yuan / ton, the mainstream transaction of ordinary brands is 18800-18910 / ton, the rising water of 1911 contract is about 80-180 yuan / ton, and the rising water of Tianjin market is stable at 30 yuan / ton compared with Shanghai stock market. Refinery shipments are normal today. In the market, the supply of goods is still relatively tight. The quotation of high-priced brand source is concentrated in about 150-180 yuan / ton of 11 liter water, and that of ordinary brand is about 80120 yuan / ton of 11 liter water. Disk downward, rising water stalemate, the market is still more bearish mainly wait-and-see, downstream buying a little boost. On the whole, today's transaction is slightly better than yesterday, but the whole is still relatively light. Zi Zijin, Hongye, Bailing, Chihong, Xikuang, etc., were traded in 18850-18960 yuan / ton, and Zi Zijin, Chi Hong and Hongye were traded in 18800-18910 yuan / ton.

Nickel: today, Russian nickel is 300 yuan / ton higher than Shanghai Nickel 1911, Jinchuan Nickel is 400-600 yuan / ton higher than Shanghai Nickel 1911 contract, only a few traders are reporting 400 yuan / ton, generally 600 yuan / ton. Today's nickel prices continued yesterday's decline, opening all the way lower. In the process of falling, the response of the spot market is mediocre, fully reflecting the mentality of buying up and not buying and falling, and is generally pessimistic about the future. Russian nickel rising water continues to rise slightly, but the trading is not ideal, because the source of negotiable goods is tight superimposed nickel price fell sharply, the holder is more willing to rise. However, there are still some low-liter water supply transactions, Jinchuan Shengshui 400 yuan / ton has the actual transaction. On the whole, it is not as active as the first half of the week, converging with yesterday. The ex-factory price of Jinchuan Company is 131700 yuan / ton, 3000 yuan / ton higher than yesterday.

< updating >

"Click to sign up for a thousand people event in China's non-ferrous metals industry.

Scan QR code and apply to join SMM metal exchange group, please indicate company + name + main business

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)