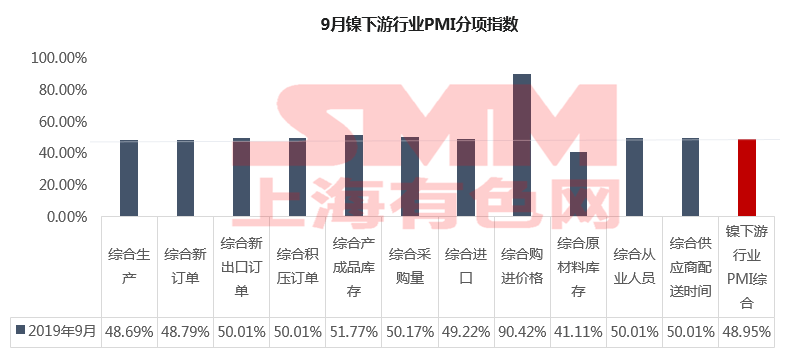

SMM, Oct. 8: the final value of the PMI composite index for nickel downstream industries in September was 48.95%, down from August and continuing to be lower than the rise and fall line.

In September, the composite production index was 48.69%, slightly lower than the previous value of 48.85%, slightly higher than the expected value of 47.49%. The stainless steel production index in September was 47.76%. Most of the stainless steel plants maintained normal production in September when there was still a stock of low-priced raw materials in the early stage, and the output did not decrease greatly. the decline is mainly due to the fine-tuning of some steel mills and the small reduction of some small steel mills. In September, the production index of the alloy industry increased by 15.23%. Some special steel industries may face a new round of environmental protection requirements in October, and the output will be affected to varying degrees. Production and demand in the battery industry slowly recovered, with a production index of 59.58%, lower than previous and expected values, but higher than the rise and fall line.

The composite index of new orders for September was 48.79%, up 0.88 percentage points from August, below the rise and fall line but higher than expected by 46.90%. Among them, the stainless steel new order index 47.76%, compared with the stainless steel factory overall high inventory high scheduling, the order situation appears to be inferior, does not have "the gold nine silver ten" exuberant, but the stainless steel downstream to the price increase also has the ability to accept passively, the demand has not been frustrated by the stainless steel price increase for the time being. In September, the alloy industry new orders index rose 15.23%, downstream orders improved, but still weaker than in the same period in previous years, earnings were lower than in previous years. In September, the battery industry new order index 66.18%, much higher than the previous value and expected value, the battery industry demand slowly recovered, has not yet returned to the level before the subsidy retreat, but there is demand downstream before the National Day, some of the demand pre-demand led to a better performance this month.

In September, the comprehensive raw material inventory index was 41.11%, down 9.07 percentage points from the previous value of 50.18%, below the rise and fall line. The comprehensive raw material inventory index is mainly dragged down by the stainless steel industry. In September, the raw material inventory index of the stainless steel industry was 37.18%, lower than the rise and fall line. During the shock of the high nickel price, the steel mill and the nickel pig iron factory played a fierce game, but under the insistence of the nickel pig iron factory and the capital operation of the trader, the high price transaction was gradually realized.

In September, the composite product inventory index was 51.77%, almost flat from the previous value of 51.91%, slightly lower than the expected value of 52.54%. Among them, the product inventory index of battery industry is 87.37%, which is significantly higher than that of other nickel downstream industries. The main reason is that the output of battery industry recovers obviously, but the demand recovers slowly, and the storage of finished products in the factory is obvious.

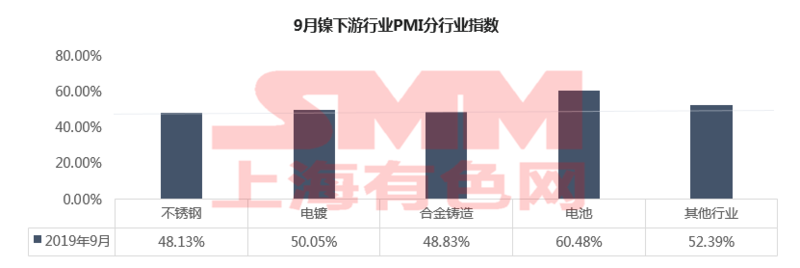

By industry:

September nickel downstream sub-industry PMI sub-index

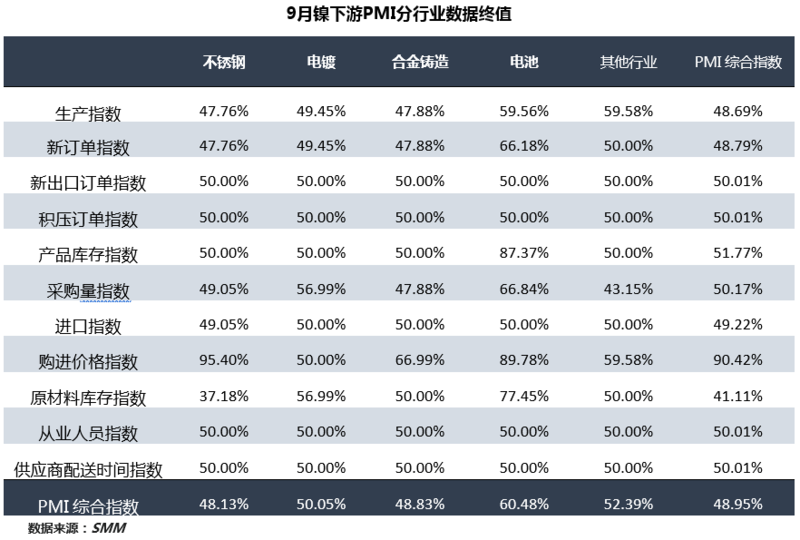

The detailed values are shown in the following table:

The final value of the PMI comprehensive index of the stainless steel industry in September was 48.13%, lower than the rise and fall line, down 1.47% from August, and 0.47% lower than the expected value. Due to Indonesia's implementation of an early mining ban at the end of August, nickel prices skyrocketed, stainless steel plants in September are in a difficult situation, stainless steel increases can not keep up with cost increases, most steel mills without RKEF face losses, and the cost is getting higher and higher how to ship goods is a big problem, it can be said that from the situation before National Day, the expected reduction in production is on the rise. The production index is 47.76%. Most of the stainless steel plants maintained normal production in September when there was still a stock of low-cost raw materials in the early stage, and the output did not decrease significantly. The decline was mainly due to the fine-tuning of some steel mills and the small reduction in some small steel mills. New order index 47.76%, compared with the overall high inventory and high scheduling of stainless steel factory, the order situation appears to be relatively inferior, there is no "gold nine silver 10" exuberant, but the downstream of stainless steel also has the ability to passively accept the price increase, demand has not been frustrated by the price increase of stainless steel for the time being. The purchasing volume index is 49.05%, and the raw material inventory index is 37.18%, all of which are lower than the rise and fall line. During the shock of the high nickel price, the steel mill and the nickel pig iron factory played a fierce game, but under the persistence of the nickel pig iron plant and the capital operation of the traders, the high price transaction was gradually implemented, and the cost level of the stainless steel plant rose in an all-round way. In September, the purchase price index was as high as 95.40%.

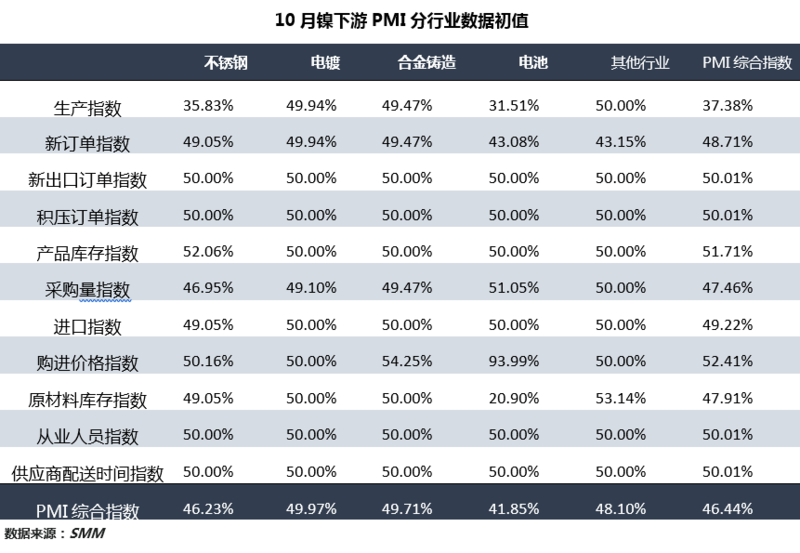

In October, the initial value of the PMI comprehensive index in the stainless steel industry was 46.23%, 1.9% lower than the final value in September, of which the production index was the most obvious, with a reduction of 11.94% to 35.83%. The high price of nickel pig iron was gradually implemented, and there were still signs of continuing to raise prices until National Day. It is expected that the probability of production reduction in non-integrated stainless steel plants will rise significantly next month under tremendous operating pressure. At the end of September, a stainless steel plant in East China announced plans to reduce production, which is expected to affect the output of 300 series of 20,000 tons, while the northern stainless steel plant also has a tendency to reduce the proportion of 3 series. The new order index is 49.05%, 1.29% higher than the final value in September, and the product inventory index 52.06% is 2.06% higher than the final value in September. The surveyed enterprises said that the order situation in October did not improve significantly, not only the social inventory is high, each steel mill also has some in-plant inventory, the later cost pressure and shipment pressure are more prominent. The purchasing volume index is 46.95%, and the raw material inventory index is 49.05% lower than the rise and fall line. The decrease of purchasing volume is mainly caused by the decrease of the proportion of 3 series and the reduction of production in some 300 series stainless steel plants. It is very important for steel mills to stabilize procurement and stable production, but in view of the high cost of products in the later stage, once the market falls, they will lose a lot of money, so they are purchased according to rigid demand, and the stock of raw materials in steel mills is on the low side. some steel mills focus on increasing the proportion of scrap stainless steel.

In September, the final value of the PMI comprehensive index of the electroplating industry was 50.05%, slightly higher than the rise and fall line, slightly better than expected. The electroplating industry improved slightly in September. The composite index of production index and new order index in September was 49.45%, up 8% from August. Orders in September improved slightly, mainly due to the arrival of the National Day holiday and the demand for some orders. Raw material inventory days increased.

The initial value of PMI comprehensive index of electroplating industry in October was 49.97%, in which the production index and new order index were 49.94%. According to the downstream reaction, the situation of electroplating industry in October was weaker than that in September, and also affected the production to a certain extent because of the National Day holiday.

The final value of the PMI comprehensive index of the alloy industry in September was 48.83%, 8.59% higher than that in August, better than expected, and still below the rise and fall line. The annular increase was mainly boosted by the production index, new order index and purchase volume index. In September, the alloy industry production index, new order index and purchase volume index rose 15.23%. Downstream orders improved, but still weaker than in the same period of previous years, and the profit situation was lower than in previous years. Some special steel industries may face a new round of environmental protection requirements in October, and the output will be affected to varying degrees.

In October, the initial value of PMI composite index in alloy industry increased by 0.88% to 49.71%, which is still below the rise and fall line. Downstream demand did not improve significantly in October, and orders are expected to be flat in September, but due to the grim environmental situation, some enterprises in Jiangsu and northern regions are still affected by environmental protection, so the PMI composite index is still difficult to stand on the rise and fall line.

The final value of the PMI composite index for the battery industry in September was 60.84%, up from the end of the previous month and higher than the expected 55.01%. Production and demand in the new energy sector have slowly recovered and have not yet returned to pre-subsidy levels, but there is demand for stock downstream before National Day, some of which has led to better demand this month. This month's production index, new orders index 59.56% and 66.18%, are higher than the rise and fall line.

The initial value of the PMI composite index for the battery industry in October was 41.85%. Production was cut and production fell during the National Day holiday in some factories, while demand before demand led to a significant decline in demand after the return of the National Day holiday.

The final value of the PMI composite index for other industries in September was 52.39%, up 6.85% from the end of the previous month, and returned to the top of the rise and fall line, close to the expected value of 53.37%. In other industries, including nickel wire, nickel mesh and printing, factories received stable orders, and the index of new orders returned to 50% of the rise and fall line. Companies that had previously stopped production due to high temperatures resumed stable production in September, so the production index rose to 59.58%.

The PMI composite index for other industries is expected to be 48.10% in October, which will lead to a small drop in the production index as a result of the National Day holiday in October.

Initial value of nickel downstream PMI in October:

The initial value of PMI in the lower reaches of nickel in October was 46.44%, which was 2.51% lower than that of the end of September.

(for more information, please consult SMM, if you find it valuable, please move your finger to help forward it! )

"Application for downstream industry PMI composite index report trial

Welcome to contact Shanghai Colored Network big data-Nickel team:

Shanghai colored net big data-nickel Liu Yuqiao

Tel: + 86-21-5166 6804

Shanghai colored net big data-nickel Gao Yin

Tel: + 86-21-5166 6865

Shanghai colored net big data-nickel Duan Chunjing

Tel: + 86-21-5166 6896

Shanghai colored net big data-nickel Wang Tong

Tel: + 86-21-5166 6855

Shanghai colored net big data-nickel Wu Ruoyao

Tel: + 86-21-5159 5864