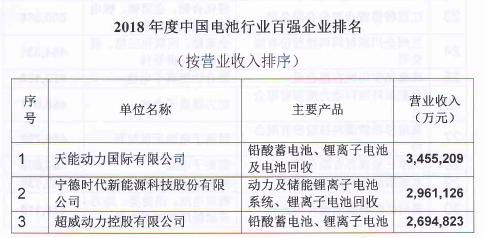

SMM News: on July 29, 2019, the China Chemical and physical Power Industry Association, based on enterprise declaration data and annual report data of listed companies, issued the "list of Top 100 Enterprises in China's Battery Industry in 2018" after examination and assessment. Tianneng Power International Co., Ltd. once again ranked first in the top 100 enterprises in China's battery industry with 34.552 billion yuan, an increase of 28.4% over the same period last year. Ningde Times New Energy Technology Co., Ltd. ranked second with 29.611 billion yuan, an increase of 48.1 percent over the same period last year. Chaowei Power Holdings Co., Ltd. ranked third with 26.948 billion yuan, an increase of 9.3 per cent over the same period last year. Ningde New Energy Technology Co., Ltd. and BYD Co., Ltd. ranked fourth and fifth with 24.665 billion yuan and 21.807 billion yuan respectively, up 32.7 percent and 45.5 percent, respectively.

In 2018, the top 100 enterprises in China's battery industry achieved a total operating income of 449.935 billion yuan, up 19.9 percent from 375.149 billion yuan in 2017. Among the new top 100 enterprises in China's battery industry, there are 25 lead-acid battery enterprises, with lead-acid battery business income of 118.746 billion yuan, accounting for 26.4%; 39 lithium-ion battery enterprises, lithium-ion battery business income of 156.427 billion yuan, accounting for 34.8%; lithium-ion battery module enterprises, lithium-ion battery module business income of 53.93 billion yuan, accounting for 12%; There are 9 zinc manganese / alkaline manganese battery enterprises, zinc manganese / alkaline manganese battery business income 18.014 billion yuan, accounting for 4%; nickel hydrogen / nickel cadmium battery business income 3.004 billion yuan, accounting for 0.7%; material enterprises 26, all kinds of material business income 75.405 billion yuan, accounting for 16.8%; equipment enterprises, 6.339 billion yuan, accounting for 1.4%.

The characteristics of the top 100 enterprises are as follows: (1) the scale of the top 100 enterprises has been further expanded and the industry concentration has increased again: for the first time, the business income of one of the top 100 enterprises has exceeded 30 billion yuan, and the business income of five enterprises has exceeded 20 billion yuan, an increase of 3 over 2017. There are 8 enterprises with more than 10 billion yuan, an increase of 1 over the previous period, and 23 enterprises with more than 5 billion yuan, an increase of 2 over the previous period. There were 53 cases with more than 2 billion yuan, an increase of eight over the previous period. The minimum operating income of the shortlisted enterprises was 771 million yuan, compared with 679 million yuan in the previous period. (2) lead-acid batteries are still in great demand in the fields of vehicle starting, electric bicycles, electric tricycles, low-speed electric vehicles, electric forklifts, communications, new energy storage and so on, but the total output growth rate in 2018 was only 2%. The concentration of lead-acid battery industry has been further improved. At present, there are more than 340 lead-acid battery enterprises in China. Because of the consumption tax levied by the state, the profit margin of enterprises is further compressed, and the survival of enterprises is facing greater pressure. Some enterprises have increased their distribution in Vietnam, India, Central Asia and other regions, expanded overseas production and intensified the development of international markets. (3) lead-acid battery is facing the fierce competition of lithium-ion battery in many fields. In the long run, lead-acid battery is replaced by lithium-ion battery in the fields of communication standby power supply, electric bicycle, new energy storage, low speed electric vehicle and so on. In consumer electronic products, lithium-ion batteries are also rapidly replacing nickel-hydrogen batteries, the market size of nickel-hydrogen batteries is gradually shrinking, the vast majority of nickel-hydrogen battery enterprises' lithium-ion battery revenue has exceeded that of nickel-hydrogen batteries.

According to statistics and analysis of the China Chemical and physical Power Industry Association, China's lithium-ion battery revenue reached 172.7 billion yuan in 2018, up 8.7 percent from 158.9 billion yuan in 2017. Production of lithium-ion batteries increased from 100.9 billion watt-hours to 124.2 billion watt-hours, up 23.1 per cent from a year earlier. This is mainly due to the rapid growth of the market for power batteries and energy storage batteries for new energy vehicles. Among them, the operating income of lithium-ion batteries for consumer electronic products increased from 75.7 billion yuan to 77.2 billion yuan, an increase of about 2 percent over the same period last year, and the output increased by 3 percent from 52.4 billion watt-hours to 54 billion watt-hours. The main markets for batteries for consumer electronic products are mobile phones, laptops, mobile power supplies, power tools and wearable devices. Demand for mobile phones, laptops, tablets and mobile power supplies has all decreased, but demand for lithium-ion batteries for electric bicycles, power tools and wearable devices is growing relatively fast. The operating income of lithium-ion batteries for new energy vehicles increased by 14.1 percent to 89 billion yuan from 78 billion yuan, and the output increased by 45.7 percent from 44.6 billion watt-hours to 65 billion watt-hours. The operating income of lithium-ion batteries for energy storage increased from 5.2 billion yuan, an increase of 20 percent over the same period last year to 6.5 billion yuan, and the output increased from 3.9 billion watt-hours to 5.2 billion watt-hours, an increase of 35 percent over the same period last year.

The market demand of power lithium-ion battery is huge, but the competition in the industry is becoming more and more fierce, and the integration of the industry is continuing. With the deep adjustment of national policy and the rapid decline of subsidies, the concentration of the power battery industry continues to increase, and the market will be further concentrated to the head enterprises. The first 20 enterprises accounted for 91.8% of the installed capacity in 2018, and the top five enterprises accounted for 73.6% of the installed capacity. The top two enterprises accounted for 61.3%. From January to May 2019, the first 20 enterprises accounted for 96.5% of the installed capacity, the top five enterprises accounted for 80%, and the top two enterprises accounted for 70%. In 2019, various enterprises are facing multiple pressures, such as the sharp decline in subsidies, the increase of energy density and the lower limit of endurance threshold, the tension of enterprise capital chain, and so on. The market has entered the stage of rapid reshuffle, and the second and third echelon enterprises are facing greater financial pressure. Many enterprises have given up the power battery business of new energy vehicles and turned to small power markets such as power tools and electric bicycles. In the first half of 2019, the number of power battery enterprises matching with new energy vehicles dropped to less than 70, and the number of power battery enterprises will further decrease in the second half of the year.

Power battery enterprises have a strong desire to reduce costs in the short term, and will make up for them as much as possible by "reducing costs" to upstream diaphragm, electrolyte, negative pole, positive pole and so on, as well as increasing energy density, standardization, large-scale production and other "efficiency" measures. In the next three to four years, it will be the most difficult period for the upstream and downstream enterprises of the power battery industry chain, especially in the pressure of reducing costs, the upstream and downstream enterprises will face unprecedented challenges, which requires the cooperation of the whole industrial chain to tide over the difficulties. Enterprises should rapidly expand their scale and occupy market share through the comprehensive advantage of product performance-to-price ratio, but also maintain reasonable cash flow to ensure the normal operation of enterprises. Power battery enterprises to put quality and safety in the first place, ignore the safety of enterprises will pay huge after-sales costs! Only manufacturers with strong technology accumulation, sufficient financial support, cost-effective advantages and rapid response to the market can take the lead in the fierce market competition in the future and win the market. Enterprises should seize the opportunities of Belt and Road Initiative construction and international capacity cooperation, set up international R & D institutions, actively carry out overseas layout, promote the transfer of industrial cooperation to high-end links of the industrial chain, such as cooperative R & D and brand cultivation, and speed up integration into the global market.

"Click to sign up for this summit

"Click to sign up for this summit

Scan QR code and apply to join SMM metal exchange group, please indicate company + name + main business

![Lead-Acid Battery Market Demand Is Weak, Some Battery Enterprises Shut Down for High Temperature Holiday [SMM Lead-Acid Battery Weekly Operating Rate Comment]](https://imgqn.smm.cn/usercenter/guTSZ20251217171722.jpg)

![Suppliers Expanded Discounts to Dump Goods at Month-End, Spot Market Transactions Sluggish [SMM Refined Lead Spot Market Weekly Review]](https://imgqn.smm.cn/usercenter/mIbTL20251217171721.jpg)

![SMM Primary Lead Smelter Weekly Operating Rate (July 17, 2026 - July 23, 2026) [SMM Primary Lead Smelting Weekly Review]](https://imgqn.smm.cn/usercenter/mfCMp20251217171721.jpeg)