SMM10 19: at the "2018 China Nonferrous Metals Annual meeting and 2019 (SMM) Metal Price Forecast Conference" held by Shanghai Nonferrous Metals Network, Fu Peng, global macro hedge fund manager, Chong he investment director and director of macro strategy, said. The market overestimates the "illusion of optimism" we have seen over the past two years, and the relationship between the economy and commodities is discussed more on the demand side. The commodities we have seen over the past two years are far better than the risks we feel, and the fundamental reason is that China launched supply-side reforms in 2016. In the past few years, the gambling policy may have been right, but in the next few years, China will continue to deleverage, reduce the debt ratio, control finance, control real estate, return to reality, and enterprises should be psychologically prepared to deal with it. No more gambling!

In the next two years, China will basically copy Premier Zhu's "risk prevention" path.

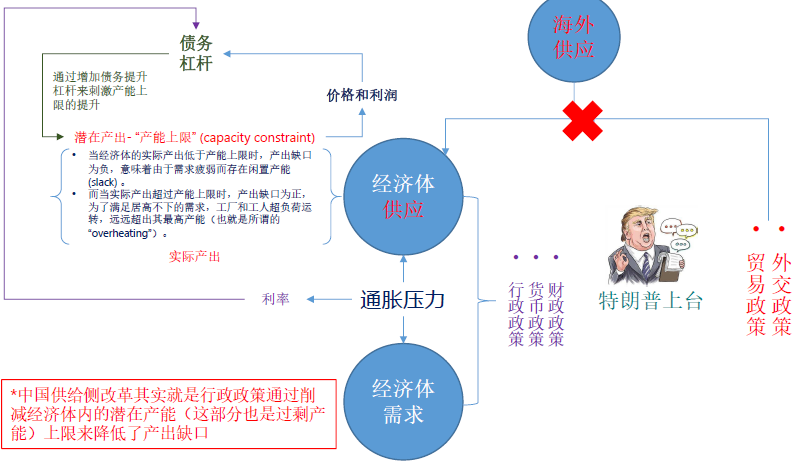

China's supply-side reform is that administrative policy has reduced the output gap by cutting the upper limit of potential capacity in the economy, which is also excess capacity. The real starting point of supply-side reform is the supply-side reform implemented by Premier Zhu Rongji in 1998. In the next two years, China is basically copying the whole process of domestic debt and leverage in the process of dealing with domestic debt and leverage, how to use supply-side reform to achieve debt risk relief, this is what we really want to review.

In 1998, Premier Zhu Rongji's "risk prevention" path: monetary policy was "neutral and tight", forcing enterprises to remove production capacity and deleveraging. The use of administrative means, supply-side reform: stop repeated construction, clean up excess capacity, merger and bankruptcy of backward enterprises, laid-off diversion of labor. When an enterprise's creditor's rights are converted into equity, the financial policy goes to the bottom, and the asset management company divest the bank debt. We will implement a positive fiscal policy based on the issuance of additional long-term construction treasury bonds.

From 1998 to 2000, the essence is to restrain the supply side by administrative means, so that after the supply curve is tightened, the price recovery brings the industry profit to rise, and then resolve the debt of the excess capacity industry. This page has also been experienced in the past two years.

How do you interpret supply-side reform? Because of the simple rise in prices, there will be a feeling that the advantage of rising prices will come. But it's obviously very different from how you feel. The reason is that the price rise is more from the supply side, and what you feel is the demand side. So in the past two years there has been a strange phenomenon, for example, the black industry chain is very comfortable, a year to earn hundreds of millions, billions! But it is important to understand that the money made in the past two years is not because the industry itself has reached the dimension of making money, but more because of the policies of the past two years.

Since 2014 and 2015, the great dimension of China has entered a stimulus brought about by $4 trillion, and the single negative effect has also been gradually reflected. Since 2014, China's main task has been how to remove debt, reduce leverage, and gradually burst bubbles within a manageable range. Because of the huge changes in the biggest debt side in 2014 and 2015, the United States began to raise interest rates!

The reasons behind the shift in American Policy and the sharp rise in populism

There has been a drastic revision of US monetary policy. Soros said when he talked about global economization, including China's current senior levels, including the current consensus that global economic integration will lead to win-win values. Bring China to win and the United States to win. Of course, if you look at this point of view alone, it seems to be quite correct. A spokesman for the Ministry of Foreign Affairs has also said that China has earned global income and has achieved a surplus through labor production and processing. But America's powerful financial multinationals, Wall Street and the US debt clearing system have resulted in the distribution of entire wealth on the US capital side. It sounds fair, but a few decades ago, these economists, including Krugman, analyzed it, which was not the case, because the most important message was that under the division of labor brought about by global financial integration, Will it lead to uneven domestic distribution among countries because of their different division of labor? The United States is a typical example. Transitional countries have lost their real economies, such as the total disappearance of Detroit factories in the United States and taken away by China, ostensibly as Wall Street has become rich and bottom workers have lost their incomes. But this model in the United States is unsustainable, Soros explains. Wall Street's continued strength and financial strength will lead to a further increase in the rich and the poor and, in the end, who will control the vote. Mr Soros says the result of global economic integration is a sharp rise in populism.

Populism has a nice word for patriotism, so the US has faced these problems since the collapse of the subprime mortgage crisis in 2008. During the global economic boom of the past two decades, excessive US finance has created internal imbalances. Since 2008, the United States has been carrying out measures such as restrictions on Wall Street, strengthening financial regulation, real estate regulation and so on. Trump came to power and populism warmed up. The United States has made such a return over the past decade, and it has to do so. Because in the words of Krugman, we are competing with each other, and he is good without you. In the future, once there is a crack in the global economy, or from Hello, I am good, he is good, it is good for me, you are bad for you, if I change bad, you will become worse than me. This is the case with financial relations between countries and countries with large categories of assets around the world from last year to this year.

Most people have only experienced the process of globalization in the past 20 years, habitually forming the concept of global co-governance, Europe will recover, Japan will recover, and it is customary to judge economic recovery from the relationship between large categories of assets. However, the current situation is whether the risks in emerging markets should explode, from Brazil, Argentina to Turkey. Get blown up. Trump policy is one of the reasons, and the other is the redistribution of all income under the structure of global economic integration.

It can be understood that emerging markets, if the market does not grow there will always be debt problems, the problem today is that the strong United States has not led to income growth, debt problems will lead to emerging market problems one by one. China has the same problem, but we don't have the same open access to the market as they do. China will introduce capital controls after 2015, giving it a better organizational approach when it comes to reprocessing debt and income relations at home. From this, it can be seen that the supply reform in 2016 is a policy designed to resolve debt, and the market for simple balance sheet repair is the same as in 1999.

The deeper meaning of Commodity Trading Choice

At the peak of copper prices last July, our trading choice was to do a lot of long crude oil at $45. At that time, it was explained why the relationship between shorting copper and oil copper was not just a commodity. The deep meaning was that when oil prices rose sharply, the oil-copper ratio began to rise rapidly, often because of the risks brought about by interest rate shocks. The classic deal was in 1998 and 1999. During the Asian financial crisis in 1997, the price of crude oil rose far more than that of copper in 1999, which finally caused the Internet bubble in 2000, with interest rates exceeding the total demand. This is the implicit answer of the most famous commodity trading. Therefore, the commodity portfolio should not only have a very strong meaning of commodity trading, but also implies a very strong meaning of relationship, and its corresponding result is that the transaction makes a lot of money.

The volatility of the global market in 2018 is very high, and this year the market is doing a trade, not betting that the US stock market will rise further, but has been buying insurance trading. Why? The rise in interest rates and the continuous rise of US bonds to 300 million will eventually have a major impact on global rights and interests. Emerging markets were the first to take risks in February, the US was slightly stronger than the rest of the world, and the second shock came again in October.

At present, the oil price on the international market is about 10 yuan, the ratio of oil to copper is more than 30, the direct result is the impact of interest rates. Will history repeat itself? Yes.

What about the economy?

What about the economy? The global economy is not much, and the momentum and potential of economic growth have always been problematic in the past six or seven years. It is precisely because the potential of economic growth is problematic that the global total cake distribution is not enough, thus leading to the present situation. Countries are forced to protect their incomes by their own populism.

It might be better to stand on the shoulders of your ex and see a lot of things. The old people who have experienced these things in those days, their experience is very worth learning from. The approach we take in dealing with the same problem is almost exactly the same.

The result of Trump's policy is the logic of anti-globalization.

How to look at the impact of the expansion of global aggregate demand on commodity markets if the United States wants to engage in fiscal stimulus, tax cuts, and the expansion of global aggregate demand. The expansion of US debt and fiscal expansion will eventually translate into the total demand of the United States, and the supply of the United States will be insufficient under the growth of total demand in the United States, so its expansion of total demand will certainly translate into the expansion of total demand in the periphery of the producing countries. In turn, it is converted into orders from the producing country, and then into the demand for basic raw materials in the producing country, and finally into a driving force. It is entirely based on this line that US tax cuts or fiscal stimulus will lead to higher commodity prices. But the prerequisite for this line is global economic integration. This is Trump's left hand card. You don't see Trump's right hand card.

Like this picture, there is no problem looking at the left hand alone, which is bound to translate into our overseas demand, that is, the overseas supply of the United States. But when Trump adds his right hand, he will find that the expansion of aggregate demand in the United States will lead to a shortage of supply in the United States.

We have been talking about aluminum, such as Trump's aluminum tariff, which has resulted in a significant increase in aluminum in the United States and a rise in the price of downstream products. But Americans still make their choices in order to protect the interests of their own country, which is typical of populism. But as financial markets, we must look at all issues calmly.

Moreover, Trump has a hand, and when the trade link is played, the United States will be turned into a shortage of internal supply, resulting in inflationary pressure on employment wages in the United States is far from a very tight state. It will be interesting to see that the debt of some countries is tightening sharply, because it is the internal factors that determine the US debt. The Fed made a big move forward, the rate rise should continue to rise, and US bond yields should rise upward. You find a problem, not only is the cost of debt increasing, but your income is also decreasing. You can see why the end result of Trump's policy is that emerging markets go wrong one by one. This is in fact a typical anti-globalization logic.

Anti-globalization brings turmoil to global financial markets. China deleveraging and deleveraging will not stop.

The structure of the previous analytical framework is about to change. What will happen to us when the reverse globalization is torn apart? Your surplus or your surplus, you must constrain your supply side through supply-side reform, you must eliminate a large number of people, but it will also lead to an uneven distribution of income. Debt must come down and leverage must come down. In the process, can real estate have a good day? Is there a good day for finance? Will there be a good day for the stock market?

It should be said that our means should be much better than those of countries such as Brazil and Argentina. We can intervene in the market through administrative means to transfer distribution, debt and leverage. For example, the best way of debt transfer in the real estate market is to regulate the first-line market, limit purchases, the first line can not buy, let the second and third lines to inventory.

China has been dealing with debt and leverage in recent years. From 2006 to now, the result of bigger and stronger finance is the crazy growth of asset prices and the uneven distribution of wealth. In short, it is impossible for finance to serve the real economy. The nature of finance is greedy, the nature of debt and leverage is greedy, so debt can not expand infinitely, in the end, there will be a process of redistribution, the same all over the world. What will happen to China in the next few years? To prepare for the hard times, China will continue to deleverage, reduce its debt ratio, control the property market and control the financial market, so companies should be psychologically prepared to deal with it. In the past few years, the gambling policy may have been right, but next, we can't gamble any more!

Commodity markets will fall into a state of low volatility

Most commodities will fall into a very low volatility state next year, with no obvious trend. Perhaps the same is true of the macro situation in the next two or three years. Therefore, it is more likely to find some contradictions in the structure of their respective commodities, which is far better than the discovery of some macro contradictions.

To draw a distinction between assets in the next few years, rights and interests, interest rates, energy are the same, commodity attributes and macro correlation more and more desalinated.

What will be the state of anti-globalization? What's the future?

The demand increment should not be as high as it used to be. Crude oil will have a direct effect on monetary policy on interest rates, resulting in a substantial rise in interest rates, and the rate of return on asset investment, that is, the demand for real economic growth, can no longer be pushed up, which is the beginning of the bubble. Will China have a good opportunity to increase our aggregate demand in the future, similar to that given in 2002? In the next few years to remove debt, deleveraging, the challenges are still greater.

To put it simply, what Xi Jinping said was right. De-debt, deleveraging, control of finance, control of real estate, return to reality, the house is used to live, not to speculate, everything is logically right. Is that what's left of you? do you still want to bet?