SMM8, March 23: the recent surge in the US dollar has made the global non-US exchange rate market suffer.

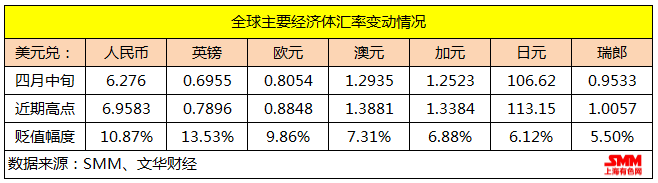

Since mid-April, the dollar has jumped like a runaway rabbit, rising 16 per cent from a low of 82.215 to a recent peak of 95.531. In sharp contrast to the strength of the US dollar is the decline of the rest of the currencies. Similarly, since mid-April, the renminbi and sterling have depreciated by more than 10%, the euro has depreciated by 8.8%, and the Australian dollar, Canadian dollar, yen and Swiss franc have all fallen by more than 5%.

Exchange rate movements in the world's major economies:

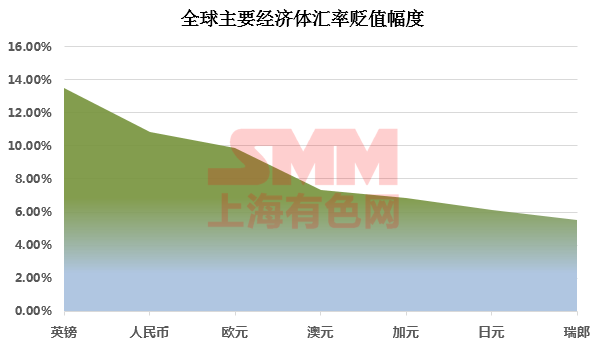

Exchange rate depreciation in some of the world's major economies:

For emerging markets, the rise of the dollar is more than just a change in the exchange rate, along with the collapse of their own currencies, the collapse of the exchange rate market, the withdrawal of foreign investment, and the collapse of the stock market. Until domestic inflation and the value of domestic assets shrink, the economy of the whole country will fall into crisis.

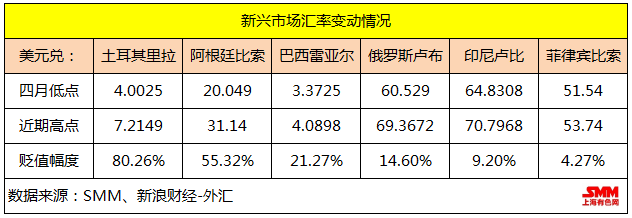

Emerging market exchange rate movements:

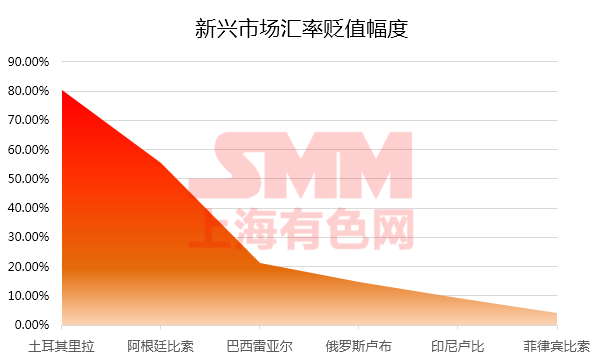

Emerging market exchange rate depreciation:

In the picture, we can find that the Turkish lira with the highest devaluation is naturally the Turkish lira, which was "stabbed" by Trump some time ago. Since the sharp rise in the US dollar in April alone, the lira has depreciated by more than 80%. If we start at the beginning of this year, The lira has nearly doubled in value.

Dollar Turkish lira (USDTRY):

(from a low of 3.72 at the beginning of the year to a recent high of 7.2149, with a total devaluation of 93.94%)

Affected by the collapse of the domestic exchange rate market, domestic inflation in Turkey remained high. According to statistics, in June this year, the consumer price index in Turkey rose 3.24 percentage points from the previous value to 15.39%. In July, The inflation rate remained high, rising to 15.85%, the highest level in nearly four years. The soaring prices have dealt a serious impact to the domestic economy, with Turkey's real estate industry affecting the most. As most of the raw materials used for building houses depend on imports, the collapse of the lira has led to a rise in the prices of raw materials. In addition, the Turkish central bank raised interest rates in order to tighten the currency, resulting in a loan interest rate of 25%, and developers doubled the pressure to repay their loans. According to the latest news, although the Turkish government has begun to cut interest rates and developers have begun to cut prices, there are still very few buyers, and most of the real estate projects in Ankara have been shut down.

Also suffering from the same situation is Argentina, which is also an emerging market. In order to curb the decline of the Argentine currency, the Argentine government was forced to raise interest rates three times in a row in a short period of a week or so from April 27 to May 4. To stabilize the shaky monetary system.

Dollar appreciation: a key step for the United States to plunder the fruits of the Global economy

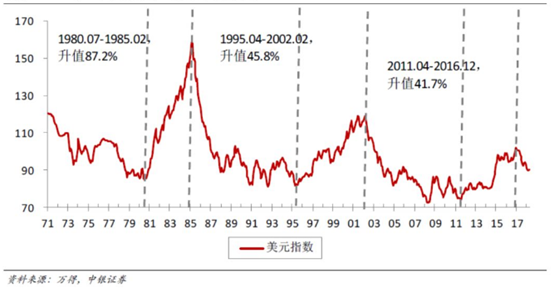

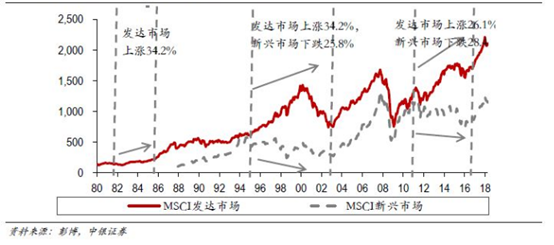

The tragedy of emerging markets, however, is not the first time that the dollar has risen for the first time. There have been three cycles of appreciation in history, each of which has been accompanied by severe capital outflows and financial crises from emerging market countries.

Three dollar cycles:

Market performance corresponding to the three dollar cycles:

As a global currency, a sharp appreciation of the US dollar can enable global capital to flow back to the mainland quickly, and a large part of the capital flow lies in US Treasuries. For the United States, Treasury bonds are an important tool for reabsorbing dollars from around the world.

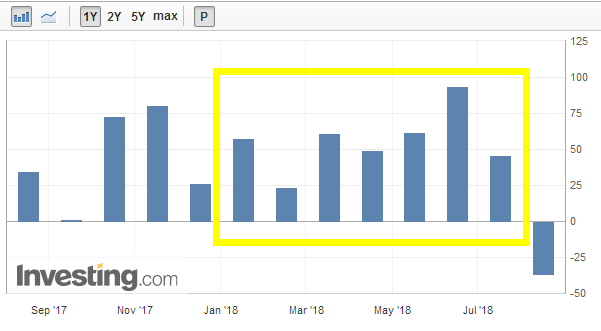

Us International Capital flows report (TIC) net long-term Capital inflows:

(net long-term capital inflows to the United States have been positive since the first half of this year.)

In a new era in which global trade continues to grow by leaps and bounds, in order for the world to continue to settle in dollars, while ensuring the dominance of the dollar in the international monetary system, the United States needs to continue to export dollars. If the US dollar flows out of the country, it will cause a shortage of domestic currencies, the US dollar will appreciate sharply, and this direction will never be reversible. Long-term currency appreciation will deal a fatal blow to the US industry, and at the same time put great pressure on US exports.

To this end, the United States began to overissue money, combined with the long-term implementation of low interest rate monetary policy, to promote domestic private investment and consumption, through the market to flow dollars to the world. With the means of distributing US dollars, it is also necessary to recover US dollars. what the US government has come up with is high-interest US Treasuries, which, on the one hand, serve as a recovery link in the monetary cycle system, and on the other hand, provide a large supplement to fiscal revenue.

In this way, although the international status of the dollar has been maintained, there is a new big problem in front of the US government: what should we do with the huge US national debt? The United States has chosen to forcibly reduce its debt through various means, either through trade wars, or under pressure from military forces, or by other political means. At this point, it is clear that there is a road of "plunder" derived from the US dollar. The successive appreciation of the dollar has been accompanied by "cutting leeks" against the global economy again and again.

In understanding the importance of the appreciation of the US dollar, it is not difficult to understand why the US Federal Reserve has repeatedly wanted to raise interest rates at home, on the one hand, the hegemonic position of the US dollar in the future, and at the same time, Higher interest rates have also helped to correct previous excessive leveraged lending due to ultra-low interest rates. As long as the US economy is on track, the Fed is ready to raise interest rates again, according to the minutes of the Fed meeting in August. It is reported that the Fed statement mentioned the word "strong" five times and made a rare comment that "US economic activity is rising at a strong rate", deleting the "robust" growth statement from the last meeting statement. This shows that Fed officials at the meeting are confident that the US economy will grow strongly at least in the near future.

However, not everyone in the United States supports the continued appreciation of the dollar, such as US President Donald Trump.

Trump lashes out at Powell for raising interest rates by the Federal Reserve

"I'm not excited [about the strength of the dollar]," Trump said in an interview with CNBC on July 19. Because every time we start the economy to get better, the Fed wants to raise interest rates again. I'm not happy about it. " This is not the first time Trump has publicly criticized the Fed's monetary policy. Trump believes that the rise in the dollar exchange rate will give other competitors an advantage and make it difficult for him to win in a trade war. So what makes a president risk universal opinion to intervene in the Fed's interest rate decision, which claims to be first in terms of independence?

Unlike former President Barack Obama's efforts to revive the economy through increased government spending, Trump wants to focus his economic growth on tax cuts, trade protection, industrial relocation, increased military spending and infrastructure investment. His argument is the opposite of the Fed: economic growth requires a weak dollar.

(source: Fed official website)

For Trump, dollar hegemony no longer seems to be the first point of his consideration, as the United States withdrew from the Trans-Pacific Partnership (TTP) in 2017 as a front stop for industrial relocation and trade protection. In order to better revitalize and support domestic enterprises, especially the manufacturing industry, the United States needs the depreciation of the US dollar to promote exports, and under the Sino-US trade war, which has lasted for more than half a year, The devaluation of the yuan has partly slowed down the strength of the trade war that Mr Trump had envisioned.

Trump believes that competitors in a massive trade war with it have used currency depreciation to avoid sanctions, and he has criticized departments such as the Federal Reserve for giving competitors an advantage by raising the dollar exchange rate. On the other hand, the Fed said that in the long run, a stronger dollar is good for the US economy, and that it still showed a hawkish attitude at previous Fed policy meetings, suggesting that interest rates would be raised further.

Who are you going with in the future?

After a four-month rally, the dollar index retreated for the first time, suspended by Trump's "criticism" of Powell's exchange rate policy and the macro risks of advancing trade talks between China and the United States, starting last Thursday (August 16). The dollar closed down for five days in a row.

Meanwhile, on Aug. 21, Trump's former lawyer, Michael Cohen, admitted that he had violated campaign finance laws before the presidential election-at the behest of then presidential candidate Donald Trump. As soon as the news came out, the dollar continued to weaken. But just two days later, news of a 25 per cent tariff on about $16 billion in goods revived global risk aversion and boosted the dollar.

(us President Donald Trump gives a speech)

At present, there are different opinions on whether the dollar is a "real fall" or a "fake fall", but the Fed is likely to raise interest rates in the coming September, although uncertainty in the US political situation is putting pressure on the dollar. But the hawkish hints of the latest Fed minutes no doubt support the dollar.

SMM collates the views of major institutions on the future development of the US dollar and the subsequent economic situation in China:

Li Yong, Chief analyst of fixed income and Big Finance at Northeast Securities:

The US economy grew 4.1 per cent in the second quarter of this year, inflation and unemployment were at record lows, and the US economy showed strong momentum. The successive interest rate increases by the Federal Reserve and the high probability of interest rate increases in September and December have exacerbated the flow of international capital back to the United States. The collapse in the Turkish lira has heightened international capital concerns about debt defaults and investment climate in emerging markets. From the domestic point of view, the economy is under pressure, the market shows a certain pessimistic mood, the financial industry from deleveraging to the "stable leverage" stage. Supply-side structural reform has entered a deep water area and a difficult period, but the new uncertainties in the internal and external environment are increasing, the difficulties and challenges are increasing, and the downward pressure on the economy is still obvious.

Shao Yu, Chief Economist of Oriental Securities:

At present, China's monetary policy should grasp the balance between stable growth and risk prevention. There is a liquidity supplementary demand within our country, but the external US dollar has a tendency to tighten monetary policy and raise interest rates in the interest rate hike cycle. If we take into account China's economic growth, monetary policy has a marginal relaxation requirement. Once the external policy is tightened, it will form greater pressure on the RMB exchange rate, but also lead to a certain degree of capital outflow, so the internal and external environment faced by the Central Bank of China is more complex. If the United States raises interest rates twice, our central bank may say something. However, from the current domestic policy point of view, the central bank has' hit 'the interbank market interest rate to a lower level through the continuous directional reduction of the standard and the corresponding monetary policy operation. Do not rule out or have a certain space to rise, but the space is relatively limited, after all, the real economy is relatively "fragile", to reduce financing costs is a top priority.

Citic Securities analysts Zhu Jianfang and Cui Rong:

In view of the upward trend of core inflation in the United States, the Federal Reserve will raise interest rates once a quarter this year, and the European and Japanese Central Bank meetings in July have expressed the dovish position of monetary policy one after another, and the dollar index still has room to rebound in the third quarter. The rebound height is about 96-97. But in their view, the dollar index is still in a downward trend in the medium to long term, "because the divergence of monetary policy between the European, Japanese central banks and the Federal Reserve will narrow." The middle and late stages of the US economic and monetary policy cycle and Trump's trade policy orientation do not support the continuation of a strong dollar. Our benchmark for a weaker dollar is September, when markets expect changes in Fed rate hikes and tightening by the European and Japanese central bank, while relatively strong second-quarter economic data from the United States will be released in the third quarter one by one.

SMM warm tip: if you like this article, you can forward it to more friends who pay attention to the economy, your attention and support is our driving force.