SHANGHAI, Apr 8 (SMM) - This is a roundup of China's metals weekly inventory as of April 8.

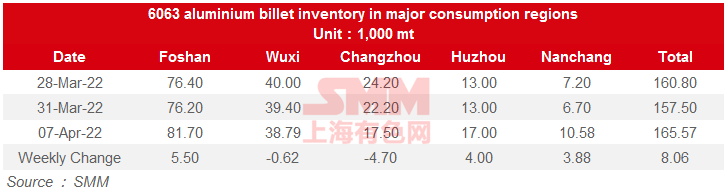

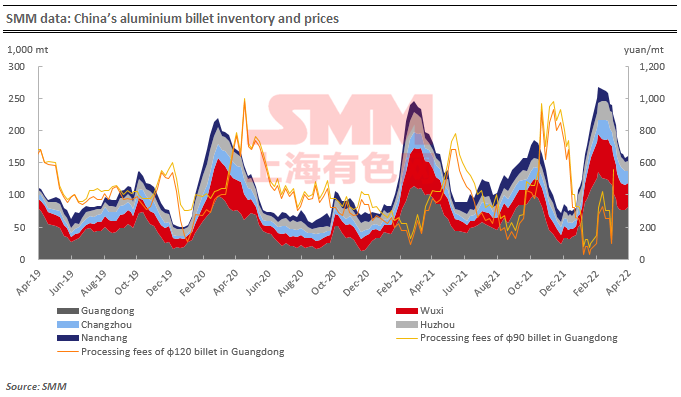

Aluminium Billet Inventory in China Increased as Pandemic Undermined Consumption

The domestic aluminium billet inventory stood at 165,600 mt as of April 7, an increase 8,100 mt or 5.12% from a week ago. The regional inventory changes were as follows: Nanchang (+3,900 mt or 57.91%); Changzhou (-4,700 mt or 21.17%); Wuxi (-600 mt or 1.57%); Huzhou (+4,000 mt or 30.77%); Foshan (+5,500 mt or 7.22%). The pandemic-induced transportation problems in Wuxi prompted buyers to pick up cargoes from Changzhou, where the pandemic was less severe, leading to a sharp decline in local inventory. This week, the impact of the pandemic on truck shipments has intensified, especially in east China, where both inflows and outflows of cargoes were hindered. In addition, traders and downstream producers refrained from purchasing amid sluggish end consumption, also contributing to higher inventory in Foshan, Huzhou, and Nanchang.

Given declining demand in mainstream consumption areas under the influence of the pandemic, it is expected that the aluminium billet inventory will continue to accumulate next week.

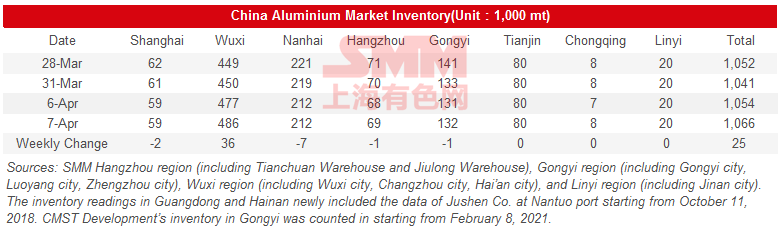

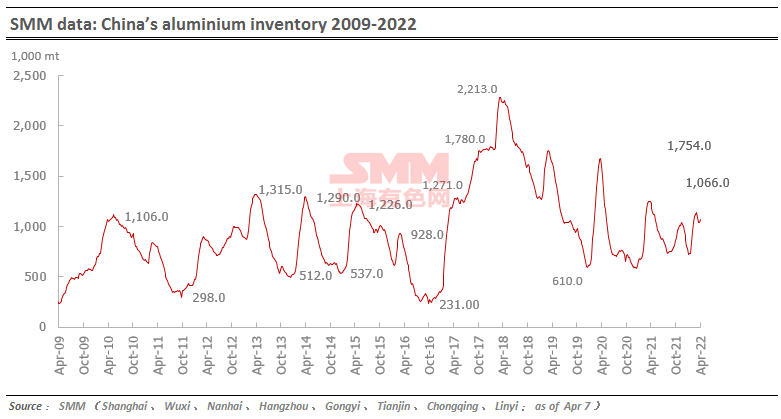

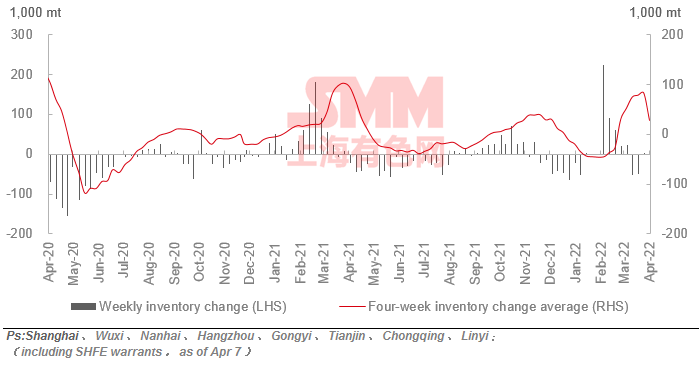

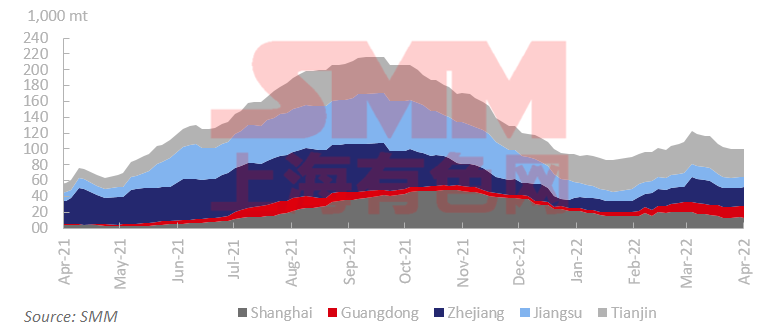

SMM China Aluminium Social Inventory Added 25,000 mt on Week

SMM China aluminium social inventory totaled 1.07 million mt as of Thursday April 7, up 25,000 mt on week.

The inventory in Wuxi rose the most by 36,000 mt on a weekly basis as the local transportation was severely affected by the pandemic, and the warehouses could not ship normally; in terms of arrivals, the railway transportation has been regular, and truck drivers with traffic permit and negative nucleic acid testing report within 48 hours are allowed to enter the city. The inventories in Tianjin, Chongqing and Linyi were flat, and those in Shanghai, Nanhai and Hnagzhou falling to different degrees, with Nanhai (-7,000 mt) falling the greatest.

The market shall keep watching the changes of aluminium prices and the marginal impact on inventory.

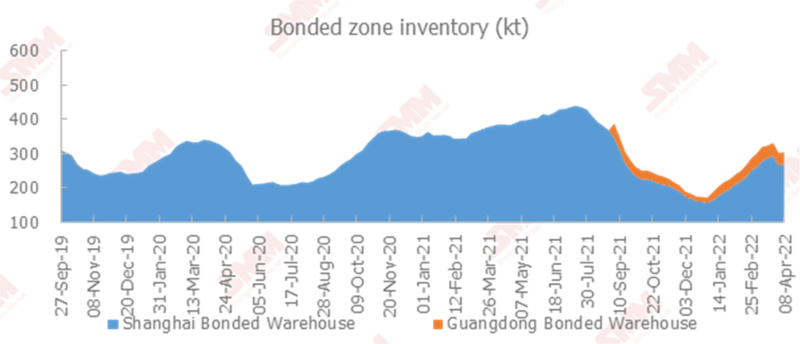

SMM China Copper Inventory in the Bonded Zone Rose 2,100 mt on Week

SMM China copper inventory in the bonded zone added 2,100 mt from last Friday April 1 to 306,500 mt as of April 8. Among them, the inventory in Shanghai bonded zone stood unchanged at 269,800 mt, while that in Guangdong bonded zone rose 2,100 mt on a weekly basis to 36,700 mt.

The import window remained closed this week, and the imports that completed customs clearance this week were low. The shipments to and from bonded warehouses in Shanghai were deeply affected by the pandemic, and real flow of goods was almost stagnant despite pre-customs declaration, hence the weekly inventory stood unchanged.

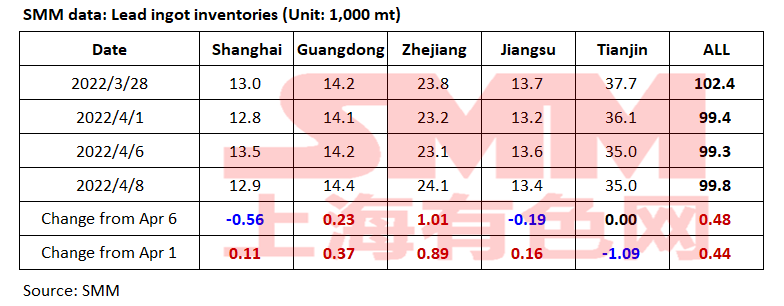

SMM China Lead Ingot Inventory Up 400 mt on Week

SMM China lead ingot inventory across five major markets totalled 99,800 mt as of Friday April 8, up 400 mt from last Friday April 1 and 500 mt from Wednesday April 6.

According to SMM research, lead-acid battery market has been increasingly muted after the Qingming Festival, and some lead-acid battery manufacturers even curtailed the production due to resurging pandemic, resulting in less demand for lead ingot compared with March. In addition, as lead prices dropped recently after hitting high, futures and spot prices showed great differences, especially in the major supplying areas like south China where the supply has been relatively sufficient, and the spot prices were mostly in wide discounts. However, the Shanghai market was still affected by the pandemic, and the operation of warehouses faced many difficulties. The sources from early deliveries were shipped from Zhejiang and Jiangsu, and arrived recently, reversing the previous fall in local inventory.

SHFE 2204 lead contract will be delivered next week, and lead social inventory is expected to rise after the sources for delivery arrive.

SMM China Copper Inventory in Major Markets Rose 2,600 mt on Week

As of Friday, April 8, SMM copper inventory across mainstream regions in the country achieved the first weekly rise since March 4, with an increase of 3400 mt to 140300 mt compared with Wednesday April 6, and a slight increase of 2600 mt compared with last Friday.

From Wednesday to this Friday, the regions where inventory increased and decreased each accounted for half across the country. Specifically, the inventory in Shanghai increased by 4500 mt to 83700 mt; rose by 400 mt to 45100 mt in Guangdong; added 2000 mt to 4200 mt in Jiangsu; decreased by 100 mt to 500 mt in Zhejiang; fell 1000 mt to 2200 mt in Chongqing; and dropped 400 mt to 2000 mt in Tianjin. Affected by the pandemic, the country's logistics has been in chaos recently. The inventory in Shanghai increased as the trucks are not allowed to leave the city due to severe pandemic situation. The inventory of Jiangsu and Zhejiang has decreased as the local downstream customers have turned to purchase local inventory. The arrivals in Guangdong have generally returned to normal, but the inventory increased due to poor downstream consumption. If the manufacturers in east China had not turned to the north for procurement at the end of this week, the inventory in Guangdong should have risen more significantly.

It is expected that the inventory will continue to increase next week because the logistics has little possibility of returning to the normal level, and the smelters who are to deliver the SHFE 2204 contract will also increase the shipments directly to warehouses through railway transport.

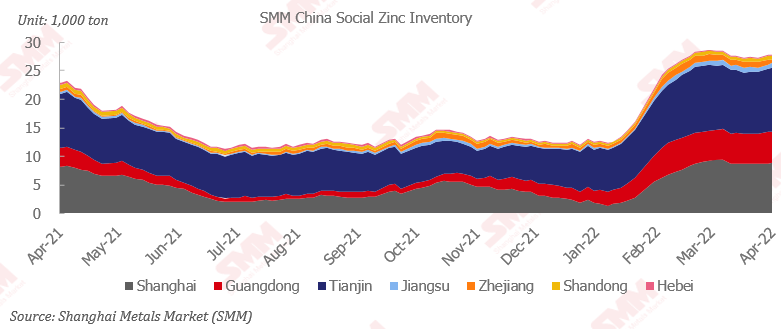

SMM China Zinc Inventory in Major Markets Rose 5,200 mt on Week

Total zinc ingots inventories across seven major markets in China stood at 278,000 mt as of April 8, up 5,200 mt from April 1, down 300 mt from March 6. Domestic inventories increased. Overall, the market inventory remained unchanged under the impact of the pandemic. In Shanghai market, there were no shipments from warehouses due to the pandemic prevention and control measures but only a small number of arrivals in some warehouses. Some holders may intend to export with small amount of goods and because of the difficulty in picking up goods, inventory in Shanghai continued to increase. In Tianjin market, the overall arrivals were relatively stable, but the operating rates of downstream were weak and the inventory rose due to the Qingming Festival holiday and transport restrictions in Hebei. In Guangdong market, the arrivals were rather less with slight increase in the inventory. Inventories in Shanghai, Guangdong and Tianjin rose 7,500 mt, and inventories across seven major Chinese markets increased 5,200 mt.

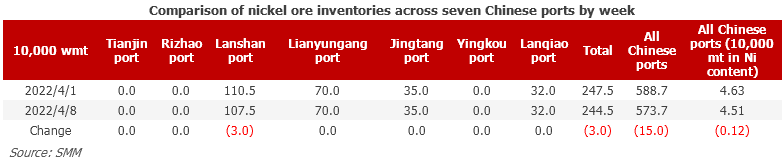

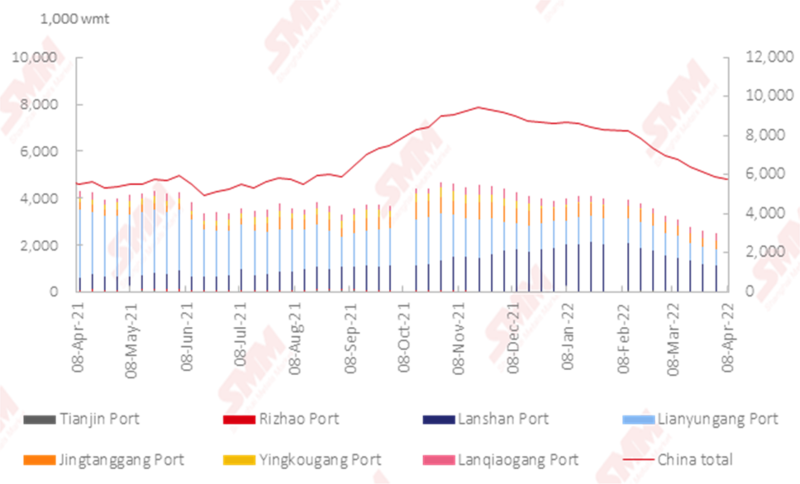

Nickel Ore Inventories at Chinese Ports Fell 150,000 wmt on Week

As of April 8, the nickel ore inventory at Chinese ports dipped 150,000 wmt from a week earlier to 5.737 million wmt. Total Ni content stood at 45,100 mt. The total inventory at seven major ports stood at 2.445 million wmt, 30,000 wmt lower than last week. The decrease in inventory slowed down. At present, the rainy season in the Philippines gradually ends, so the import volume may increase significantly. Besides, the production of domestic manufacturers in some areas was poor due to the pandemic. Therefore, the destocking speed is expected to decline.

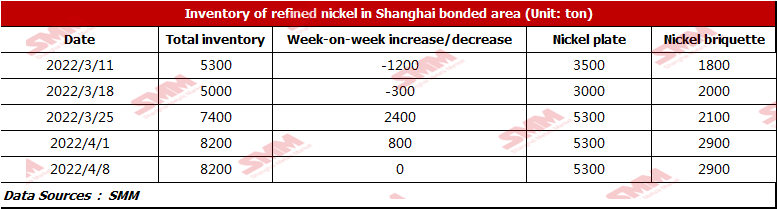

Nickel Inventory in Bonded Zone Changed Little due to the Pandemic in Shanghai

This week, LME and SHFE nickel fluctuated slightly, and the import was at a loss due to the stable spread between the domestic and overseas markets. Nickel inventory in Shanghai bonded zone was 8,200 mt this week. The inventory of nickel briquettes and nickel plates was 2,900 mt and 5,300 mt respectively, flat from last week. Due to the COVID-19 outbreak, the inventory in Shanghai bonded zone changed little. As LME nickel has not gotten rid of the capital game, the import will still be at a loss next week.

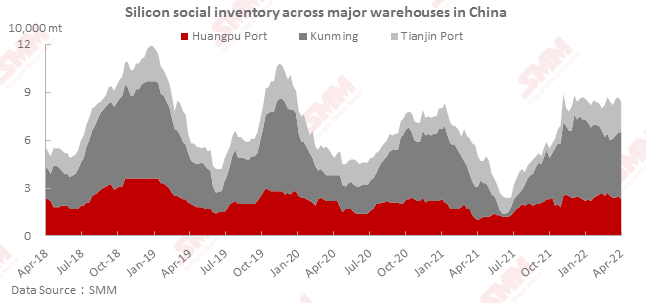

SMM China Silicon Inventory in Major Markets Dropped 3,000 mt on Week

According to SMM's statistics, social inventories of silicon in Huangpu port, Kunming, and Tianjin port totalled 84,000 mt as of April 8, a decrease of 3,000 mt from the previous week. After the Qingming Festival, the shipments at the ports increased compared to the pre-holiday period, but the arrivals were rather less due to transport restrictions and other reasons. The inventory in Tianjin port and Huangpu port both decreased. There was a slight delay in the shipments from Kunming, resulting in a small increase in stocks, and train transportation accounted for over 90% of the goods sent from Kunming to the port due to the road restrictions.

![진롱동업이 오늘 조셀레늄 30톤을 입찰했다 [SMM 셀레늄]](https://imgqn.smm.cn/usercenter/NPpAM20251217171723.jpeg)

![[SMM 코발트 모닝 브리핑] 비수기 수요 부진 지속; 다수 부문 가격 약세로 시장 줄다리기 심화](https://imgqn.smm.cn/usercenter/CIcRv20251217171725.jpg)