A sudden shutdown at Mobarakeh Steel Company and Khouzestan Steel Company has placed nearly one-third of Iran’s crude steel output at risk, threatening to disrupt a key source of semi-finished steel supply in the Middle East. As two cornerstone integrated producers go offline, Iran’s exportable surplus, particularly billets and slabs, is expected to shrink, even as domestic consumption remains largely stable. The resulting shift is likely to tighten regional supply, support semi-finished steel prices, and redirect trade flows as buyers seek alternative sources, amplifying volatility across neighboring markets.

Pre-War Steel Production and Capacity: Large but Underutilized Base

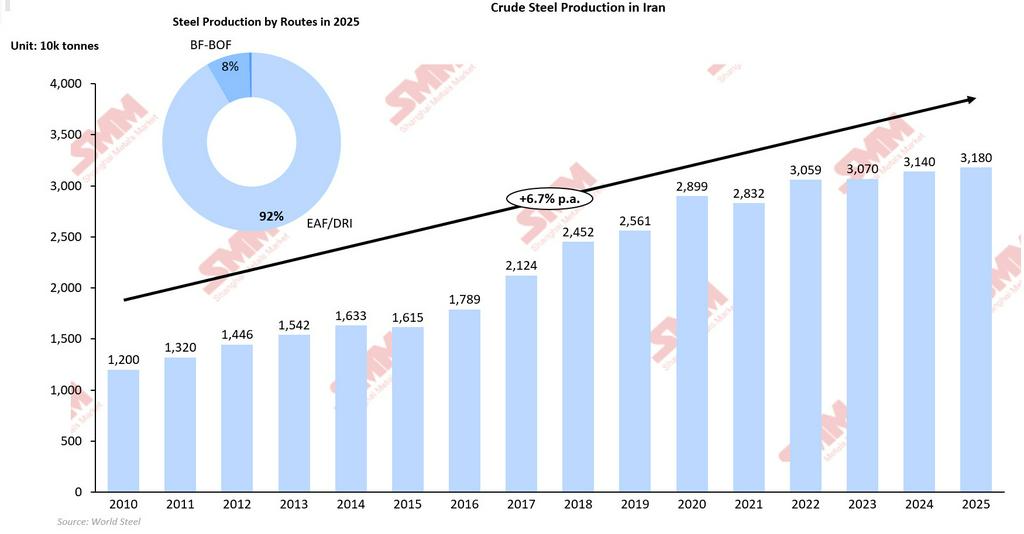

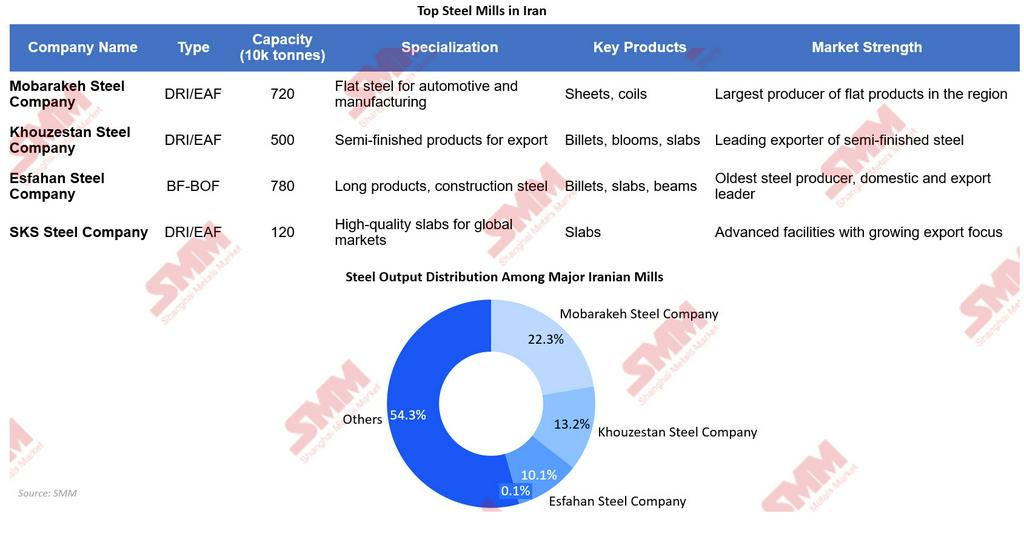

Before the outbreak of the conflict, Iran maintained a sizable but underutilized steel production base. The country consistently ranked among the world’s top ten crude steel producers, with output reaching about 31.8 million tonnes in 2025, representing an average annual growth of 6.7% since 2010. This level of production was achieved against an estimated nominal crude-steel capacity of roughly 58.2 million tonnes, implying a pre-war capacity-utilization rate of only about 53%. The relatively low utilization highlights structural constraints, including sanctions, energy supply limitations, and export logistics, rather than insufficient installed capacity. Iran’s long-term industrial strategy further underscores this surplus capacity structure. Under the Seventh Five-Year Development Plan, the country targeted 55 million tonnes of crude-steel capacity by 2026. By 2024, its crude steel capacity had already reached approximately 51.2 million tonnes, suggesting that the expansion phase was largely completed, but actual output lagged behind installed capacity. This meant the steel sector possessed significant theoretical upside potential, contingent on improvements in energy availability, financing, and export access. The industry structure is highly concentrated, dominated by large state-affiliated and quasi-public producers. Mobarakeh Steel Company, the largest steel producer in the Middle East, and Khouzestan Steel Company together contribute about 35.5% of national crude steel output, forming the backbone of Iran’s integrated steel supply chain. Beyond production, these companies play a critical role in supplying semi-finished steel to domestic rolling mills and generating exportable surplus, particularly in billets and slabs. As a result, any disruption to these key producers has disproportionate implications for Iran’s effective capacity, production levels, and trade balance.

Crude Steel Production Shock: Two Major Core Integrated Producers Cease Operations

On March 27, 2026, U.S.-Israeli strikes hit Mobarakeh Steel Company in Isfahan and Khouzestan Steel Company in Ahvaz, two of Iran’s largest integrated steel complexes. These facilities play distinct but complementary roles in the national steel chain: Mobarakeh primarily produces flat steel for automotive and manufacturing applications, while Khouzestan focuses on semi-finished steel such as billets, blooms, and slabs for export markets. Their operational disruption therefore affects both domestic finished steel supply and export-oriented semi-finished production. Khouzestan Steel produced approximately 4.2 million tonnes of crude steel in 2025 and serves as one of Iran’s leading billet and slab exporters. Mobarakeh Steel produced around 7.1 million tonnes in the same year, making it the largest flat-steel producer in the region and a key supplier to downstream industries. Combined, the two companies account for roughly one-third of Iran’s crude steel output (35.5%). This concentration means that even partial shutdowns at these facilities translate into a meaningful reduction in national production and effective capacity utilization.

Initial damage assessments indicated that production lines were halted, with repairs and output resumption potentially requiring six months to one year depending on spare-part availability and security conditions. The combined affected production capacity is estimated at around 14 million tonnes per year. Although Iran’s installed capacity is geographically dispersed across smaller EAF mini-mills, rebar producers, and semi-integrated sites, Mobarakeh and Khouzestan contribute disproportionately to integrated primary steel output. As a result, the shutdown reduces upstream crude steel availability, tightening feedstock supply for downstream rolling mills and limiting finished steel production even where downstream facilities remain operational.

Structural Vulnerability: Power and Gas Disruptions Amplify the Mill Damage

Beyond the direct physical damage to major steel mills, disruptions to Iran’s energy infrastructure significantly magnify the impact on steel production. Several producers have faced gas and electricity shortages following attacks on the South Pars gas field, a critical source of natural gas supply for the country’s industrial sector. This is particularly important because approximately 92% of crude steel production is based on the DRI–EAF route, making the entire industry structurally sensitive to energy disruptions. Any interruption in gas feedstock directly constrains DRI output, while power shortages limit meltshop operations, jointly reducing crude steel production.

These energy constraints extend the impact beyond the two directly affected mills. Even plants that were not physically damaged may operate at reduced utilization rates due to insufficient gas or unstable electricity supply. This creates a compound shock for the steel sector: direct damage to key integrated facilities, reduced energy availability across the system, and slower restart timelines for interconnected upstream and downstream operations. Consequently, production recovery becomes dependent not only on repairing damaged mills but also on restoring energy infrastructure. Even under a ceasefire scenario, this combination of constraints makes a rapid return to pre-war operating rates unlikely.

Demand Dynamics: Contraction First, Reconstruction Later

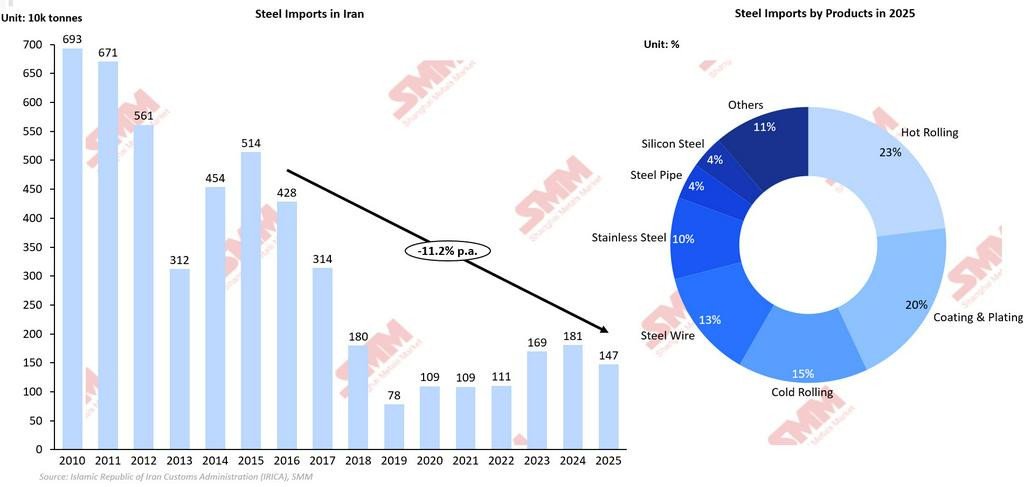

Before the conflict, Iran’s apparent steel consumption showed relatively stable growth, fluctuating around 20-22 million tonnes in recent years with modest long-term expansion. This indicates that domestic demand has been relatively steady and largely driven by construction and infrastructure activity rather than rapid industrial expansion. In practice, Iran has long treated domestic demand as the primary claim on steel bases, with the rest of its output treated as a flexible exportable surplus. This means that when production dips due to technical or external shocks, policy makers and steel producers tend to protect the domestic market, adjusting the outer ring of the value chain rather than allowing acute national shortage. In Iran’s case, production losses are more likely to be absorbed through reduced exports, meaning domestic consumption may remain broadly stable in the short term.

This inward-learning bias is invisible in the trade history of Iran. Over the past decade, rising domestic output coincided with declining steel imports, as the country substituted foreign supply with home-grown capacity. Between 2016 and 2025, for example, steel imports fell by about 11.2% Y-o-Y, even as the domestic economy grew, underscoring a structural preference for covering consumption from internal production whenever feasible. Given that pattern, the current production shock from bombings on major integrated mills is likely to play out as a re‑ordering of priorities, not an immediate collapse of domestic consumption. In this view, apparent steel consumption remains a relatively stable indicator, but it conceals tightening in the upper layers of the supply chain:

-

Downstream users (construction firms, automakers, and machinery producers) may face delivery delays, thinner product ranges, and quality substitutions.

-

The stability of consumption is thus structural and political, a deliberate choice to preserve domestic demand levels, rather than a sign that the underlying shock is minor.

However, over time, structural changes may still emerge. If shutdowns persist and export reductions are insufficient to balance domestic demand, Iran may need to selectively import higher-grade flat or coated products, reversing the logic of its recent industrial‑self‑sufficiency narrative. This would shift Iran’s trade structure toward exporting lower-value semi-finished steel and importing higher-value finished products.. The affected integrated mills were key suppliers of flat steel used in automotive, manufacturing, and pipe applications, segments where the product requirements are more demanding and less easily substituted by the output of smaller EAF‑based mills. Even if these smaller EAF plants remain physically operational, their ability to ramp up production and optimize capacity utilization is constrained by energy shortages. War‑driven damage to power‑generation and gas‑processing infrastructure, including the South Pars gas field and associated grid elements, has created gas and electricity rationing across the industrial sector. Steelmakers that once operated under partial power‑deficit conditions now face tighter allocations, forcing many EAF‑based mills to run partial shifts, staggered production windows, or inefficient operating modes. This energy‑driven cap on utilization means that the dispersed EAF base cannot fully compensate for the loss of high‑grade flat‑steel output from the major integrated complexes, even if the mechanical capacity remains intact. As a result, Iran may continue exporting billets but with a reduced volume, whereas selectively importing higher-value flat and specialty products. In such a scenario, apparent consumption would remain stable, but the composition of supply would shift toward higher imports and fewer exports. Conversely, if domestic demand weakens due to economic disruption, apparent consumption could decline modestly, reflecting both lower production and reduced activity in construction-related sectors.

In the near term, reconstruction provides the most visible source of demand support. War‑damaged steel plants, associated power infrastructure, and logistics nodes require new structural sections, plates, and rebar for rebuilding; urban and industrial‑zone infrastructure damaged nearby generates further demand for construction‑grade steel. This reconstruction cycle can provide a floor to demand and support consumption in basic steel segments. However, reconstruction demand is neither immediate nor sufficient to fully offset earlier losses. It typically emerges with a time lag and depends on fiscal capacity, security conditions, and the pace of project mobilization. As such, its contribution is gradual rather than immediate. At the same time, underlying demand conditions are weakening. War-related damage to industrial facilities and logistics networks directly interrupts production and delays procurement across downstream sectors. The impact on the automotive supply chain, particularly linked to the Sefiddasht facility, a subsidiary of Mobarakeh, further weakens demand for flat steel products used in vehicles, machinery, and manufacturing.

In the medium term, the weakening of commercial and private‑sector demand may counteract the reconstruction‑driven buildup. The broader economic environment, characterized by currency volatility, sanctions‑related financing constraints, heightened uncertainty, and rising inflation, discourages private‑sector construction, real‑estate investment, and industrial expansion. Unlike physical damage, which is localized, weaker investment sentiment affects demand across the entire economy. Even sectors not directly impacted by the conflict may reduce steel consumption due to cautious capital allocation and uncertain demand expectations. Developers may delay new projects, automobile OEMs may cut back on production runs, and machinery producers may postpone capex plans, all of which reduce the steel tied up in discretionary projects. This softening of commercial demand is particularly visible in the upper echelons of the value chain, where speculative construction and high‑end manufacturing investment are most sensitive to credit conditions and macroeconomic risk. This downside pressure offsets part of the reconstruction-driven demand, suggesting that overall steel consumption is more likely to remain broadly stable or decline modestly rather than increase sharply.

More importantly, state‑priority and strategic demand sits at the top of the allocation hierarchy. The state has a strong incentive to protect military‑industrial infrastructure, strategic energy projects, and critical transport nodes, ensuring that steel flows to facilities that support national security and essential services. This priority layer of demand is likely to be insulated from price and scarcity through formal and informal allocation rules, preferential access, and potential subsidies, even if other users face higher costs and longer lead times. The outcome of this three‑way tug‑of‑war is that Iran’s total steel demand in 2026 as a whole is likely to remain broadly flat or decline modestly, rather than expand. Importantly, this dynamic helps explain why apparent steel consumption may appear relatively stable despite underlying weakness. Policy priorities and supply reallocation can preserve domestic availability in the short term, masking softer end-user demand. In reality, the adjustment occurs beneath the surface, with weaker commercial activity offset by delayed but emerging reconstruction needs.

Overall, the most probable outcome is that Iran’s apparent steel consumption stays broadly stable in the short term, with slight downside risk. The interaction between reconstruction demand and weaker commercial investment keeps demand from collapsing, while production losses are absorbed primarily through reduced exports and selective imports. This implies that the production shock reshapes trade flows and supply composition more than it significantly alters total domestic steel consumption.

Trade Flows Under Pressure: Export Capacity Loss Meets Logistics Disruption

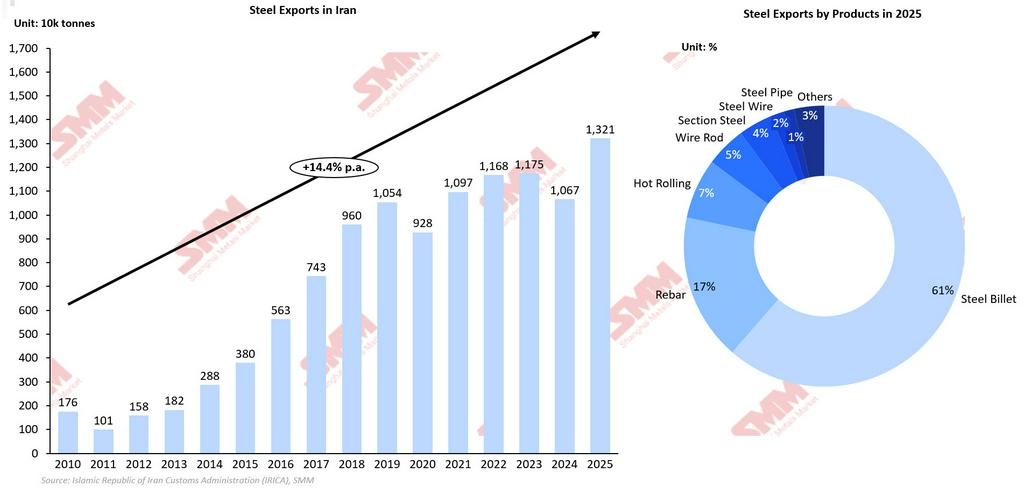

Iran has long operated as a net exporter of steel, with its overseas shipments heavily concentrated in semi‑finished products and construction‑related steel. In 2025, exports were dominated by roughly 8.1 million tonnes of billets, 2.2 million tonnes of rebar, and about 0.9 million tonnes of hot‑rolled products, flowing primarily to neighboring Gulf countries and broader Middle Eastern markets. These regional buyers have relied on Iranian billets as a competitive feedstock for their own downstream rolling mills and on Iranian rebar and hot‑rolled steel for infrastructure and construction projects. The entire structure of these export flows is closely tied to the output profiles of Mobarakeh Steel Company and Khuzestan Steel Company, both of which serve as core nodes for high‑grade flat‑steel and large‑scale semi‑finished production. The shutdown of these two complexes therefore does not merely trim a marginal portion of Iran’s overseas shipments; it directly reduces the country’s effective export capacity, particularly for billets and higher‑grade flat products that are difficult to replicate at scale through smaller, dispersed mills.

The immediate consequence of the war‑driven disruption is a sharp compression of export volumes, especially in the segments that are most dependent on integrated‑mill output. Billet and flat‑steel availability tightens in the near term, forcing regional buyers in the Gulf and across the Middle East to seek alternative suppliers such as Saudi Arabia, the UAE, India, and China. As these markets diversify their procurement, Iran’s share in regional trade may temporarily weaken, particularly in the higher‑quality flat‑steel and premium‑grade construction segments where the country once held a strong price‑quality advantage. This shift reflects the upstream nature of production shock, where constraints in crude steel output propagate directly into export reductions.

Logistics constraints further compound the trade‑flow shock, adding a second layer of disruption on top of the mill‑shutdowns and energy rationing. In the early phase of the conflict, Iran effectively closed the Strait of Hormuz, later permitting limited passage for vessels carrying essential goods under strict coordination protocols. This created uncertainty in shipping schedules, increased insurance costs, and disrupted normal trade channels, all of which tightened the execution capacity of steel exports. Even if some mills remain operational and can produce exportable volumes, the ability to ship those volumes reliably to regional markets is constrained by higher freight premiums, longer lead times, and route‑diversion risks. The steel sector consequently faces a triple shock: a reduction in export capacity due to the shutdown of key integrated mills, a disruption in the logistical network that supports the movement of steel, and an energy‑driven cap on the utilization of smaller EAF‑based plants. These factors significantly constrain Iran’s steel trade flows in the short term, reshaping the regional balance of supply and demand and altering the way the country positions itself within the global steel‑trade ecosystem.

Market Impact: Short-term Reduction in the Supply of Semi-finished Steel from Iran

The suspension of Mobarakeh Steel Company and Khouzestan Steel Company is expected to reduce Iran’s exportable surplus rather than immediately affect domestic consumption. Even with a temporary ceasefire, steel production recovery is unlikely to be swift, as repairs to integrated facilities and supporting infrastructure may take months. This delay is likely to tighten supply in semi-finished steel markets, particularly for billets and slabs, where Iran has traditionally been a key regional supplier. In the near term, Iran will likely cut export volumes to prioritize domestic supply, reducing availability to Middle Eastern buyers and providing moderate price support in regional semi-finished markets.

Several structural factors could prolong the disruption.

-

Security risks: Continued hostilities could delay reconstruction and prolong production losses.

-

Technology and sanctions constraints: Limited access to equipment and spare parts may reduce repair efficiency and capacity utilization.

-

Fiscal pressure: Reconstruction and defense spending may delay investment and slow capacity recovery

Domestically, steel prices may firm due to tighter feedstock availability, but consumption is expected to remain stable as exports adjust first. If the shutdown persists, Iran may selectively increase imports of higher-grade flat and coated products, while maintaining exports of lower-grade long steel. Overall, the most probable market outcome is reduced Iranian exports, stable domestic demand, modest regional price support, and a temporary shift in trade flows toward alternative suppliers.

![[Peru Made Final Affirmative Anti-dumping Ruling on Wire Rod from China]](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)

![[SMM HRC Daily Trading] Spot Cargo Moved Sideways](https://imgqn.smm.cn/usercenter/fljuJ20251217171715.jpg)