Entering late April 2026, China's spot aluminum market exhibited core characteristics of "elevated inventory, intensifying arrivals, regional divergence, and widening price spreads." With only one week remaining before the Labour Day holiday, under the combined effects of the lifting of the loading ban, accelerated clearance of backlogs into warehouses, concentrated release from upstream plant warehouses, and cautious downstream stocking, the upward trend in China's aluminum ingot inventory was difficult to reverse, approaching the high level of 1.5 million mt. Meanwhile, the spot price spread between south China and east China continued to widen, cross-regional transshipment economics emerged, and a restructuring of regional cargo flows was imminent.

I. Social Inventory Continued to Rise, with Arrival Pressure Intensifying Across All Consumption Regions

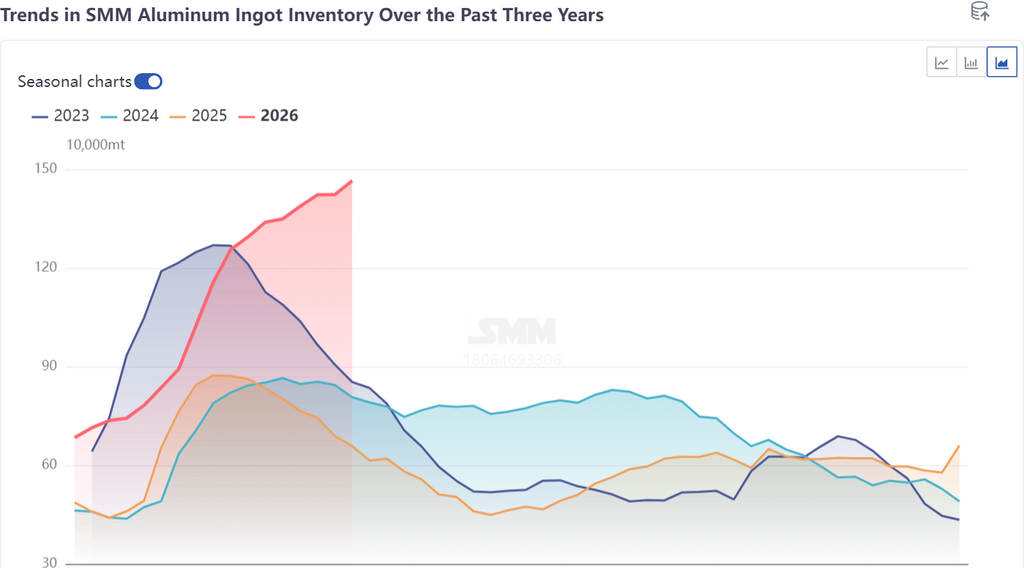

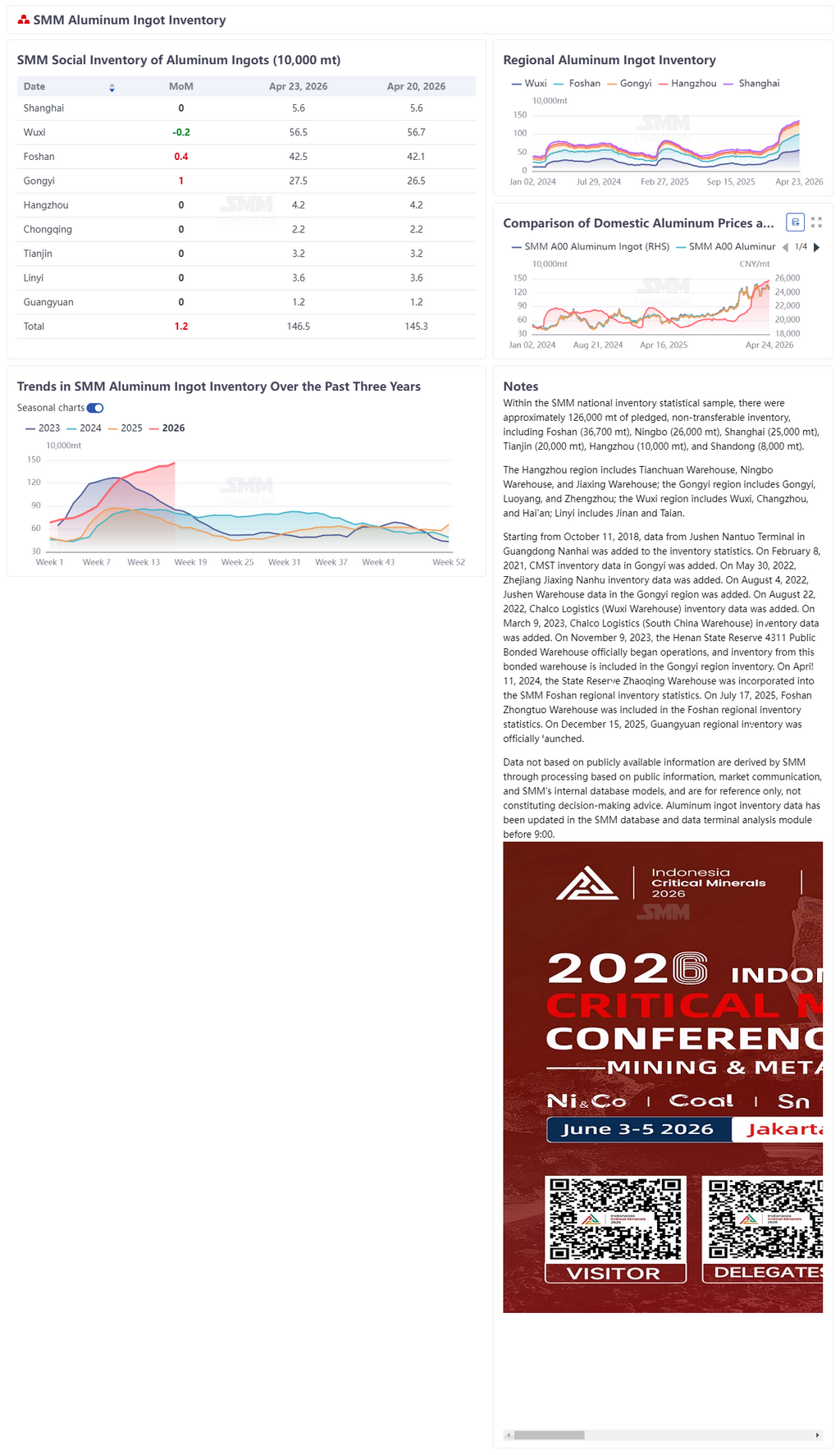

According to SMM statistics, as of April 24 (Thursday), aluminum ingot social inventory across China's major consumption regions stood at 1.465 million mt, up 42,000 mt WoW from Thursday, marking consecutive weeks of inventory buildup, with the buildup magnitude expanding further WoW. Weekly warehouse withdrawals rebounded slightly by 14,200 mt WoW to 115,200 mt, but the improvement in withdrawals fell short of recent arrival increments, and destocking momentum was clearly insufficient.

II. Recent Inventory Pressure Showed a Pattern of "Severe in East China, Fluctuating in Central China, and Persistent in South China"

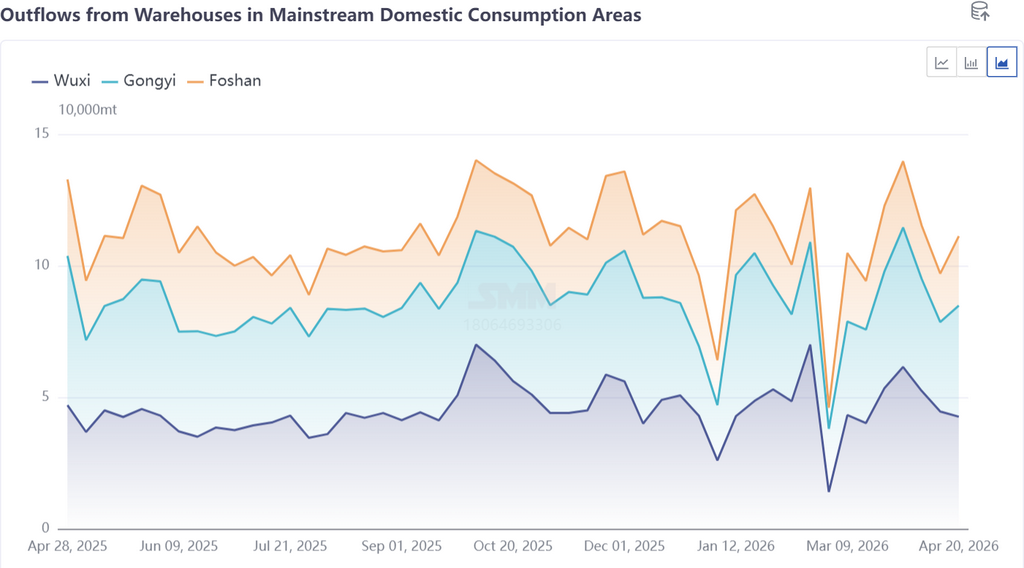

East China (Wuxi): Previously affected by the loading ban, upstream shipments were restricted and in-transit volumes declined, with brief and modest destocking occurring mid-week. However, after the ban was lifted, previously backlogged cargo flowed into warehouses in a concentrated manner, with an estimated 30,000–40,000 mt of backlog still remaining. Combined with the accelerated warehousing of these backlogged cargoes ahead of the Labour Day holiday, inbound pressure is expected to rise significantly over the next one to two weeks, with strong inventory buildup expectations.

Central China (Gongyi): During the loading ban period, northern cargo was diverted here, causing inventory to build up again notably this week after a prior destocking inflection point. Regional inventory pressure surged, but as the backlog situation had already been fully resolved earlier, subsequent inventory pressure is expected to be relatively moderate.

South China (Foshan): Spot warehouse withdrawals remained sluggish, upstream plant warehouses in south-west China released inventory in a concentrated manner, and combined with accelerated clearance of yard backlogs ahead of Labour Day, inventory continued to climb. As the Guangdong-Shanghai price spread widened, cross-regional transshipment opportunities began to open up. Some upstream producers in south-west China had already reduced shipments to the Foshan area. The current backlog of less than 10,000 mt is expected to be fully cleared before the Labour Day holiday, and subsequent arrival pressure in south China is expected to ease steadily.

III. Market Outlook: Inventory Buildup Pressure to Persist, Inflection Point Still Awaited — Focus on Three Core Variables

Overall, approaching month-end and the Labour Day holiday, arrival pressure across China's major consumption regions is expected to remain significant. Although aluminum prices rebounded slightly after a sharp decline from highs during the week, downstream buy-the-dip restocking enthusiasm was moderate, driving some improvement in warehouse withdrawals, but this was not enough to support destocking in China. Current operating aluminum capacity in China stayed high, with strong supply-side rigidity, while downstream demand remained at just-needed levels. High aluminum prices suppressed restocking enthusiasm, and demand recovery was lackluster during the off-peak to peak season transition. The widening Guangdong-Shanghai price spread drove the initiation of cross-regional transshipment and restructuring of regional cargo flows, but this was unlikely to alter the overall inventory landscape in the short term.

SMM believes that a trend inflection point for China's aluminum social inventory remains difficult to form at present, and aluminum ingot inventory is expected to approach the high level of 1.5 million mt around the Labour Day holiday. Going forward, three core variables warrant close attention:

Downstream operating stability during the off-peak to peak season transition: Operating performance in sectors such as architectural profiles, PV, and automotive will determine the strength of demand recovery and the magnitude of improvement in warehouse withdrawals.

Export order release intensity: Against the backdrop of tight global aluminum supply, the release of aluminum semis export orders from China will directly or indirectly affect the pace of domestic destocking.

Spot transactions and price spread dynamics: Whether spot transaction activity in south China and east China can recover after the holiday, along with the sustainability of regional price spreads, will determine the scale of cross-regional transshipment and the progress of regional inventory rebalancing.

![Guangdong-Shanghai Price Spread Widens, Pre-Holiday Cross-Regional Transshipment Economics Emerge [SMM Analysis]](https://imgqn.smm.cn/production/admin/votes/imagesqsDLb20240416161800.jpeg)