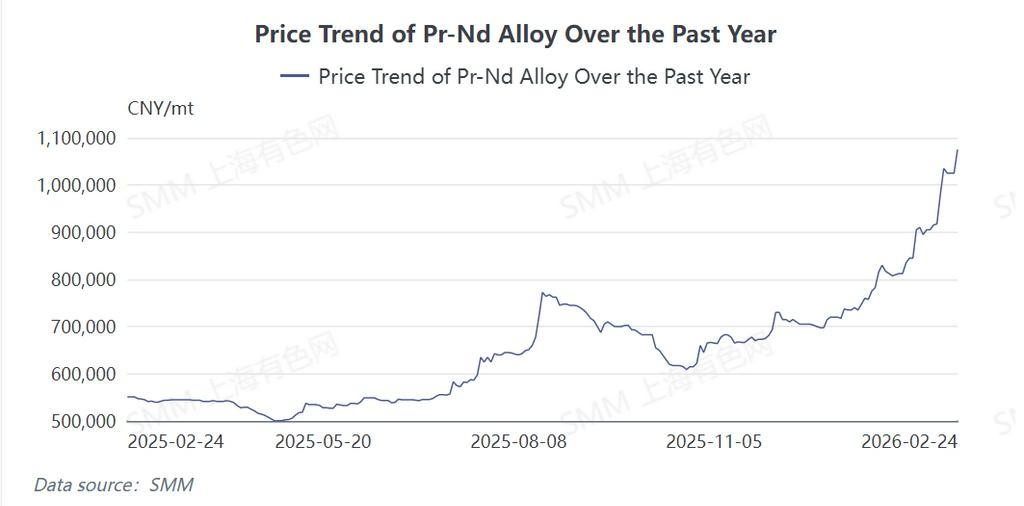

【SMM News】 Influenced by multiple factors, light rare earth prices surged dramatically today. The market quotation for praseodymium-neodymium oxide is in the range of 880,000 - 890,000 yuan/tonne, representing an increase of approximately 35,000 yuan/tonne compared to pre-holiday levels, a rise exceeding 4.12%. This marks a staggering 98% increase year-on-year. The quotation for praseodymium-neodymium metal stands at 1.07 - 1.08 million yuan/tonne, up by 50,000 yuan/tonne (4.88%) from pre-holiday prices, also reflecting a 95% year-on-year increase. The sharp spike in raw material prices on the first trading day of the new year has caught downstream permanent magnet and motor manufacturers, who have not fully resumed operations, off guard. Although some companies anticipated the upward trend before the holiday, the reality of the price hike led many magnetic material producers to exclaim in surprise as they commenced post-holiday market trading. In response to this price fluctuation, SMM analysts conducted a special market survey to explore the practical impacts of sustained rare earth price increases on the magnetic material and motor segments.

I. Magnetic material enterprises provided varying feedback.

The rise in rare earth oxide and metal prices primarily impacts magnetic material manufacturers. However, feedback from these producers varies significantly following this price surge.

Firstly, leading magnetic material enterprises, represented by Jingli Permanent Magnet, Zhenghai Magnetic Material, and Zhongke Sanhuan, maintained relatively high operating rates during the Spring Festival holiday. Having generally stocked up on raw materials at lower pre-holiday prices, and with overseas order demand not significantly reduced during the holiday period, these leading companies maintained stable production. Their long-term order agreements, locked in advance, have limited the impact of today's price increase and potential volatility for the rest of the month on their operations. Market transactions for these head enterprises are stabilizing as post-holiday operating rates gradually increase.

Secondly, some non-leading producers face a different situation. Constrained by already high pre-holiday raw material costs, their operating rates had been consistently low, with profit margins steadily eroded. Consequently, they opted for extended holiday breaks to avoid immediate price impact. This strategy has afforded them a more ample time window to observe subsequent market price movements.

Thirdly, some companies that have resumed operations adopted a more aggressive approach, choosing to raise their product quotations in line with market prices. These firms, primarily stronger mid-tier enterprises, are also under cost pressure but have decided to follow the price hike immediately based on an optimistic outlook for future price trends. Their small-scale pre-holiday stockpiles also provide some buffer and bargaining leverage in price negotiations with downstream customers, giving them confidence to engage in pricing battles.

Lastly, a group of cautious enterprises has chosen to temporarily maintain pre-holiday quotations. These producers generally view the current surge as a short-term phenomenon, likely to recede due to sluggish downstream transactions. The scant inquiries from motor manufacturers and end-users on the first workday further supports their rationale for holding prices steady, with a "wait-and-see" attitude being the common response. In summary, magnetic material producers exhibited diverse reactions on the first post-holiday workday.

Nonetheless, continuous monitoring, close tracking, and maintaining high sensitivity to raw material price changes will be the central theme for this segment this week.

II. Persistent Cost Concerns from Motor Manufacturers

In contrast to the varied feedback from magnetic material producers, motor manufacturers express more uniform and profound concern regarding this round of rare earth price increases. Many resumed permanent magnet motor manufacturers explicitly report feeling greater cost pressure.

For the permanent magnet motor industry, sustained rare earth price hikes signify not just a direct increase in production costs but, more profoundly, introduce severe volatility into the entire rare earth industrial chain's pricing system. This sharp price fluctuation poses a significant challenge to the supply chain stability of permanent magnet synchronous motors (PMSMs). Multiple companies indicate they can accept moderate price increases but cannot withstand drastic and unpredictable swings. End-users persistently weigh cost-reduction technical alternatives, making a relatively stable pricing environment crucial for motor manufacturers.

Even if prices rise, sufficient buffer and adaptation time for the downstream market are deemed necessary. Some leading new energy vehicle traction motor manufacturers are particularly concerned about future cost pressures. Their apprehension lies in the fact that prices have already soared despite demand not being fully unleashed. Should demand recover concentrately later, prices could climb to unpredictable heights, drastically amplifying cost pressures.

More worryingly, a rapid price decline after peaking would create immense difficulties in inventory management and production planning. Although, from a technical standpoint, PMSM technology remains mature, reliable, and offers superior comprehensive performance compared to non-magnet motor alternatives, the extreme instability of raw material prices is substantively eroding the market competitiveness and supply chain health of this technology route.

Finally, SMM forecasts that rare earth raw material prices will experience high-level volatility this week, keeping prices for NdFeB permanent magnets elevated. It is recommended that downstream manufacturers across the board continue to closely monitor upstream raw material price trends, carefully assess market direction, and conduct procurement transactions opportunistically. For any assistance with market insights, please feel free to contact SMM Senior Rare Earth Analyst, Sofia.

SMM Senior Rare Earth :Sofia Shi

Email Address:shixin@smm.cn

![Policy Tailwinds Combined with Rising Expectations of Improving Demand, Rare Earth Permanent Magnets Concept Strengthened, Xiangdian Co. Hit Daily Limit [SMM Express]](https://imgqn.smm.cn/usercenter/AJTtH20251217171744.jpg)

![Rare Earth Export Prices Saw Slight Correction This Week as Geopolitical Tensions and Supply Chain Restructuring Accelerated [SMM Rare Earth Ex-China Weekly Review]](https://imgqn.smm.cn/usercenter/UXEpx20251217171743.jpeg)