Introduction

Depuis des décennies, les déchets d’aluminium sont échangés dans le monde entier comme une matière recyclable classique, les flux commerciaux étant principalement dictés par les prix, les coûts logistiques et la dynamique régionale de l’offre et de la demande. Cependant, avec l’importance croissante de la transition énergétique, de la fabrication bas carbone et de la sécurité des ressources, la valeur stratégique des déchets d’aluminium est en train d’être réévaluée à l’échelle mondiale.

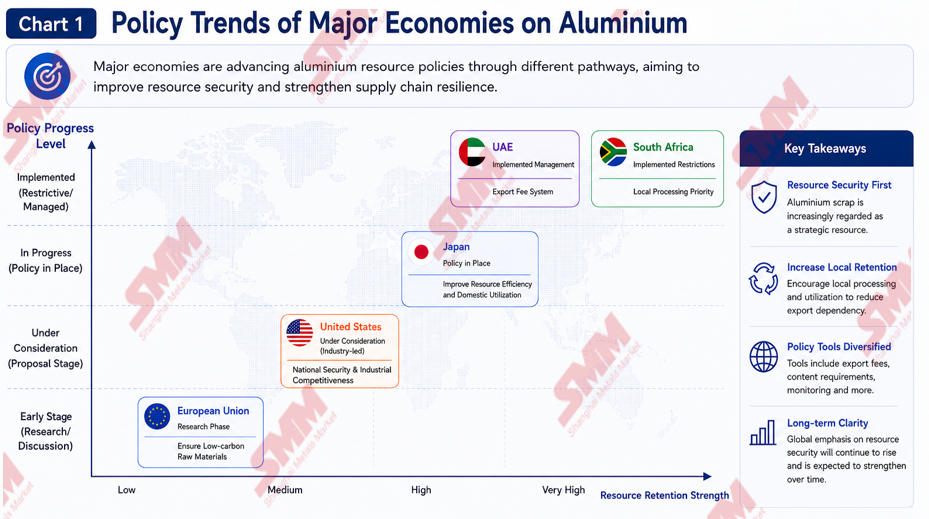

De la réflexion de l’Union européenne sur des restrictions à l’exportation des déchets, à l’appel de l’industrie américaine de l’aluminium pour classer les déchets comme un actif stratégique, en passant par les efforts du Japon pour renforcer les systèmes d’économie circulaire et la mise en place par les Émirats arabes unis de taxes à l’exportation des déchets métalliques, les grandes économies redéfinissent progressivement le rôle des déchets d’aluminium au sein des chaînes d’approvisionnement industrielles.

Pour les marchés asiatiques qui dépendent fortement des déchets importés pour produire de l'ADC12 et des alliages d'aluminium secondaires, cette tendance pourrait devenir un facteur important influençant la disponibilité future des matières premières et les coûts de production.

Pourquoi les déchets d'aluminium deviennent-ils une ressource stratégique ?

L'importance croissante des déchets d'aluminium est étroitement liée aux efforts mondiaux de décarbonation. Par rapport à la production d'aluminium primaire, l'aluminium secondaire ne nécessite généralement qu'environ 5 % de la consommation d'énergie tout en réduisant les émissions de carbone d'environ 95 %. Alors que des secteurs comme les véhicules électriques, les infrastructures électriques, la construction, l'emballage et la fabrication avancée poursuivent des objectifs de réduction de carbone de plus en plus ambitieux, l'aluminium recyclé est devenu une voie essentielle pour la décarbonation industrielle.

Parallèlement, les tensions géopolitiques, les perturbations des chaînes d'approvisionnement, la volatilité des marchés de l'énergie et les préoccupations croissantes concernant la résilience industrielle ont incité les gouvernements à réévaluer la sécurité des approvisionnements en matières premières critiques. Les déchets d'aluminium sont donc de plus en plus considérés non pas comme une simple matière recyclable, mais comme un intrant industriel stratégique capable de soutenir la fabrication à faible émission de carbone, la sécurité des chaînes d'approvisionnement et la compétitivité industrielle à long terme.

Alors que les gouvernements accordent davantage d'importance à l'autonomie stratégique et à la résilience des ressources, le commerce mondial des déchets d'aluminium passe progressivement d'un modèle purement dicté par les prix à un modèle de plus en plus influencé par les objectifs politiques et les considérations de sécurité des ressources.

1. Union européenne : défendre les ressources en déchets à l'ère du MACF

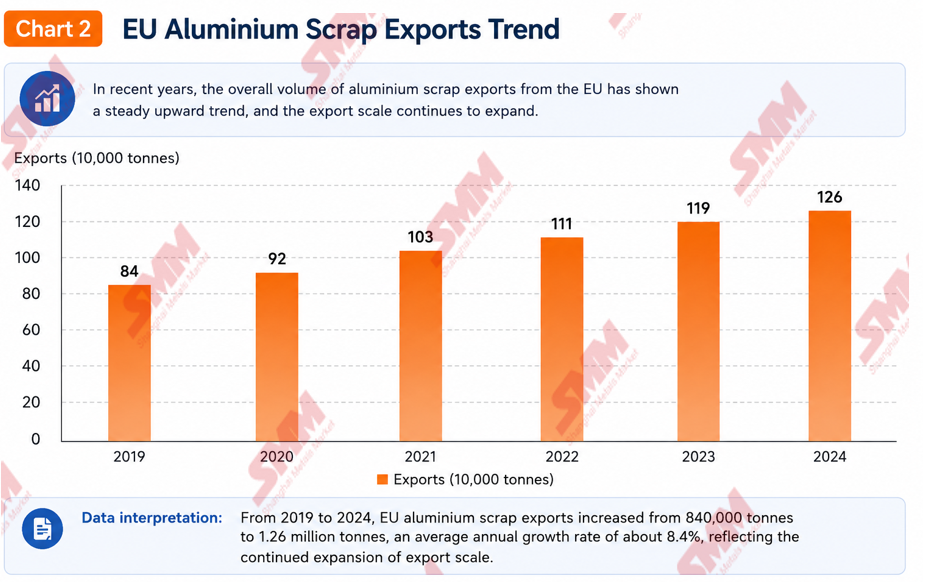

L'Union européenne est actuellement l'une des régions les plus surveillées du marché mondial des déchets d'aluminium.

Selon les estimations du secteur, les exportations de déchets d'aluminium de l'UE sont passées d'environ 840 000 tonnes en 2019 à environ 1,26 million de tonnes en 2024, soit une croissance de près de 50 % en cinq ans. Une part importante de ces matériaux a été expédiée vers des destinations telles que l'Inde, la Turquie, la Malaisie, la Thaïlande et d'autres marchés asiatiques.

Cette tendance suscite des inquiétudes croissantes chez les producteurs européens d'aluminium. European Aluminium a fait valoir que les exportations continues de déchets de haute qualité affaiblissent la compétitivité de l'industrie de recyclage domestique en Europe. L'association a souligné que certaines capacités de production d'aluminium secondaire en Europe restent sous-utilisées malgré d'importants volumes de ferraille de valeur quittant la région.

Cette question est étroitement liée aux stratégies industrielles et climatiques plus larges de l'UE. Des initiatives telles que le Pacte vert pour l'Europe, la loi sur l'industrie nette zéro et le mécanisme d'ajustement carbone aux frontières (MACF) ont considérablement accru l'importance des matières premières à faible teneur en carbone dans les chaînes d'approvisionnement manufacturières européennes.

Le MACF, qui est entré dans sa phase transitoire en 2023 et entrera dans sa phase définitive en 2026, exigera que les produits en aluminium importés supportent des coûts liés au carbone en fonction de leurs émissions de production. Dans ce contexte, l'aluminium recyclé a gagné en importance stratégique en raison de son empreinte carbone nettement plus faible.

Comparé à la production d'aluminium primaire, l'aluminium secondaire ne nécessite qu'environ 5 % de l'énergie tout en réduisant les émissions de carbone d'environ 95 %. En conséquence, l'aluminium recyclé est de plus en plus considéré comme l'une des voies les plus efficaces pour les efforts de décarbonation de l'industrie de l'aluminium.

Pour les fabricants européens, augmenter la teneur en matières recyclées contribue non seulement à réduire l'empreinte carbone des produits, mais peut également atténuer les futurs coûts liés au MACF. Alors que des secteurs tels que les véhicules électriques, l'emballage, la construction et les énergies renouvelables accélèrent leur transition bas carbone, les déchets d'aluminium évoluent progressivement d'un matériau recyclable conventionnel vers une ressource industrielle stratégique.

Par conséquent, European Aluminium a préconisé des mesures plus fortes pour conserver les ressources en ferraille en Europe. L'une des propositions les plus suivies est la recommandation de l'association d'un droit d'exportation de 30 % sur les déchets d'aluminium. Les partisans soutiennent que des coûts d'exportation plus élevés pourraient accroître la disponibilité de la ferraille sur le marché intérieur et renforcer l'industrie du recyclage en Europe.

Dans ce contexte, la Commission européenne a lancé des consultations ciblées sur les exportations de déchets d'aluminium et évalue les mesures potentielles dans le cadre du futur plan d'action REsourceEU. Les instruments politiques actuellement à l'étude comprennent des droits d'exportation, des systèmes de licence d'exportation, des mécanismes renforcés de surveillance des exportations et des exigences accrues en matière de contenu recyclé.

Cependant, ces propositions ont rencontré une opposition du secteur du recyclage. En mai 2026, Recycling Europe, conjointement avec le Bureau of International Recycling (BIR) et plusieurs autres organisations professionnelles, a soumis une lettre conjointe à la Commission européenne s'opposant aux restrictions à l'exportation de déchets d'aluminium. Ces groupes soutiennent que l'Europe ne fait pas face à une pénurie structurelle de déchets et avertissent que les contrôles à l'exportation pourraient nuire aux recycleurs, réduire les investissements et affaiblir l'économie circulaire.

Bien que le résultat final de la politique reste incertain, l'accent mis par l'UE sur l'augmentation de l'utilisation domestique des ressources en déchets devient de plus en plus clair.

2. États-Unis : Les déchets d'aluminium entrent dans le cadre de la sécurité nationale

Aux États-Unis, les discussions autour des déchets d'aluminium ont de plus en plus dépassé le recyclage pour entrer dans le débat plus large sur la compétitivité manufacturière, la résilience de la chaîne d'approvisionnement et la sécurité nationale.

En 2025, l'Aluminum Association a publié son livre blanc intitulé Scrap the Exports, Save U.S. Supply, décrivant les déchets d'aluminium comme un actif stratégique. Le rapport soutient que conserver davantage de déchets aux États-Unis pourrait renforcer les chaînes d'approvisionnement domestiques, réduire la dépendance aux importations et soutenir la croissance industrielle à long terme.

Selon l'association, environ 85 % de l'aluminium produit aujourd'hui aux États-Unis est de l'aluminium secondaire dérivé de déchets recyclés. Malgré cette forte dépendance aux matériaux recyclés, le pays continue d'exporter environ 2 millions de tonnes de déchets d'aluminium par an.

L'association estime également que les États-Unis font face à un déficit annuel d'approvisionnement en aluminium primaire d'environ 4 millions de tonnes. Dans ce contexte, conserver davantage de déchets générés localement est de plus en plus considéré comme un moyen rentable de renforcer la sécurité de la chaîne d'approvisionnement et de réduire la dépendance aux métaux importés.

Les groupes industriels soutiennent que la demande croissante des véhicules électriques, des infrastructures électriques, des centres de données, de l'aérospatiale et de la fabrication de défense nécessitera un meilleur accès aux ressources domestiques en déchets. En conséquence, l'association a appelé à la rétention prioritaire des flux de déchets de haute qualité tels que les canettes usagées (UBC), les déchets prêts pour le laminoir et les déchets industriels.

Les UBC sont considérées comme l'une des catégories les plus précieuses en raison de leur rôle dans les systèmes de recyclage en boucle fermée, tandis que les déchets prêts pour le laminoir peuvent être directement introduits dans les opérations de fusion avec un minimum de traitement. Les déchets industriels générés lors de la fabrication sont également très appréciés en raison de leur qualité et de leur composition constantes.

En revanche, l'association a adopté une position plus prudente concernant les flux de déchets mélangés de qualité inférieure tels que le Zorba et le Twitch, arguant que les restrictions sur ces matériaux pourraient créer des goulets d'étranglement logistiques et décourager les investissements dans les infrastructures de tri et de traitement.

Bien qu'aucune restriction formelle à l'exportation n'ait été introduite, le débat lui-même reflète un changement significatif dans la réflexion politique. Les déchets d'aluminium sont de plus en plus considérés non seulement comme un matériau recyclable, mais aussi comme une ressource stratégique capable de soutenir la compétitivité industrielle et les objectifs de sécurité nationale.

3. Japon : Renforcer la sécurité des ressources par l'économie circulaire

Contrairement à l'Union européenne et aux États-Unis, le Japon n'envisage pas actuellement de droits d'exportation, de systèmes de licences d'exportation ou d'interdictions d'exportation pour les déchets d'aluminium. Au lieu de cela, le pays se concentre sur le renforcement de la sécurité des ressources par le développement de l'économie circulaire et une plus grande utilisation des matériaux recyclés.

En tant que nation pauvre en ressources et fortement dépendante des matières premières importées, le Japon a longtemps considéré la sécurité des ressources comme un élément clé de la politique industrielle. Les perturbations de la chaîne d'approvisionnement mondiale et l'incertitude géopolitique croissante ont encore renforcé cette priorité.

En 2026, le Japon a introduit un nouveau Plan d'action pour l'économie circulaire, visant environ 1 000 milliards de yens d'investissements liés à l'économie circulaire d'ici 2030. L'initiative vise à améliorer la productivité des ressources, à augmenter les taux de recyclage et à renforcer la résilience industrielle tout en réduisant la dépendance aux matières premières importées.

L'industrie japonaise de l'aluminium promeut également une plus grande utilisation de l'aluminium recyclé et bas carbone. L'un des exemples les plus notables est la collaboration entre Toyota et UACJ sur les systèmes de recyclage de véhicules en boucle fermée, qui récupèrent l'aluminium des véhicules en fin de vie et le réintroduisent dans la fabrication automobile.

Parallèlement, la Japan Aluminium Association a souligné à plusieurs reprises l'importance de l'aluminium vert, du recyclage et de l'efficacité des ressources pour soutenir les objectifs de neutralité carbone du pays.

Bien que le Japon reste attaché aux principes du libre-échange et qu'il soit peu probable qu'il introduise des restrictions directes à l'exportation dans un avenir proche, une demande domestique plus forte d'aluminium recyclé pourrait progressivement réduire la disponibilité à l'exportation au fil du temps.

À cet égard, l'influence du Japon sur les futurs flux de déchets d'aluminium pourrait passer par une consommation domestique accrue plutôt que par une intervention réglementaire.

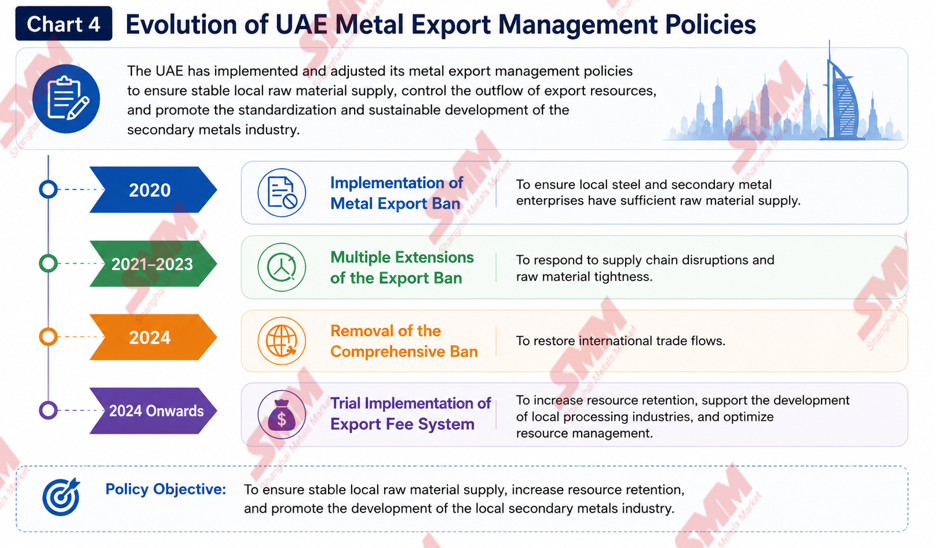

4. EAU : De l'interdiction d'exportation au système de frais d'exportation

Les EAU représentent l'un des exemples les plus pratiques de politiques de rétention des ressources déjà mises en œuvre.

En tant que plaque tournante régionale majeure pour les déchets ferreux et non ferreux, les EAU ont introduit des restrictions à l'exportation des déchets métalliques pendant la période pandémique pour soutenir les fabricants domestiques confrontés à des pénuries de matières premières et à des perturbations de la chaîne d'approvisionnement.

Entre 2020 et 2023, le pays a prolongé à plusieurs reprises les restrictions à l'exportation de déchets pour garantir une disponibilité suffisante de matières premières pour les industries locales. Cependant, plutôt que de maintenir une interdiction d'exportation permanente, le gouvernement s'est ensuite orienté vers une approche basée sur le marché.

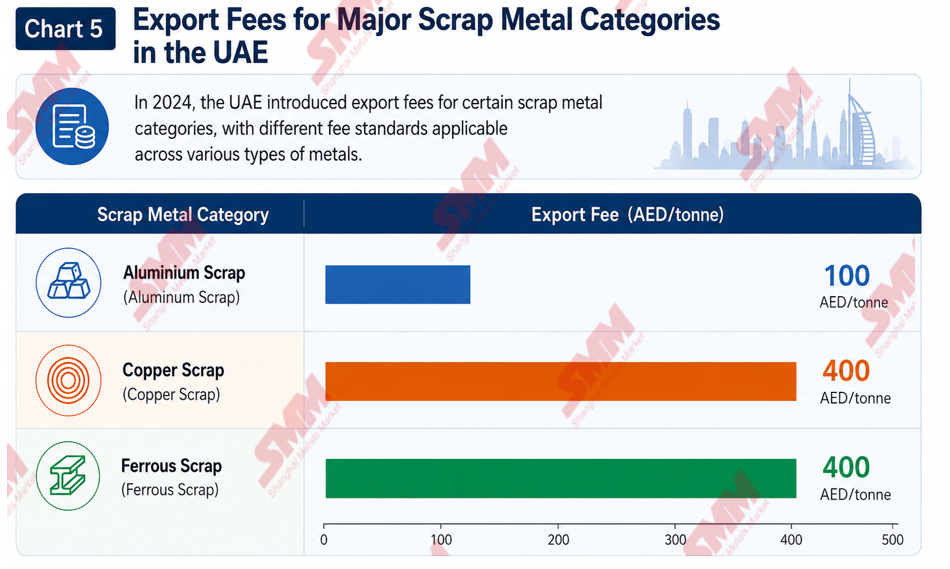

En 2024, les EAU ont officiellement remplacé leur interdiction d'exportation par un système de frais d'exportation. Les frais actuels comprennent 100 AED par tonne pour les déchets d'aluminium et 400 AED par tonne pour les déchets de cuivre et ferreux.

Comparé à une interdiction d'exportation complète, le système de frais permet au commerce international de se poursuivre tout en encourageant davantage de matériaux à rester sur le marché domestique. La politique reflète un changement plus large des restrictions administratives vers une gestion des ressources basée sur le marché.

L'approche des EAU cherche à équilibrer la sécurité des ressources, le développement industriel et le commerce international. Alors que la demande de métaux recyclés continue de croître dans les secteurs de la construction, de l'emballage, du transport et des énergies renouvelables, les déchets sont de plus en plus considérés comme des ressources industrielles stratégiques plutôt que comme de simples marchandises commerciales.

L'expérience des EAU est de plus en plus considérée comme un cas de référence pour d'autres pays explorant des moyens de conserver des ressources précieuses en déchets sans perturber complètement les flux commerciaux internationaux.

5. Afrique du Sud : Prioriser la transformation domestique

L'Afrique du Sud fournit un autre exemple de politiques de rétention des ressources mises en œuvre pour soutenir le développement industriel domestique.

Ces dernières années, le pays a renforcé les contrôles sur les exportations de déchets métalliques et introduit des mesures visant à prioriser la transformation locale. En 2022, l'Afrique du Sud a mis en œuvre une interdiction d'exportation des déchets métalliques couvrant plusieurs catégories de déchets métalliques.

La politique a été conçue pour améliorer la disponibilité des matières premières pour les fabricants domestiques et soutenir la production locale à valeur ajoutée. Les autorités sud-africaines ont fait valoir que l'exportation de grands volumes de déchets peut générer des revenus commerciaux à court terme, mais ne contribue guère à soutenir l'industrialisation et la croissance de l'emploi.

Contrairement à l'accent mis par l'Union européenne sur la décarbonation ou à l'accent mis par les États-Unis sur la sécurité de la chaîne d'approvisionnement, la politique de l'Afrique du Sud est largement centrée sur le développement industriel, l'ajout de valeur et la création d'emplois.

L'expérience du pays démontre que les politiques de rétention des ressources ne se limitent pas aux économies développées. De plus en plus, les marchés émergents cherchent également à conserver davantage de ressources recyclables au sein de leurs écosystèmes industriels domestiques.

Point de vue de SMM

Bien que les approches politiques adoptées par l'UE, les États-Unis, le Japon, les EAU et l'Afrique du Sud diffèrent considérablement, elles pointent toutes vers la même tendance sous-jacente : les déchets d'aluminium sont de plus en plus reconnus comme une ressource stratégique plutôt que comme une simple marchandise recyclable.

À l'heure actuelle, la plupart de ces mesures ne sont pas susceptibles de provoquer une perturbation immédiate des flux commerciaux mondiaux. Cependant, la direction du mouvement devient de plus en plus claire. Les gouvernements et les organisations industrielles accordent une plus grande importance à l'utilisation domestique des ressources, à la résilience de la chaîne d'approvisionnement et au développement industriel bas carbone.

Pour les acteurs du marché, la question clé n'est pas de savoir si les politiques changent, mais si ces politiques modifieront finalement les flux de ressources. Si davantage de déchets de haute qualité restent dans les régions productrices comme l'Europe et l'Amérique du Nord, la concurrence pour les qualités de déchets haut de gamme pourrait s'intensifier sur les marchés internationaux.

Cette tendance est particulièrement pertinente pour les producteurs d'ADC12 et les fonderies d'aluminium secondaire qui dépendent de matières premières importées. Dans les années à venir, le suivi des développements politiques pourrait devenir tout aussi important que le suivi des prix de l'aluminium, des taux de fret ou des taux de change.

En fin de compte, le marché mondial des déchets d'aluminium entre dans une nouvelle phase où le prix, la politique et la sécurité des ressources deviennent de plus en plus interconnectés. Dans un tel environnement, l'accès à des chaînes d'approvisionnement stables en déchets pourrait s'avérer être l'un des avantages concurrentiels les plus importants pour les producteurs d'aluminium secondaire.

![Le marché des lingots d'aluminium à l'étranger diverge : le marché américain est fort, tandis que le Japon et la Thaïlande sont faibles [Analyse SMM]](https://imgqn.smm.cn/usercenter/kVTpA20251217171654.jpg)