[Conflict Impact]

The outbreak of the Middle East conflict on February 28, 2026, significantly disrupted global aluminum market dynamics, driving increased volatility in aluminum prices.

Aluminum prices on the London Metal Exchange (LME) surged alongside escalating tensions, rising from an Official Price of $3,156.5/mt on February 27 to a peak of $3,519.5/mt in early March. Prices later retreated to the $3,200–3,300/mt range in late March, as market sentiment gradually stabilized.

On March 28, in response to attacks on Iranian industrial zones, Iran reportedly targeted major regional aluminum producers including Aluminum Bahrain and Emirates Global Aluminum, while Qatar Aluminum declared force majeure. These developments constrained primary aluminum output in the Middle East, tightening market liquidity and increasing supply uncertainty.

As a result of supply disruptions, global aluminum availability declined, particularly impacting regions outside China in Asia. Entering April, LME aluminum prices rebounded to $3,400–3,500/mt, breaking above $3,600/mt in mid-April and fluctuating within the $3,500–3,600/mt range.

[Shipping Disruptions]

The conflict initially disrupted transportation systems across the Middle East, with the Strait of Hormuz being most severely affected. Key aluminum exporters—including the UAE, Saudi Arabia, Qatar, Iran, and Kuwait—faced significant logistical constraints.

Exports that traditionally passed through the Strait were heavily restricted, forcing market participants to adopt alternative logistics routes, including land transport to Red Sea ports. These adjustments significantly increased freight costs and extended delivery lead times.

In April, the escalation of conflict into the Red Sea region further limited alternative shipping routes. Most Europe–Asia vessels opted to reroute via the Cape of Good Hope, driving both freight costs and transit times higher.

According to SMM market research, cargo delivery delays reached 3–5 weeks, while container freight costs surged by as much as 60–70%.

[Primary Aluminum and Processing]

Reduced Middle Eastern exports tightened primary aluminum supply across major Asian consuming countries, particularly Japan, Thailand, India, and South Korea.

In 2024, the Middle East exported 6.408 million mt of primary aluminum and key aluminum products, with these four countries accounting for approximately 20.8% (1.331 million mt). In 2025, exports declined to 6.071 million mt, with imports from these countries totaling approximately 1.215 million mt (~20%).

Demand for primary aluminum alloys and billets (notably 6xxx series) remained strong. SMM data shows that following the outbreak of conflict, processing fees for 6063 billets in Southeast Asia rose from $200–250/mt to $250–300/mt, peaking at $300–310/mt.

Market feedback indicates a recovery in demand for 6xxx billets, with both domestic and export transactions in Malaysia and Thailand increasing significantly in April. Downstream purchasing sentiment improved, offsetting weaker market conditions observed in January–February.

Demand for primary foundry alloys also strengthened. Elevated aluminum prices, reduced Middle Eastern supply, and growth in downstream sectors such as automotive (particularly in Thailand) drove increased enquiries for alloys including A356, AlSi10MnMg, and AlSi10FeMg.

Notably, interest in low-carbon aluminum has also increased, reflecting rising alignment with international decarbonization policies such as the EU’s Carbon Border Adjustment Mechanism (CBAM). Against a backdrop of tightening primary supply, importing semi-finished aluminum products from alternative regions may become an increasingly viable option.

[Secondary Aluminum]

Beyond primary production, the Middle East has also been a significant supplier of aluminum scrap and secondary alloys, serving as an emerging recycling and processing hub prior to the conflict.

India and South Korea are key importers of Middle Eastern scrap. In 2024, the region exported 628,000 mt of aluminum scrap, with India and South Korea accounting for 62.6% and 13.5%, respectively. In 2025, total exports rose to 766,000 mt, with imports reaching 489,000 mt (India) and 101,000 mt (South Korea).

Amid the conflict, buyers from Japan and South Korea diversified sourcing toward Southeast Asia, particularly Malaysia and Thailand, boosting demand for ADC12 secondary aluminum alloy. This shift supported both Southeast Asian FOB prices and Japan CIF prices.

In April, continued conflict escalation drove additional demand from India, with SMM data indicating several thousand tonnes of incremental enquiries and transactions in Southeast Asia.

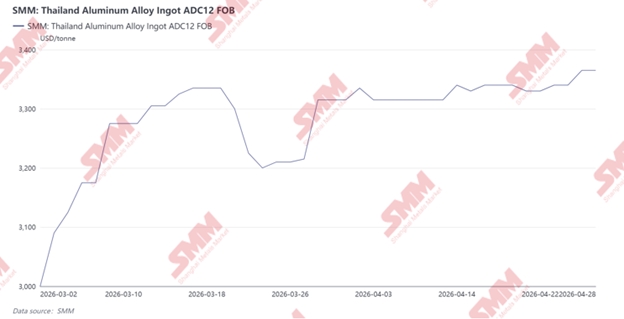

SMM began tracking ADC12 FOB prices in Thailand and Malaysia in March 2026. Prices rose from $3,000/mt on March 2 to $3,365/mt by April 27, marking an increase of $365/mt. Market activity remained robust, with strong exports to Japan, South Korea, and India, alongside steady shipments to China, Singapore, and other regions. Some producers have reportedly secured orders through late June to July.

On the raw materials side, rising LME aluminum prices pushed both imported and domestic scrap prices higher. In Thailand, aluminum cable scrap reached THB 115,000–120,000/mt ($3,560–3,710/mt) in April, significantly increasing blending costs for billet producers.

As scrap prices climbed, some billet producers reduced scrap usage and increased reliance on primary aluminum. Meanwhile, higher prices for Tense scrap led to reduced trading volumes, prompting ADC12 producers to substitute alternative scrap types, including higher-copper materials, to optimize cost structures.

Reduced scrap supply from the Middle East also intensified competition, particularly as India increased procurement from alternative markets, tightening supply and driving prices higher in Southeast Asia.

[Outlook]

The Middle East conflict has fundamentally reshaped aluminum trade flows across Asia and globally, increasing pressure on Southeast Asia’s aluminum processing sector.

If the conflict persists, global aluminum trade is likely to become more regionalized, with tighter raw material availability in Asia and stronger internal circulation in Western markets.

China may emerge as a key balancing supplier, as widening domestic-international price spreads could open export arbitrage opportunities for semi-finished aluminum products and secondary alloys.

However, Southeast Asia may face mounting pressure from raw material shortages and intensified competition, particularly from India. At the same time, tightening low-carbon policies and Western supply chain reshoring may further challenge regional competitiveness.

Conversely, a de-escalation of the conflict and normalization of logistics routes could ease supply constraints, potentially placing downward pressure on aluminum product and secondary alloy prices, gradually returning the market toward pre-conflict conditions.

[Notes]

The “18 Middle Eastern countries” referenced in this report include:

Gulf Cooperation Council (GCC):

Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, Bahrain

Levant region:

Israel, Jordan, Lebanon, Syria, Palestine

Other key regional countries:

Iran, Iraq, Turkey, Egypt, Cyprus, Libya, Yemen

Primary aluminium and related key aluminium products include the following HS codes:

- 7601 – Unwrought aluminium

- 7604 – Aluminium bars, rods and profiles

- 7605 – Aluminium wire

- 7606 – Aluminium plates, sheets and strip, thickness > 0.2 mm

- 7607 – Aluminium foil

- 7608 – Aluminium tubes and pipes