The Strait of Hormuz is the world's most critical energy transit chokepoint, carrying approximately 21% of global oil trade. Southeast Asia's dependence on Middle Eastern oil imports, estimated at roughly 60% of the region's total oil supply, has 1left fossil-fuel-intensive economies acutely vulnerable to the current disruption. Entering 2026, the escalation of geopolitical conflict in the Middle East and the resulting obstruction of this transit corridor has precipitated genuine energy and inflationary crises across the region. The surge in international oil prices has directly impacted electricity supply in the Philippines, where more than 1.2 million off-grid households face rotating blackouts lasting 8 to 16 hours per day, and insufficient grid reserve capacity has crystallized into a substantive energy crisis. In Southeast Asia, the pass-through of fossil fuel cost inflation has been even more severe. Disruption to international supply chains has driven Cambodia's domestic diesel retail prices up 84% from pre-conflict levels, with regular gasoline prices rising 41.5%. Neighboring Laos has been equally hard hit: a 99.7% surge in fuel import costs in a single month pushed Laos's March inflation rate to 9.7%, a new eleven-month high.

Under an extreme oil price scenario such as USD 150 per barrel, the generation cost of power systems predominantly reliant on diesel or heavy fuel oil could exceed 0.15 to 0.20 $/kwh, given the dominant weight of fuel costs in the total cost structure of thermal generation. At the same time, according to calculations by the International Renewable Energy Agency (IRENA), the global weighted average levelized cost of energy (LCOE) for utility-scale ground-mounted solar PV has fallen to approximately 0.043 $/kwh. Against this cost structure comparison, solar PV has not only established a significant economic advantage but has further reinforced its strategic position within the global energy system.

Brent Crude Futures: April 21, 2026

Data source: Investing.com

Solar PV as a Fossil Fuel Substitute: Cost Economics

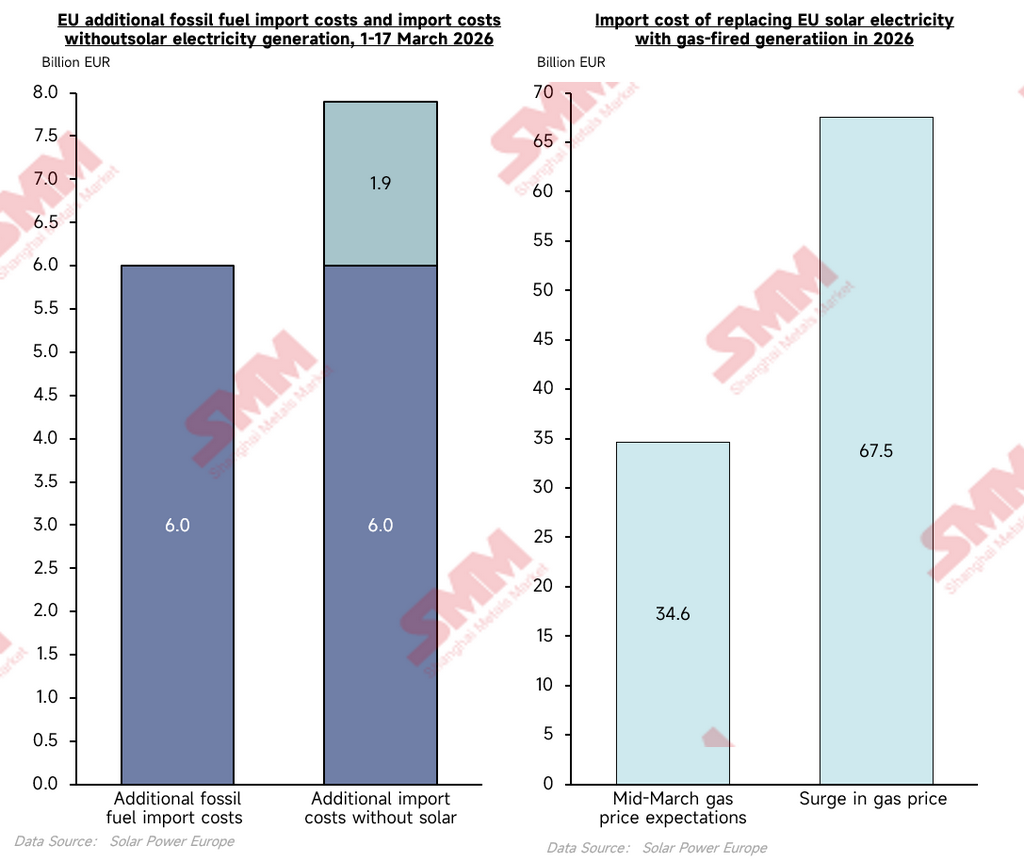

To quantitatively assess the practical utility of solar PV as a price buffer instrument during an energy crisis, using March 1 to March 17, 2026 as the measurement window and under the scenario in which the current level of installed solar PV capacity was in place, actual additional fossil fuel import expenditure for the EU over this period was measured at EUR 6.0 billion (source: SolarPower Europe). Under the comparative counterfactual model, which removes the incremental solar PV generation from the system, additional import costs would have risen directly to EUR 7.9 billion. The empirical data demonstrates that over the first seventeen days of the crisis, solar PV generation actually offset approximately EUR 1.9 billion in additional fossil fuel import expenditure for the EU, at a daily hedging rate of EUR 112 million, representing a total reduction in fossil energy import costs of 32%. Further stress testing of extreme scenarios reveals a non-linear amplification of the substitution benefit. Using mid-March 2026 natural gas price expectations as the baseline, EU solar generation this year is projected to save approximately EUR 34.6 billion in import costs; under an extreme scenario in which natural gas prices double, the cost-hedging benefit of solar expands commensurately to approximately EUR 67.5 billion. Forward projections indicate that by 2030, cumulative savings from this substitution effect could reach up to EUR 170 billion. This empirical logic is fully applicable to Southeast Asian markets that are highly dependent on external energy supply: the greater the severity of the geopolitical energy crisis, the more pronounced the economic multiplier effect of solar PV assets in offsetting imported inflation.

Data source: SolarPower Europe

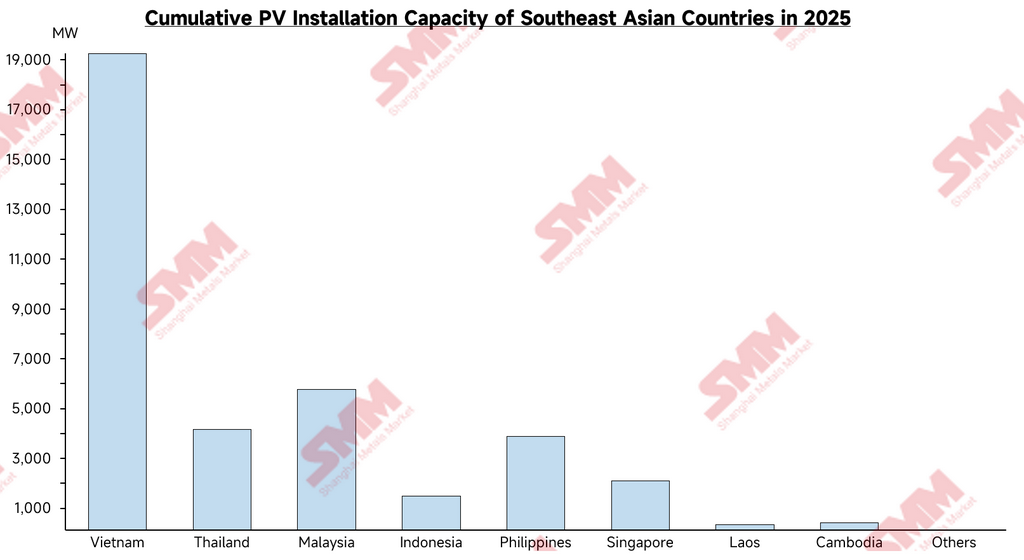

Solar PV Installed Capacity Status and Latest Policy Targets Across Major Southeast Asian Economies

Cumulative solar PV installed capacity across the region varies considerably, with a structure broadly characterized by a small number of leading markets alongside a larger group of early-stage markets. Installed capacity is concentrated predominantly in Vietnam, Malaysia, the Philippines, and Thailand, while certain economies with large populations remain materially underserved in terms of solar development.

Data source: IRENA, processed by SMM model

Vietnam: Leading Installed Scale but Entering an Adjustment Phase

Feed-in tariff policies implemented between 2019 and 2021 drove explosive short-term growth in installed capacity, establishing Vietnam as Southeast Asia's largest solar market. However, grid infrastructure development lagged materially behind, resulting in persistent curtailment in certain regions. Following the expiration of the subsidy regime, new project development slowed considerably. The market is currently awaiting the introduction of new power purchase agreement mechanisms and updated tariff policies.

Philippines: Rapidly Growing Demand and Distributed Market Expansion

The Philippines has long maintained one of Asia's highest electricity tariff levels, which significantly enhances the economic viability of self-consumption solar for commercial and industrial users. In recent years, the progressive implementation of the Green Energy Auction mechanism and the gradual expansion of corporate power purchase agreements have rapidly expanded the project development pipeline, establishing the Philippines as one of the most outstanding growth markets for solar in Southeast Asia.

Indonesia: Installed Capacity Significantly Mismatched with Economic Scale

As Southeast Asia's largest economy, Indonesia's cumulative solar PV installed capacity remains at a relatively low level. The dominance of coal-fired generation in the power mix and the government's application of strict regional quota controls to solar projects have suppressed the competitiveness of solar, while grid transmission stability and logistics challenges have also inhibited solar market development to a certain extent.

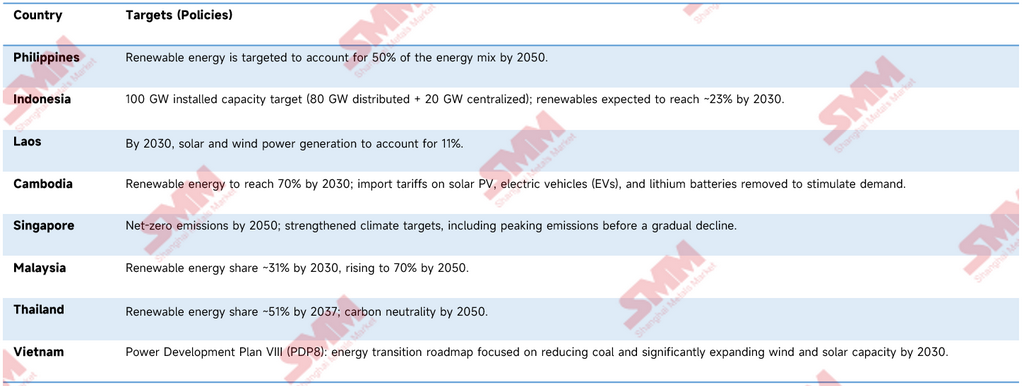

Energy Security Pressures Driving Accelerated Regional Policy Adjustment

Against the backdrop of heightened Middle Eastern tensions and rising transit risk through the Strait of Hormuz, increased volatility in international oil and gas prices has once again highlighted the structural risk of Southeast Asia's heavy dependence on energy imports. In this context, multiple countries have revised renewable energy development targets upward and, through measures such as expanding solar tender volumes, improving power purchase agreement mechanisms, and introducing tax incentives, are accelerating the structural transformation of their energy mix and reducing dependence on fossil fuels.

Chart: Renewable Energy Targets by Country

To achieve macroeconomic energy transition targets and accelerate relief from current geopolitical energy pressures, Southeast Asian countries have taken substantive actions in policy support, administrative approvals, and capital mobilization. For example, the Philippine government recently accelerated administrative approvals for 22 renewable energy projects, including 12 core solar projects; Vietnam's central Gia Lai Province recently formally approved dedicated investment projects totaling USD 190 million; and Cambodia officially implemented a zero-tariff policy on solar systems, lithium batteries, and related renewable energy equipment effective April 1, 2026, with the objective of directly stimulating market demand by reducing import costs. These micro-level acceleration signals confirm that countries are attempting to leverage policy incentives to mobilize industrial capital. The current macroeconomic installation progress and latest official plans for each major economy are set out in the table above.

Analysis of Structural Tensions in Power Systems Under High Solar Penetration

Despite the external momentum provided by the geopolitical crisis and each country's latest revised macroeconomic policies, both of which point toward large-scale solar capacity expansion, the actual rate of the energy transition in Southeast Asia is fundamentally constrained by systemic tensions between high-penetration solar integration and the established commercial models of incumbent national electricity systems. These tensions manifest acutely across three dimensions.

The first is the stock displacement effect on retail electricity revenues. The self-consumption model of commercial, industrial, and residential distributed rooftop solar directly reduces the net electricity purchased from the public grid by high-value customers. In the Philippines, for example, the surge in commercial and industrial installations driven by high retail tariffs has already exerted measurable downward pressure on the sales volumes and profit and loss accounts of both the National Grid Corporation of the Philippines (NGCP) and downstream distribution utilities.

The second is the destruction of peak pricing arbitrage mechanisms by intraday load curve distortion. The output peak of utility-scale solar is structurally coincident with daytime high-load periods. As grid-connected scale expands, large volumes of near-zero marginal cost electricity injected into the grid directly compress and in some instances invert peak electricity prices. This dynamic fundamentally erodes the profit foundation of incumbent state-owned power companies that rely heavily on peak pricing premiums.

The third is the external misallocation of system balancing redundancy costs. The strong intermittency and variability of solar output compels the grid to additionally configure large-scale peaking units, energy storage facilities, and spinning reserves. Currently, these significant ancillary service investments and grid flexibility upgrade costs are borne almost entirely unilaterally by state-owned grid enterprises. In the absence of well-designed transmission access pricing or capacity payment mechanisms through which these costs can be allocated to generators and end-users, the financial burden creates a systematic disincentive for grid operators to facilitate solar interconnection, exacerbating the passive attitude of grid entities toward promoting solar grid integration.

Conclusions and Outlook: Policy Regulation Determines the Pace of Transition

The sustained blockade of the Strait of Hormuz and the resulting regional energy scarcity and inflationary pressures have subjected Southeast Asia's energy structure to an indiscriminate stress test. From the inflationary surge in Laos to the grid crisis in the Philippines, combined with the empirical cost savings documented in Europe under analogous crisis conditions, the evidence collectively confirms that solar PV has transcended its framing as a climate protection instrument and has formally emerged as a strategic hard asset for hedging macroeconomic risk and safeguarding national energy supply. The latest round of energy development planning revisions across Southeast Asian countries represents a policy acknowledgment of this asset reclassification.

However, the deep-seated barriers constraining the actual realization rate of solar capacity additions have not been eliminated. The core obstacle remains the institutional resistance of national electricity systems confronted with a fundamental redistribution of economic interests. Indonesia provides a paradigmatic illustration: the substantial gap between the aggressive solar targets embedded in international multilateral financing frameworks and the conservative grid planning posture of the state utility PLN reflects, at its core, an unresolved impasse over the allocation of stranded coal generation assets and the cost burden of grid upgrades.

In market structures where state-owned energy entities exercise absolute control over grid investment and dispatch authority, the critical breakthrough point of the transition is entirely dependent on the political resolve of each country's senior government leadership. Only when governments are able to leverage the forcing mechanism of the current energy crisis to intervene substantively, materially restructuring electricity spot markets, establishing equitable ancillary service cost-sharing frameworks, and providing clear financial compensation mechanisms for the orderly retirement of legacy energy assets, can large-scale solar grid integration advance from policy documents to physical installed capacity.

Over the next two to three years, the pace at which these deep-water electricity sector reforms are implemented will constitute the most critical leading indicator for assessing investment certainty and the addressable market scale of Southeast Asia's solar sector.

![[PV: Italy Allocates 30 MW Quota for Floating PV in Latest FER2 Tender]](https://imgqn.smm.cn/usercenter/ZbnfH20251217171741.jpg)

![[PV: Philippines Advances GW-Scale Solar Pipeline with Terra Solar and SanMar Milestones]](https://imgqn.smm.cn/usercenter/XYkMV20251217171740.jpg)