Tensions in the Middle East have escalated again recently, as the conflict between Israel and Iran continues to intensify, drawing renewed global attention to energy transportation security in the Gulf region. The key transmission channel currently being watched by the market is energy supply, particularly shipping through the Strait of Hormuz. This waterway accounts for roughly one-fifth of global seaborne oil trade, and any disruption to traffic would have a direct impact on global energy supply. Given the high level of uncertainty surrounding the development of the situation, market risks are clearly skewed to the upside. This article provides a brief analysis of how the current conflict may affect the copper market going forward.

From a macroeconomic perspective, the surge in energy prices represents the main transmission mechanism through which the conflict affects the global economy. Rising oil prices not only push up global inflation, but also erode real household income and weigh on consumption, thereby dragging down economic growth. Market estimates suggest that if oil prices remain around $80 per barrel, global GDP growth in 2026 could be reduced by about 0.1 percentage points; if prices temporarily spike to $100 per barrel, the drag could widen to around 0.4 percentage points. At the same time, higher oil prices would also push up overall global inflation, potentially adding between 0.2 and 0.7 percentage points under a high-price scenario. Against this backdrop, markets are repricing expectations for the Federal Reserve’s rate-cutting path and global financial conditions. If energy prices remain elevated, the easing cycle could be delayed, and tighter financial conditions would place pressure on cyclical assets. For the copper market, this macro transmission channel implies short-term downside pressure on prices. As the conflict drives oil prices higher, concerns about inflation and tighter monetary policy have increased, risk appetite has declined, and some speculative long positions have begun to unwind, putting pressure on copper prices. Over the longer term, however, the copper market continues to face structural supply constraints, meaning that the current macro shock is more likely to manifest as sentiment-driven volatility rather than a fundamental reversal of the supply-demand trend.

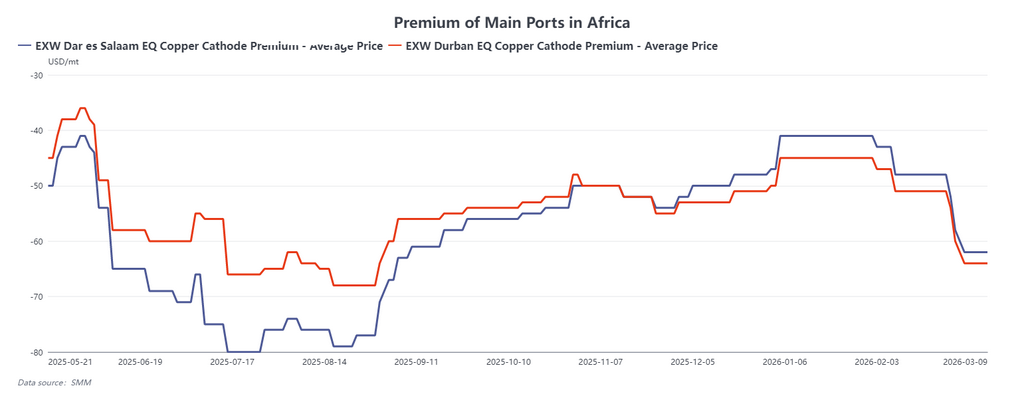

At the same time, developments in the Middle East may affect the copper market through another supply-chain channel: the indirect impact on the hydrometallurgical copper production system in the Democratic Republic of Congo (DRC). A significant portion of DRC refined copper production relies on hydrometallurgical processes, which depend heavily on sulfuric acid supply. According to SMM, sulfuric acid consumption for producing one tonne of refined copper locally ranges from about 2 to 6 tonnes; assuming an average of roughly 4 tonnes, annual sulfuric acid consumption in the DRC is estimated at around 10 million tonnes. The global sulfur trade is closely linked to energy transportation routes, and the Middle East serves both as a critical energy transit corridor and an important node in global sulfur trade. If transport in the Gulf region is disrupted, sulfur trade flows may be affected, potentially pushing up sulfuric acid prices. At present, delivered sulfuric acid prices in the DRC have already exceeded $1,000 per tonne, with a significant supply shortfall still present. Local smelters are reportedly holding only about four to six weeks of inventory. If geopolitical tensions ease in the near term, the impact may remain limited. However, rising raw material costs or tightening supply would increase the risk of production disruptions, potentially affecting the stability of African copper supply and contributing to a rebound in regional copper premiums that had previously been declining.

Overall, the Middle East conflict is affecting the copper market through two main channels. On one hand, higher oil prices are increasing inflationary pressure and tightening financial conditions, weighing on copper and other cyclical assets. On the other hand, if energy and sulfur transport disruptions persist, the cost structure and supply stability of African hydrometallurgical copper production could be affected. The future trajectory of copper prices will therefore depend on the duration of the conflict, movements in oil prices, and changes in global financial conditions, while potential disruptions to African supply chains may emerge as another key variable for the market to watch.