US-India Reach Mutual Tariff Agreement, Substantially Lowering Export Costs for Solar Modules

On February 3, 2026, the United States and India formally signed a bilateral trade agreement, reaching a significant consensus on tariff arrangements for Indian goods exported to the US market. Under the terms of the agreement, the reciprocal tariff rate applicable to Indian goods (including solar modules and energy storage components) was reduced from 25% to 18%.

The core of this adjustment lies in the US side's agreement to eliminate the 25% punitive tariffs previously imposed in response to India's trade relations with Russia, while simultaneously lowering the baseline reciprocal tariff rate. As a reciprocal commitment, India announced its intention to procure USD 500 billion worth of American energy and technology products over the next five years, and to progressively shift its energy import sources away from Russia toward the United States and Venezuela. According to SMM calculations, following these adjustments, the aggregate tariff burden on Indian photovoltaic (PV) modules exported to the US will decline sharply from approximately 50% to 18%, representing a substantial compression of export costs.

US Market Position Continues to Strengthen, India's Market Share Steadily Rising

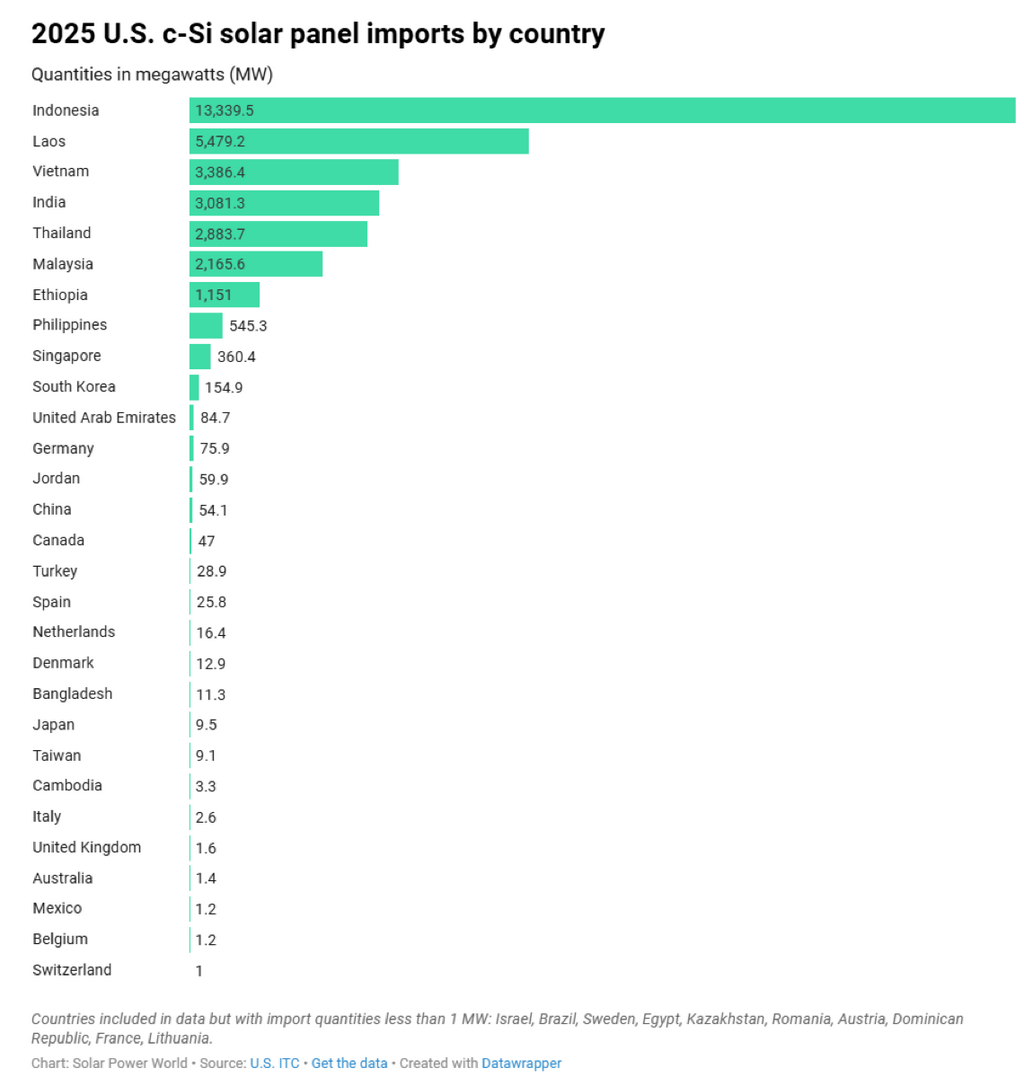

The United States has firmly established itself as the primary destination for Indian solar module exports. According to 2025 US International Trade Commission (ITC) import data for crystalline silicon (c-Si) solar panels, India's position in the US market remains solid: total annual shipments of c-Si modules to the US reached 3,081.3 MW, ranking India as the fourth-largest import source, behind only Indonesia, Laos, and Vietnam. India's market share stands at approximately 9.35%, reflecting a sustained upward trajectory from roughly 3% in 2022, and has become an indispensable component of the US solar supply chain ecosystem.

Source: U.S. ITC

Tightening Domestic Policies Create Urgency for Non-DCR Capacity to Seek Export Outlets

While the external export environment continues to improve, policy constraints within India's domestic market are progressively tightening. Under the confluence of multiple pressures, the domestic absorption capacity for non-DCR (Domestic Content Requirement) modules is expected to contract meaningfully.

- Formal Tightening of the ALMM Policy. Pursuant to regulations issued by India's Ministry of New and Renewable Energy (MNRE), effective June 1, 2026, the vast majority of domestic solar projects will be required to comply with Domestic Content Requirement (DCR) standards under the Approved List of Models and Manufacturers (ALMM), restricting the use of modules assembled with non-indigenous solar cells in utility-scale and government-funded projects. As the implementation date approaches, domestic procurement demand for non-DCR modules is expected to experience a substantive contraction.

- Narrowing Window for Raw Material Tariff Exemptions. The 2026 Union Budget has clarified that the government will retain the Basic Customs Duty (BCD) exemption only for auxiliary PV materials, while the exemption applicable to the core raw material, polysilicon, will be formally terminated on April 1, 2026. Enterprises reliant on imported polysilicon will consequently face a significant increase in production costs.

- Accelerated Development of the Fully Integrated Domestic Supply Chain. Concurrently, the Indian government is actively promoting the development of a fully integrated domestic manufacturing ecosystem through its Production Linked Incentive (PLI) scheme. Under the implementation timeline for the second tranche of PLI, successful bidders are required to complete the construction and commissioning of fully integrated manufacturing facilities by April 2026. Leading enterprises such as Reliance and Adani have already accelerated their upstream capacity buildout in polysilicon and wafer production, further advancing the localization of the industrial supply chain.

Tariff Benefits and Capacity Reorientation Converge, Accelerating the Export Window for Non-DCR Modules

The systematic tightening of domestic policies described above has objectively created an intrinsic impetus for the accelerated reorientation of non-DCR production capacity toward overseas markets. The timely conclusion of the US-India tariff agreement has, in turn, opened a realistic and viable channel through which this excess capacity can be effectively redirected.

The agreement reduces the tariff on Indian modules exported to the US to 18%, and currently imposes no mandatory restrictions on the country of origin of the solar cells contained within the modules. This effectively enhances the price competitiveness of Indian non-DCR modules in the US market. The substantial reduction in tariff costs enables Indian manufacturers to redirect non-DCR capacity, which cannot be absorbed by the domestic market under the constraints of the ALMM policy, toward exports to the United States, thereby achieving effective utilization of existing production capacity.

2026 Market Outlook: Domestic-Export Bifurcation Becomes Increasingly Defined

Taking into account the policy variables outlined above, SMM concludes that India's photovoltaic industry will exhibit a clearly defined domestic-export bifurcation in 2026.

From a timeline perspective, the resumption of polysilicon import tariffs on April 1 will raise production costs for enterprises dependent on imported raw materials; the ALMM restrictions taking effect on June 1 will further compress the domestic sales space available for non-DCR modules. As these two policy measures take effect in succession, DCR-compliant modules are expected to become an increasingly dominant source of supply for the domestic market.

At the same time, the export price advantage generated by the US-India tariff agreement will provide strong momentum for the accelerated concentration of non-DCR capacity toward the US market. SMM anticipates that following the second quarter of 2026, DCR-compliant modules will be directed primarily toward domestic market supply. Meanwhile, driven by both constrained domestic demand and the tariff dividend, non-DCR module export volumes are poised for a significant leap in scale, ushering India's solar exports to the US into a new phase of rapid expansion.

Written by: Ryan Tey Tze Yang

![[SMM PV News] Iraq Cuts Solar Customs Duties to 5% to Spur Adoption](https://imgqn.smm.cn/usercenter/CaHKo20251217171738.jpg)

![[SMM PV News] EU to Unveil 'Buy European' Rules; Strict Local Content Tied to Public Funding](https://imgqn.smm.cn/usercenter/xAoMy20251217171743.jpg)

![Silicon Metal Prices Under Pressure Amid Market Tug-of-War; Polysilicon Market Sentiment Remains Weak [SMM Silicon-Based PV Morning Meeting Minutes]](https://imgqn.smm.cn/usercenter/hIbSC20251217171737.jpg)