Les matériaux métalliques sont largement utilisés dans les composants automobiles, et leurs fluctuations de prix ont un impact significatif sur les structures de coûts. Selon les estimations de SMM, la répartition des coûts d'un véhicule électrique typique est la suivante : batterie de traction (35 %-40 %), moteur de traction et contrôleur (10 %-20 %), carrosserie/châssis/habitacle (30 %) et autres équipements électroniques (7 %). Cette analyse se concentre sur le système du moteur de traction, SMM ayant déjà largement couvert les batteries ailleurs.

Au sein du système moteur (10 %-20 % du coût total du véhicule), les matières premières représentent la plus grande part. Les principaux intrants métalliques comprennent les aimants en terres rares - néodyme-fer-bore (NdFeB) (30 %-35 %), les fils de cuivre émaillés (15 %) et les composants structurels en aluminium (20 %). La hausse simultanée du prix de ces métaux entre fin 2025 et début 2026 a exercé une pression considérable sur les coûts des fabricants de moteurs et des constructeurs de véhicules électriques.

1. Terres rares : La tension sur l'offre et la résilience de la demande font monter les prix

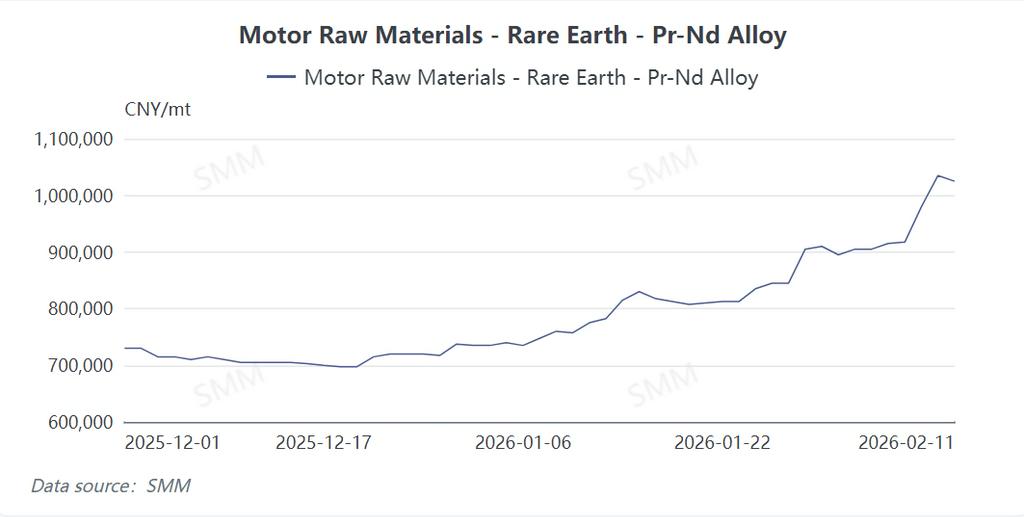

Les prix des terres rares, notamment pour le métal praséodyme-néodyme (PrNd), ont fortement augmenté. Au 9 février 2026, les prix du PrNd ont atteint 975 000–985 000 RMB/tonne, soit une hausse de 33,1 % depuis le début de l'année. Cette accélération résulte d'une offre tendue (production en amont limitée, faible activité de production et disponibilité réduite au comptant en raison des livraisons sur contrat à long terme) et d'une demande robuste (commandes stables à l'étranger pour les matériaux magnétiques et attentes croissantes pour les véhicules électriques et les vélos électriques en 2026). Ces facteurs ont collectivement poussé les prix à la hausse.

Les fabricants de moteurs rencontrent des défis plus importants que les fournisseurs de matériaux magnétiques. Ils doivent absorber non seulement les coûts élevés des terres rares, mais aussi les prix du cuivre. De plus, les fabricants de moteurs peinent à répercuter les hausses de coûts en aval. Les constructeurs de véhicules électriques, confrontés à une concurrence féroce, résistent aux ajustements de prix. Par conséquent, les producteurs de moteurs sont pris en étau entre des pertes croissantes (s'ils poursuivent la production) et une perte de parts de marché (s'ils suspendent leurs activités). Leur faible pouvoir de négociation, dû à la proximité de clients en aval concentrés, exacerbe la pression.

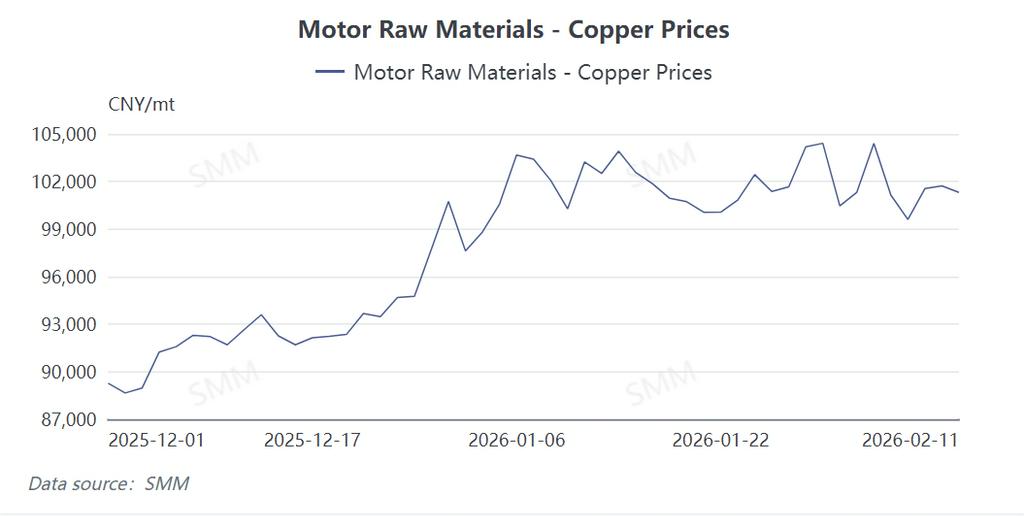

2. Cuivre : Déséquilibre structurel entre l'offre et la demande et facteurs financiers

Les prix du cuivre ont fortement augmenté, passant d'environ 87 000 RMB/tonne fin 2025 à 105 000 RMB/tonne début 2026, soit une hausse de plus de 20 %, et sont restés élevés. Cette hausse a été tirée par :

-

Contraintes de la chaîne d'approvisionnement : des perturbations de la production dans les principaux pays producteurs de cuivre (comme le Chili, le Pérou), des tensions géopolitiques et des goulots d'étranglement logistiques ont limité l'offre à court terme.

-

Influences financières : les conditions de liquidité mondiale et les anticipations inflationnistes ont attiré des capitaux spéculatifs, amplifiant la volatilité des prix.

-

Demande solide : un optimisme soutenu concernant les centres de données et la demande de câbles a en outre soutenu les prix.

L'impact sur les moteurs est direct et significatif. Le cuivre, essentiel pour les enroulements du stator et du rotor, constitue une part substantielle du coût des matières premières des moteurs. La flambée des prix ajoute des centaines de RMB au coût par moteur, ce qui se traduit par des milliards de RMB de dépenses annuelles supplémentaires pour les équipementiers de grande envergure. Cette pression se propage à travers la chaîne d'approvisionnement, comprimant les marges des fournisseurs de matériaux, des fabricants de moteurs et des constructeurs de véhicules. Bien que certaines entreprises de moteurs industriels aient augmenté leurs prix, les équipementiers de véhicules électriques ont jusqu'à présent absorbé les coûts, mettant encore plus à mal leur rentabilité.

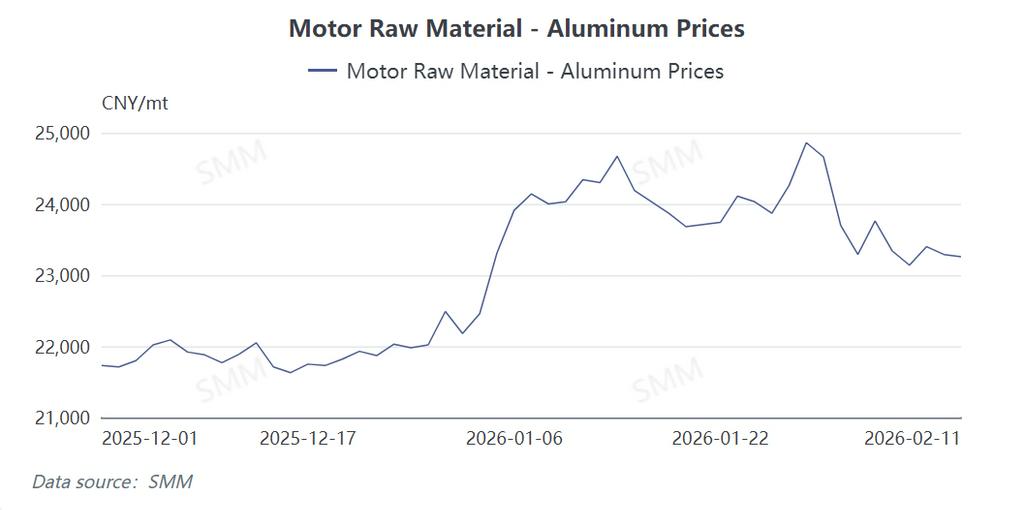

3. Aluminium : Fundamentals tendus face à la demande de transition énergétique

Les prix de l'aluminium ont grimpé de près de 10 % entre décembre 2025 et janvier 2026, principalement en raison d'une tension structurelle entre l'offre et la demande. La demande est soutenue par les tendances mondiales de transition énergétique (par exemple, les carrosseries de véhicules électriques, les plateaux de batteries et les carter de motorisations électriques) et la croissance du solaire photovoltaïque. Du côté de l'offre, la production d'aluminium—très énergivore—est sous pression en raison de la hausse des prix mondiaux de l'électricité, entraînant des taux d'exploitation instables. L'intérêt des investisseurs financiers pour les « métaux verts » a également contribué aux gains de prix.

Bien que la sensibilité au coût de l'aluminium soit inférieure à celle du cuivre, il est largement utilisé dans les carter de moteurs, les couvercles d'extrémité et les systèmes de refroidissement. La hausse des prix augmente directement les coûts de fabrication des moteurs, coûtant des centaines de millions de yuans aux producteurs ayant des volumes annuels de millions d'unités et érodant les marges des fournisseurs de moteurs et des équipementiers.

4. Perspectives : Adaptation technologique et de la chaîne d'approvisionnement

La hausse simultanée des prix des terres rares, du cuivre et de l'aluminium crée une pression sur les coûts sans précédent. Les fabricants de moteurs et de véhicules cherchent urgemment à réduire les coûts, mais les solutions technologiques (par exemple, les moteurs à fil plat, le recyclage des matériaux) nécessitent du temps. Les stratégies à court terme incluent des contrats d'approvisionnement à long terme et la couverture par contrats à terme pour gérer les risques. Le succès à long terme dépendra de l'innovation en matière de matériaux (par exemple, réduire la teneur en terres rares, optimiser la substitution de l'aluminium au cuivre) et de l'intégration verticale de la chaîne d'approvisionnement pour naviguer dans les contraintes de ressources.

SMM conseille aux acteurs du secteur de suivre de près les changements politiques et les technologies alternatives, en adaptant dynamiquement les stratégies d'approvisionnement et de production.

![Les attentes d'optimisme géopolitique s'intensifient, poussant les prix du cuivre à la hausse [Commentaire SMM sur le cuivre BC]](https://imgqn.smm.cn/usercenter/vcsIC20251217171710.jpg)