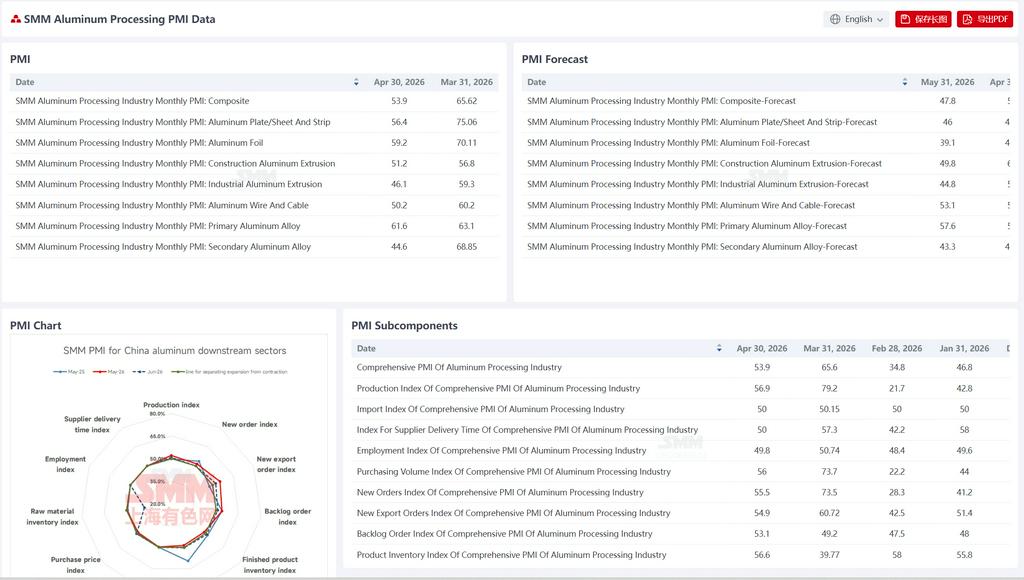

May 29, 2026:

In May, China's aluminum fabrication industry recorded an overall PMI of 50.8%, barely staying above the 50 mark but pulling back significantly by 3.1 percentage points from April. Industry sentiment slid from the edge of expansion territory toward the critical threshold, with structural divergence intensifying further. Persistently high aluminum prices suppressed domestic demand, highlighting a fractured landscape between weak domestic consumption and export support: new energy-related sectors including ESS battery foil, PV frames, and automotive extrusion, along with export orders, served as core stabilizing forces, while traditional civilian standard plate, air-conditioner foil, and secondary aluminum segments fell into deep contraction due to shrinking end-use demand and policy constraints such as "reverse invoicing." Specifically, architectural extrusion, industrial extrusion, aluminum wire and cable, and primary aluminum alloy maintained an expansionary trend, but aluminum plate/sheet and strip, aluminum foil, and secondary aluminum — three major segments — simultaneously pulled back below the 50 mark. The industry shifted from "partial pressure" to "half in contraction," underscoring the insufficient resilience of domestic demand and the growing pains of structural transformation under a high-cost environment. By specific product type:

Aluminum plate/sheet and strip: China's aluminum plate/sheet and strip industry PMI registered 47.9% in May, pulling back below the 50 mark overall. Sub-index wise, both the production index and new orders index stood at 46.1%, simultaneously entering contraction territory. The average aluminum ingot price in May remained at a high level of around 24,300 yuan/mt, deeply suppressing producers' willingness to stockpile raw materials, while end-user clients' fear-of-decline sentiment intensified, with purchases generally made on an as-needed basis. Domestic civilian general-purpose plate saw weak orders due to delayed cargo pick-up and shrinking demand, as the industry entered a phase of competing for existing market share, with top-tier players adopting volume discounts to seize market share. The new export orders index registered 56.8%, in expansion territory and significantly higher than domestic demand, directly corresponding to the strong export performance: April aluminum plate/sheet and strip exports grew 18% both YoY and MoM. Previously suspended Middle Eastern orders were gradually restored through Red Sea rerouting, long-established customers outside China continued to release incremental orders, and enterprises' export orders were already booked through late July. The finished product inventories index was 53.9%. Against the backdrop of high aluminum prices, downstream clients were cautious in picking up goods, and some traders incurred book losses after purchasing, dampening cargo pick-up sentiment and leading to passive accumulation of finished product inventories. Overall, the May aluminum plate/sheet and strip PMI fell below the 50 mark. Energy storage, packaging, and export orders underpinned production on the demand side, but persistently high aluminum prices continued to suppress domestic demand, civilian general-purpose plate orders remained weak, and operational pressure in the industry became prominent. The aluminum plate/sheet and strip PMI is expected to remain under pressure below the 50 mark in June.

Aluminum foil:China's aluminum foil industry PMI registered 48.2% in May. Sub-index wise, the production index and new orders index registered 49.3%, with marginal contraction on both the production and order sides. The energy storage segment became the core growth driver, with downstream large battery cell orders in undersupply and top-tier players' order schedules already booked through 2027, providing strong incremental support for battery foil; food packaging foil maintained its rigid demand attributes. However, the air-conditioner foil segment became the main drag—affected by sluggish property completions, the phase-out of national subsidy policies, overseas capacity relocation, and Middle Eastern geopolitical disruptions, air-conditioner foil orders pulled back notably MoM in May, with weak end-use demand continuing to drag down overall industry output. The new export orders index was 55.8%, maintaining an expansion trend. April aluminum foil exports grew 11% MoM, as the Middle Eastern transportation deadlock was gradually easing, with previously accumulated orders delivered in bulk after Red Sea rerouting was implemented, while the recovery trend in new orders became increasingly clear. Overall, the May aluminum foil PMI fell below the 50 mark. Battery foil and packaging foil demand resilience remained intact, but the deep weakness in air-conditioner foil became the core drag. A further downward shift in the center of the aluminum foil PMI in June will most likely materialize. Architectural Extrusion: The architectural extrusion composite PMI registered 53.5% in May, remaining above the 50 mark for consecutive months. The production index registered 57.0%, the new orders index registered 55.6%, and the purchasing volume index registered 53.5%. The industry continued its recovery trend in May. Some enterprises in Shandong reported that as temperatures rebounded and the construction window opened, end-user demand for home renovation and door/window replacement recovered marginally. Meanwhile, enterprises in North China and Southeast China were actively expanding into large-scale engineering projects, securing orders for schools, libraries, industrial parks, large factory buildings, and landmark structures. These orders were large in volume and long in cycle, providing relatively stable support for production in the short term. The export orders index registered 53.5% this month, with steady release of architectural extrusion demand from Latin America and Oceania, while Central Asian import demand for architectural extrusion also showed a growing trend, indicating a notable recovery in exports. Looking ahead to June, large-scale engineering orders on hand are expected to continue providing stable production support, the aluminum semis price spread in and outside China has room to widen, and the favorable export momentum is expected to sustain. However, the real estate market recovery remains sluggish, with limited visibility on forward development-related orders, which continues to constrain industry sentiment. Overall, the architectural extrusion PMI in June is expected to stay above the 50 mark, but upside room is relatively limited.

Industrial Extrusion: The industrial extrusion composite PMI registered 51.6% in May, rebounding above the 50 mark, with industry sentiment returning to expansion territory. The production index registered 52.8%, the new orders index registered 52.4%, and the purchasing volume index registered 51.6%, with production, demand, and raw material stockpiling all rebounding. On the demand side, the automotive and power sectors maintained steady performance, providing fundamental support for industry operations. In late May, aluminum prices weakened on a phased basis, increasing downstream purchase willingness, driving order growth, and boosting enterprise capacity utilization rates marginally. In the PV segment, some enterprises reported that due to concentrated delivery deadlines in early June, month-end production schedules were ramped up, providing a phased boost to overall industry production. The finished product inventories index registered 50.8% this month. Although enterprises moderately restocked due to increased orders, they overall adhered to the strategy of "produce based on sales with lean inventory" to maintain healthy cash flow. The new export orders index registered 54.3% this month. Manufacturers in Shandong and Henan reported increased export volumes of industrial extrusion products such as container bodies and rail transit components, and the favorable export trend is expected to continue. Looking ahead to June, the industrial extrusion industry remains resilient, and export orders expectations are expected to continue improving. However, aluminum prices are still expected to mainly fluctuate at highs in the near term, and caution is warranted against disruptions to downstream stocking pace triggered by aluminum price fluctuations. The industrial extrusion PMI in June is expected to continue staying above the 50 mark. Aluminum Wire and Cable: In May, China's aluminum wire and cable PMI registered 54.3%, staying above the 50 mark, indicating that the industry maintained an expansion trend and operated at a high level of prosperity. In terms of sub-indices, the production index registered 55.75% in May, the new order index 59.06%, and the new export order index 63.59%. Benefiting from the price spread between domestic and overseas markets, export orders grew significantly, driving domestic manufacturers' operating rates to stay high. Orders also showed strong continuity, extending beyond July, with the backlog order index registering 57.89%. Due to the improvement in new orders, manufacturers' procurement volume increased significantly, with the procurement index registering 56.92%. Meanwhile, shipments stayed at peak levels, and in-factory inventory declined, with the index registering 48.89%. Overall, driven by the significant growth in aluminum stranded wire export orders, the aluminum wire and cable market is expected to maintain a high level of prosperity. However, attention should be paid to the potential drag from a weakening pace of power grid deliveries. The aluminum wire and cable industry PMI is expected to continue operating in expansion territory in June.

Primary Alloy: In May, the primary aluminum alloy industry PMI was 57.4%. Although it pulled back MoM, it remained above the 50 mark, with the industry maintaining an overall prosperous state. In terms of sub-indicators, the production index was 70.3%, the inventory index 25.3%, and the purchase price index 49.3%, which pulled back MoM, reflecting eased overall downward pressure on prices and a slight recovery in trading activity. Demand side, aluminum wheel hub exports performed well in April, up 19.43% MoM and up 12.71% YoY. Export orders continued to recover, providing certain support for aluminum wheel hub demand. Overall export demand in May is also not expected to weaken significantly and is expected to maintain a stable volume. However, Chinese market demand has yet to show notable growth. Combined with aluminum prices fluctuating at highs, enterprises' willingness to increase production was suppressed, limiting further improvement in primary aluminum alloy operating rates. Notably, aluminum prices have pulled back recently, and some downstream enterprises have begun to place quotes, with trading volume recovering slightly. However, overall spot order transactions remained thin, and wait-and-see sentiment was strong in the market. Despite limited downside room for prices, actual transaction growth remained insignificant. Overall, the primary aluminum alloy industry is expected to continue its current operating trend next week, with operating rates remaining stable and no significant fluctuations. Looking ahead to June, supported by exports and stable domestic demand, the primary aluminum alloy PMI is expected to remain above the 50 mark. Secondary alloy: The secondary aluminum industry PMI registered 44.6% in May, down 6.3 percentage points MoM, remaining below the 50 mark, with industry prosperity continuing in contraction. Production side, secondary aluminum production generally declined in May, mainly due to the overlap of two factors: first, the Labour Day holiday combined with weakening end-use demand led to order contraction that dragged down operations; second, continued tightening of regulatory oversight on the "reverse invoicing" policy drove up compliance costs in the aluminum scrap recycling process, tightening the supply of available invoiced materials, leaving enterprises facing the dual pressure of "invoice shortages" and production losses, further lowering operating rates. However, a few enterprises maintained stable or slightly rebounding operating rates, mainly because gaps existed in the ex-China aluminum alloy market and domestic prices held a competitive advantage, leading to increased export orders. Meanwhile, orders from some small and medium-sized enterprises concentrated toward top-tier players, with large enterprises seeing moderate order performance. Overall, however, enterprises remained cautious in taking orders, prioritizing delivery to aluminum liquid and long-term contract clients, with insufficient willingness to take spot orders with limited profit margins, constraining further recovery in operating rates. Inventory side, imported aluminum scrap and domestically compliant raw material circulation remained tight, enterprise raw material inventories continued to be depleted, new restocking volumes were limited, and combined with supply-side narrowing, both raw material and finished product inventories declined. Looking ahead to June, if the raw material shortage issue is not substantially alleviated, enterprise procurement difficulties will persist, and combined with demand moving further into the off-season, operating rates are expected to continue declining, with the PMI remaining under pressure below the 50 mark.

Brief commentary:

In May, the aluminum processing industry PMI pulled back under pressure to the edge of the 50 mark, with high aluminum prices and weak domestic demand forming the core contradiction, while export resilience and new energy demand served as key supports. Industry divergence intensified, with traditional sectors (civilian general-purpose plate, air-conditioner foil, secondary aluminum) deep in contraction territory, while building profiles, aluminum wire and cable and other segments maintained expansion relying on engineering orders and exports. In the short term, aluminum prices fluctuating at highs and lackluster property recovery will continue to constrain domestic demand recovery, and enterprises are likely to maintain cautious strategies. The June PMI is expected to move sideways near the critical threshold with marginal pressure, making the urgency for industry transformation and structural optimization increasingly pressing.

![Aluminum Liquid Aluminum Proportion Increased More Than Expectations in May, Expected to Edge Up in June [SMM Analysis]](https://imgqn.smm.cn/usercenter/JnyfJ20251217171654.jpg)

![Aluminum Billet Processing Fees Broke Through in May, Supply-Side Disruptions Not to Be Ignored [SMM Analysis]](https://imgqn.smm.cn/production/admin/votes/imagesSDWVM20240508153016.png)