Según la Agencia de Noticias Xinhua, a medida que se intensificaba el conflicto entre Estados Unidos e Irán, el Cuerpo de la Guardia Revolucionaria Islámica de Irán anunció el cierre del Estrecho de Ormuz en la tarde del 28 de febrero. Varios propietarios de buques cisterna y comerciantes han suspendido el transporte a través del estrecho. Esta es la primera vez en los últimos años que el canal central de transporte de energía y productos químicos a nivel mundial se enfrentaba a una suspensión sustantiva. Como la "garganta" del comercio mundial de azufre, esta interrupción cortará directamente los canales de exportación de azufre de Oriente Medio y creará una reacción en cadena que afectará a la producción de MHP de Indonesia y a la industria de fertilizantes fosfatados de China, las cuales dependen en gran medida de las fuentes de Oriente Medio.

I. Estrecho de Ormuz: el "canal vital" para las exportaciones de azufre de Oriente Medio se corta y la capacidad de las rutas alternativas es limitada

El Estrecho de Ormuz es el paso central absoluto para el comercio mundial de azufre, y su cierre tendrá un impacto de "magnitud" en las exportaciones de azufre de Oriente Medio.

1. El comercio mundial de azufre depende en gran medida de este paso

En el comercio marítimo mundial de azufre, el 50 % de la carga (aproximadamente 20 millones de toneladas al año) proviene de la región del Golfo Pérsico en Oriente Medio y debe pasar por el Estrecho de Ormuz para llegar a los mercados mundiales. Los principales países exportadores incluyen Arabia Saudita, Emiratos Árabes Unidos, Catar, Kuwait e Irán.

2. Todos los principales puertos de exportación están bloqueados

Los principales puertos de exportación de azufre de Oriente Medio —Ruwais en Emiratos Árabes Unidos, Jubail y Ras al-Khair en Arabia Saudita, Ras Laffan en Catar, Al Zour y Shuaiba en Kuwait y Bandar Imam Jomeini en Irán— todos necesitan transportar su azufre a través del Golfo Pérsico y luego, a través del Estrecho de Ormuz, al Océano Índico. El cierre del estrecho significa que el azufre de estos puertos no puede cargarse ni exportarse.

3. Capacidad extremadamente limitada de las rutas alternativas

Aunque existen opciones para evitar el Estrecho de Ormuz, son difíciles de operar a gran escala:

Puerto de Fujairah, Emiratos Árabes Unidos: se encuentra fuera del estrecho en el Golfo de Omán, pero lejos de las principales áreas de producción del Golfo Pérsico, con altos costos de transporte terrestre y capacidad limitada, y es difícil dar prioridad al azufre a granel durante las crisis.

Puertos Rojos del Mar de Arabia Saudita: El azufre puede transportarse por tierra hasta el puerto de Yanbu, pero el transporte terrestre a larga distancia enfrenta desafíos económicos y operativos significativos.

II. Indonesia MHP: El azufre del Medio Oriente como fuente central de materiales auxiliares, la interrupción logística aumentará directamente los costos de producción

Como sitio de producción clave para los materiales de níquel-cobalto de nueva energía (MHP) a nivel global, los proyectos HPAL de Indonesia dependen en gran medida del azufre del Medio Oriente. Esta interrupción afectará directamente los costos de producción y la estabilidad del suministro de MHP.

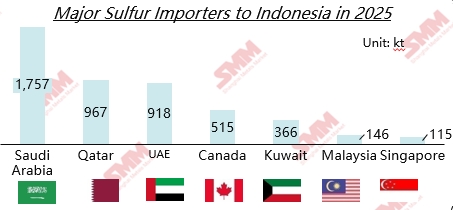

1. Alta concentración de importaciones de azufre en Indonesia

Según datos aduaneros indonesios, más del 75% de las importaciones de azufre de Indonesia en 2025 provienen del Medio Oriente. Esta estructura de suministro altamente concentrada significa que, tras el cierre del Estrecho de Ormuz, la fuente principal de materias primas para los proyectos MHP de Indonesia quedaría cortada.

2. Demanda rígida para la producción de MHP

Basándose en promedios de la industria, producir 1 tonelada de MHP requiere aproximadamente 11,7 toneladas de azufre. Aunque recientes deslizamientos de tierra en un parque industrial indonesio han interrumpido algunos proyectos, llevando a operaciones con baja carga y demanda incierta a nivel de abajo, otros proyectos MHP existentes y nuevos aún tienen una demanda rígida significativa de azufre.

3. Mecanismo de transmisión de costos fortalecido

Impacto directo en los costos: SMM estima que, para enero de 2026, el azufre representaba el 41% de los costos de producción de MHP. Si los precios del azufre continúan subiendo debido a las interrupciones del suministro, el costo del azufre en MHP también aumentará, reduciendo los márgenes de ganancia de los proyectos.

Costos de adquisición en aumento: Los compradores indonesios se verán forzados a competir con compradores globales por suministros limitados no provenientes del Medio Oriente. Además, los incrementos en las primas de seguros y los costos de envío debido a desvíos, elevarán aún más los costos de llegada.

III. Impacto ampliado en los precios: La acelerada disminución de las existencias de azufre en China impulsará aún más los precios

Como el mayor importador de azufre del mundo, China tiene una dependencia estructural de las fuentes del Medio Oriente. Esta interrupción afectará directamente el suministro doméstico de azufre y la producción de fertilizantes fosfatados, impulsando aún más los precios del azufre.

1. Dependencia extremadamente alta de las importaciones

La dependencia externa de China en azufre se ha mantenido durante mucho tiempo entre el 50% y el 53%. Los datos aduaneros muestran que en 2025, Oriente Medio representó el 56,2% de las importaciones de azufre de China, lo que significa que más de la mitad de la logística de azufre importado se verá afectada.

2. Demanda rígida para la preparación de fertilizantes en primavera

Actualmente, es un período crucial para la preparación de fertilizantes en primavera, donde existe una demanda rígida de azufre para la producción de fertilizantes fosfatados. Las empresas de diammonium fosfato a nivel de abajo mantienen altas tasas de operación, con demandas de reposición liberadas, y las subastas generalmente se cierran a precios premium, lo que indica una fuerte intención de los comerciantes de mantener firmes los precios.

3. Agotamiento acelerado del inventario, suministro alternativo limitado

Los datos financieros de iFinD muestran que, al 28 de febrero, el inventario total de azufre en los puertos de China fue de 1,7398 millones de toneladas. Con un consumo mensual promedio de 1,4 a 1,5 millones de toneladas durante la temporada de arado de primavera, el inventario actual solo puede soportar 1,2 a 1,5 meses. Considerando los inventarios de fábrica y las mercancías en tránsito, el tiempo de soporte se extiende a 1,5-2 meses. Si el bloqueo del estrecho continúa, el inventario se agotará rápidamente durante el pico de la temporada de arado de marzo-abril. Aunque China puede buscar fuentes alternativas en Norteamérica, el Mar Negro y Asia Central, las mayores distancias de transporte, los costos de flete más altos y las restricciones contractuales limitarán la velocidad de reabastecimiento.

Ⅳ. Advertencias de riesgos a nivel de abajo

1. Materiales para baterías de vehículos eléctricos:Como material crudo central para precursores de cátodos ternarios, el aumento en los costos de MHP se transmitirá a lo largo de la cadena de la industria a materiales de cátodo y células de batería, afectando finalmente los costos de fabricación de vehículos eléctricos.

2. Fertilizante fosfatado: El 56% de las importaciones de azufre de China enfrenta un riesgo de interrupción del suministro. Los inventarios portuarios nacionales se agotarán rápidamente durante el pico de la preparación agrícola de primavera, con los precios del azufre esperados a superar máximos anteriores y transmitirse a los precios de fertilizantes fosfatados a nivel de abajo, elevando finalmente los costos de producción agrícola.

3. La duración es la variable central:

Si la suspensión es a corto plazo (1-2 meses): El impacto se centrará principalmente en las fluctuaciones de precios, que las empresas pueden manejar mediante ajustes de inventario y sustitución de materias primas.

Si la suspensión es a largo plazo (más de 3 meses): provocará una brecha de suministro en constante expansión. Algunas empresas que dependen de acuerdos a largo plazo con el Medio Oriente pueden experimentar escasez de materias primas, reducción de la carga de las instalaciones o incluso cierres. Las cadenas globales de azufre y sus industrias downstream experimentarán una reestructuración profunda.

![[SMM Analysis] Análisis del mercado del sulfato de níquel de junio: Precio bajo presión por el aumento de costos y el desajuste entre oferta y demanda](https://imgqn.smm.cn/usercenter/KFwsY20251217171734.jpg)