SMM July 17 News:

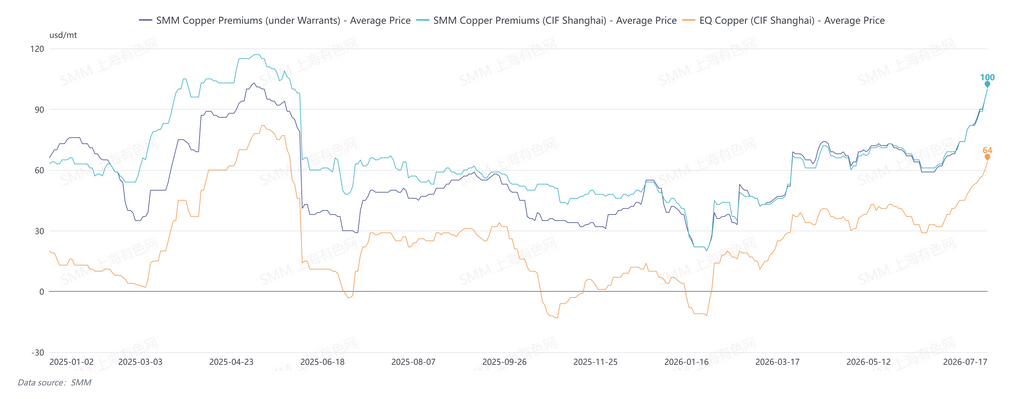

Since late June, copper premiums cif China have been climbing. Spot premiums for registered copper arriving at China's ports from late July to August have recently breached triple digits, continuously setting new yearly highs.

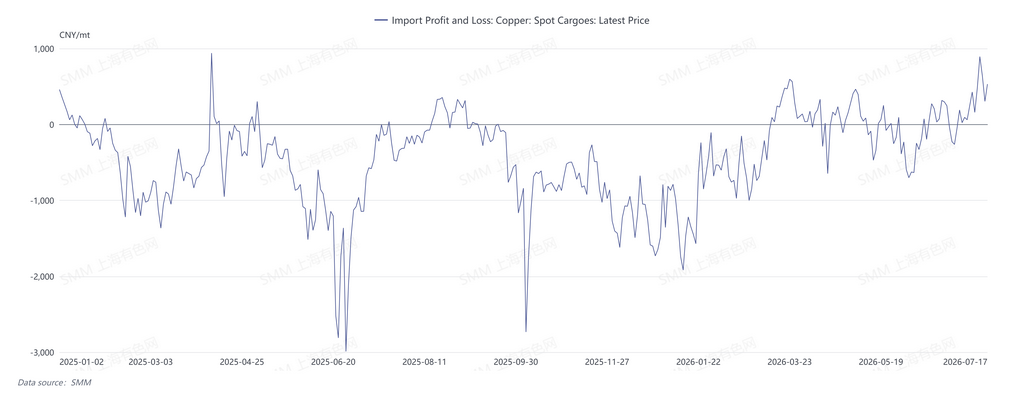

On July 17, the SMM copper premiums CIF China quotation range was $95–$105/mt, QP August, with an average of $95/mt; the premiums in-whs Shanghai quotation range was $95–$105/mt, QP August, average $95/mt; and the EQ copper premiums CIF China quotation range was $60–$68/mt, QP August, average $64/mt. As of July 17, the ex-FX SHFE/LME copper price ratio for LME copper against the SHFE August 2026 contract stood at 1.1384, implying import losses around 139.75 yuan/mt. The LME copper nearby structure was in contango, with the spread between the August and September dates at −$8.23/mt.

The current surge in copper premiums is primarily driven by tight market supply:

1. As the US copper tariff policy remains unresolved, frequent arbitrage opportunities between LME and COMEX markets continue to channel global copper cathode shipments to North America.

2. Ongoing geopolitical conflicts and high costs for sulphuric acid and energy have hurt SX-EW copper production in Africa. Meanwhile, Zambia has entered an intensive maintenance period, and logistical uncertainties have reduced arrivals in China in July–August.

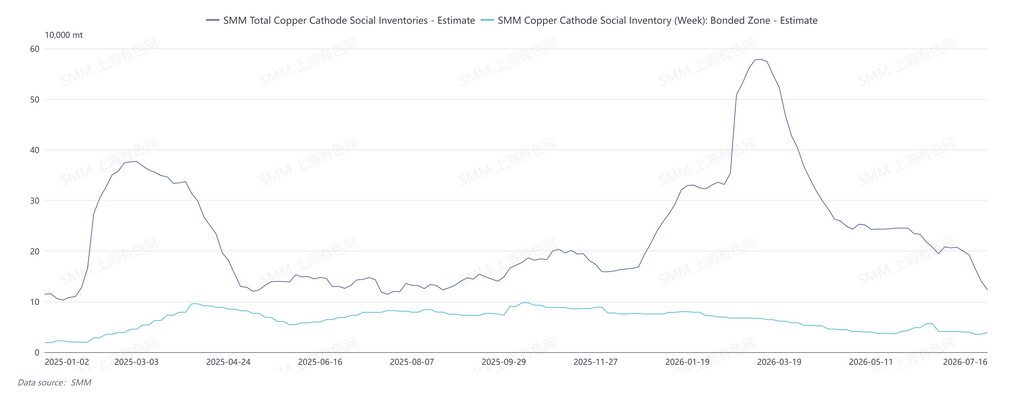

3. China's social inventory has been rapidly depleting, while smelter arrivals have been relatively low. Tight supply of copper concentrates and falling spot TC, coupled with limited secondary material availability, have created significant raw material pressure for smelters. At the same time, the impact of the intensive May–June maintenance season has not yet fully faded. Production resumptions and output recovery at some smelters have been slow, and some have introduced unplanned maintenance. As a result, domestic copper cathode output and shipments to major consumption areas remain below previous levels.

Price ratio side, the spot import window is open, but the August and September date windows remain shut, intensifying suppliers' tendency to hold back from selling. Only a few seller offers are available in the market, giving upstream players strong confidence to hold prices firm. However, downstream demand has been mediocre, so recent actual deal volumes are limited. Overall, sellers' firm pricing and downstream fear of high prices have intertwined, leaving the market in a pattern of both weak supply and demand.

According to SMM, as of Thursday, July 16, China bonded zone copper inventories rose about 3,300 mt WoW from July 13 to 38,900 mt. Shanghai bonded inventories rose 2,900 mt WoW to 34,800 mt, and Guangdong bonded inventories rose 400 mt WoW to 4,100 mt. The bonded zone inventory shifted from destocking to inventory buildup, mainly due to reduced warehouse withdrawa

Looking ahead, with the North American siphon effect and African production hit by rising costs, the market is expected to continue trading on tightness of available material in the near term. However, it is worth noting that LME cancelled warrants have increased notably recently. As of July 15, total LME inventory stood at 300,600 mt, down 1,675 mt from the previous period, while cancelled warrants rose to 169,075 mt, with the ratio of cancelled warrants at 56.25%. According to SMM, amid current high premiums, some material is already being shipped to China. Attention should be paid to the volume of this supply replenishment and the downstream's ability to absorb high premiums given actual consumption demand.

![Spot Transactions of Imported Copper Concentrates Increase, TCs Continue to Deteriorate [SMM Copper Concentrate Spot Weekly Review]](https://imgqn.smm.cn/usercenter/ULCXN20251217171714.jpeg)

![Price Difference Between Copper Cathode and Copper Scrap Widens by Over 2,000 Yuan, Spurring Arbitrage Purchases to Dominate Transactions [SMM Analysis]](https://imgqn.smm.cn/usercenter/HAuaN20251217171710.jpg)