The global overseas primary aluminum spot market faced overall downward pressure this week, with spot premiums in Japan, Southeast Asia, South Korea and the US all falling week-on-week. The Asian market was weighed down by weak downstream purchasing sentiment amid the traditional consumption off-season. Ample circulating supply stemming from concentrated cargo arrivals in the US compounded the bearish sentiment. Meanwhile, the LME curve briefly flipped into a Backwardation (B) structure this week. Elevated capital costs prompted traders to step up sell-downs, pushing spot offers lower across regions and dragging down transaction benchmarks.

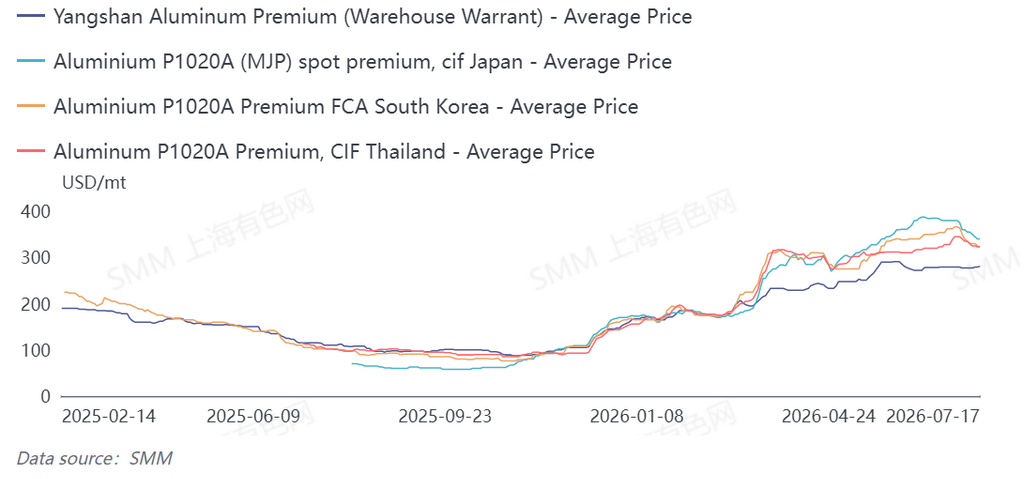

I. Weekly Comparison of Key Global Spot Premiums

II. Regional Spot Transaction & Market Commentary

(I) Asian Market: Sluggish Off-Season Buying, Wide Disparity Between Long-Term Benchmark QMJP and Spot Prices

Japan Market

Japan’s spot market remained sluggish this week, with downstream buyers only placing sporadic orders to meet immediate operational needs and no large-scale restocking activities. The Q3 QMJP benchmark price was set at USD 395/mt, sharply diverging from actual spot transaction prices ranging from USD 330–350/mt, resulting in steep discounts against the quarterly benchmark across the market.

Southeast Asia, South Korea and Indonesia

Spot premiums in Thailand and South Korea retreated in tandem as traders showed strong willingness to offload inventories. Overseas end-user demand for Indonesian primary aluminum stayed muted, while downstream players remained reluctant to accept high prices, driving down local ex-factory offers and concluded transaction prices.

Across Asian trading channels, the temporary Backwardation structure on the LME aluminum curve, paired with higher capital costs and inventory pressure, encouraged holders to cut offers to liquidate stocks. Coupled with feeble downstream demand, spot prices faced additional downward pressure.

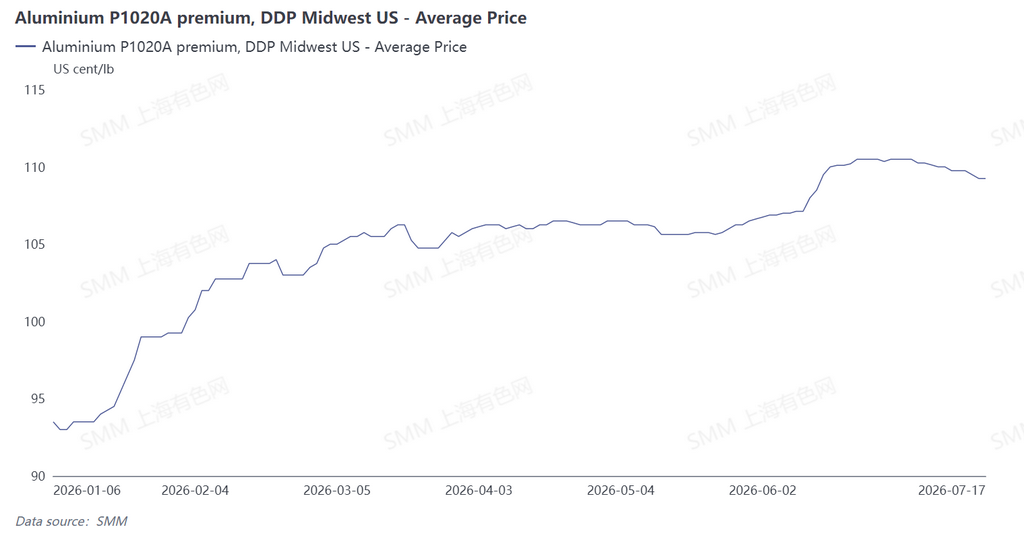

(II) US Market: Concentrated Cargo Arrivals from Multiple Regions Weigh on Premiums

Easier spot prices in Europe previously diverted some Canadian aluminum ingots to the US, alongside a portion of Indonesian primary aluminum shipments. Concentrated cargo arrivals boosted market supply substantially. Despite rigid underlying demand in the US, the surge in available supply kept DDP premiums under mild week-on-week downward pressure.

III. Core Macro Drivers Shaping Overseas Spot Markets

End-User Demand: Off-Season Drags on Asian Buying Sentiment

Southeast Asia and Japan entered their traditional demand off-season. Downstream fabricators only purchased materials on an as-needed basis without proactive stockpiling, and market acceptable price levels kept sliding, leaving spot transactions without solid support.

Trading Flows: High Capital Costs Fuel Traders’ Inventory Liquidation

The temporary Backwardation structure on the LME aluminum curve lifted holding costs for metal traders. Most market participants opted to cut prices to sell stocks and recover capital, flooding the market with available material and further depressing spot premiums.

IV. Brief Market Outlook

In the near term, the off-season in Asia is far from over, and traders retain strong incentives to liquidate inventories, which will keep overseas primary aluminum spot premiums subdued. Market participants will closely monitor the commissioning timeline of Indonesian aluminum projects and restocking activities among overseas downstream manufacturers going forward.

![Cost Support and Demand Constraints Coexist, ADC12 Consolidates at Highs [SMM Analysis]](https://imgqn.smm.cn/usercenter/tkWbz20251217171654.jpg)

![Cost Support and Demand Constraints Coexist, ADC12 Consolidates at Highs, Awaiting Peak Season Breakthrough [SMM Analysis]](https://imgqn.smm.cn/usercenter/jWDCu20251217171653.jpg)