SMM News, June 26:

1. H1 Import and Export Overview: Lead Ingot Imports Surge Sharply, Exports Remain Sluggish

According to China’s General Administration of Customs, combined imports of refined lead and lead products in January-May 2026 stood at 248,443 mt, surging 291.06% YoY cumulatively. The import window remained wide open in H1, with overseas cargoes flooding in continuously, pushing total import volume beyond the full-year 2025 level. On the export side, combined exports of refined lead and lead products totaled only 20,197 mt in January-May, down 32.49% YoY, hovering at low levels overall.

Monthly import data showed a sustained uptrend: cumulative imports of refined lead reached 33,412 mt in January-February, with single-month YoY growth in February exceeding 11x; March imports of refined lead and lead alloys totaled 49,399 mt; April combined imports stood at 57,343 mt, up 15.69% MoM and surging 680.12% YoY; May refined lead imports reached 36,684 mt, only 0.66% MoM lower, and adding 23,414 mt of lead alloy imports brought the monthly total to nearly 60,100 mt, up 731.65% YoY. The high import level in May was supported by three main factors: the elevated SHFE/LME lead price ratio providing steady import arbitrage opportunities, the concentrated arrival of cargoes from India and South Korea, and supply tightness from domestic smelting maintenance and secondary lead production cuts; at the same time, LME inventories surged to 314,000 mt, with sufficient availability of overseas low-grade lead ingots, though spot premiums for high-grade lead ingots in Southeast Asia remained elevated.

The export market performed poorly, with March refined lead exports at 3,190 mt, tumbling 70.96% MoM to 926.52 mt in April. May exports rebounded 128.99% MoM to 2,121.59 mt but were still 61.80% lower YoY. Export cargoes mainly headed to Vietnam, Malaysia, and Taiwan, China. The persistently inverted SHFE/LME price ratio weighed on export willingness over the long term.

2. Price, Inventory, and Trade Window Dynamics Review

The domestic market outperformed the overseas market throughout H1, which was the core driver behind the continuously open import window. From January to March, both the SHFE and LME dropped in tandem; in April, LME lead strengthened while SHFE lead was in the doldrums, keeping overall import arbitrage space ample. The trend shifted in May, as the SHFE/LME price ratio declined, import profits narrowed substantially, and the logic behind the price spread between Chinese and overseas markets gradually reversed.

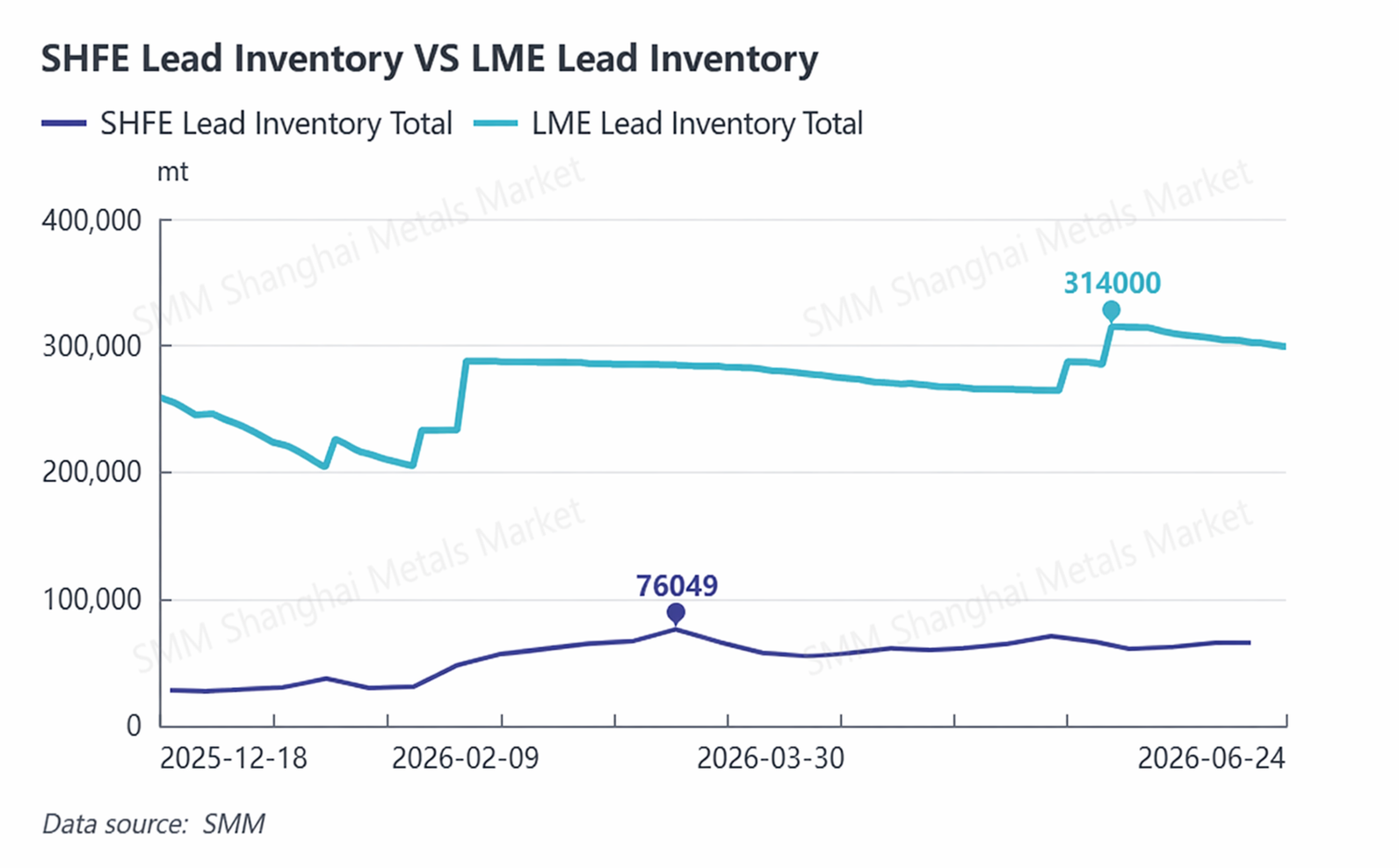

The inventory trend diverged sharply between the domestic and overseas markets: overseas LME inventories surged to 314,000 mt by end-May, hitting a 13-year high, before pulling back slightly to 300,700 mt in June, highlighting a global oversupply of low-end lead ingots. Domestically, SMM social inventory across five major regions exceeded 70,000 mt in mid-May and slowly destocked to 67,700 mt in June. SHFE warrants rose in tandem, and persistent spot supply pressure remained in China.

3. Short-term Import and Export Forecast for June

Imports: Combined imports of refined lead and lead products in June are expected to fall to 35,000-45,000 mt. On the one hand, lower LME lead prices and LME spot discounts compressed import profits, and partial production resumptions at domestic secondary lead smelters filled supply gaps, weakening import momentum. On the other hand, previously placed overseas orders in May will see delayed arrivals, so imports will unlikely fall off a cliff. Exports: Monthly exports are expected to stay at low levels of 2,500-3,500 mt. The extended off-season for domestic batteries, scarce EXW cargoes from smelters, and tariff barries in the Middle East will constrain any substantial opening of the export window.

4. Key Variables to Watch in H2

1. Fluctuations in the SHFE/LME price ratio: Directly determining the opening and closing of the import-export arbitrage window and trade flow direction;

2. Progress of domestic secondary lead production resumptions: Deciding the scale of China’s supply gap and indirectly affecting import demand;

3. Intensity of Q3 end-use consumption: If restocking exceeds expectations during the peak season, it could provide temporary boosts to imports;

4. Overseas supply chain disruptions: Middle East geopolitical tensions and changes in shipping costs could affect spot premiums for overseas lead ingots;

5. US Fed monetary policy: USD fluctuations could indirectly shift the center of the SHFE/LME price ratio.

Q3 (July-September): As the battery sector enters its traditional peak season, downstream restocking should offer temporary support for imports. However, considering the concentrated resumption of domestic secondary lead production, which will enhance China’s self-sufficiency in raw materials and marginally reduce its reliance on imports, the average monthly import volume is expected at 30,000-40,000 mt. Q4 (October-December): If the SHFE/LME price ratio continues to decline and the import window closes sporadically, monthly refined lead imports will further contract to 20,000-30,000 mt. In total, the estimated combined imports of refined lead and lead products for full-year 2026 will likely range between 320,000-360,000 mt.

![SMM July 29 Automotive Battery Market Roundup [SMM Evening Update]](https://imgqn.smm.cn/usercenter/TmYox20251217171721.jpeg)

![Bears reduced positions more, lifting the center of SHFE lead [Lead Futures Brief Comment]](https://imgqn.smm.cn/usercenter/bAjSC20251217171721.jpg)