In 2025, international sulfur prices experienced significant fluctuations, rising from below $200 per mt to over $540 per mt. The market currently focuses on the marginal demand increment from Indonesia's nickel intermediate product hydrometallurgy projects. Meanwhile, the growth of the electrochemical energy storage industry, centered on lithium iron phosphate (LFP) batteries, serves as another strong marginal demand variable. Through a rigid transmission chain, it is disturbing and will further influence the global sulfur supply-demand pattern.

I. Rigid Transmission: From Hundreds of GWh in ESS Production to Millions of Metric Tons in Sulfur Demand

Energy storage has become a core component of the global energy transition, with market demand showing highly certain growth. As the absolute mainstream technology for ESS batteries, LFP batteries and their core cathode material—LFP—are experiencing rapid simultaneous capacity expansion. By year-end 2025, China's LFP capacity had exceeded 6.5 million mt, with multiple new capacity projects planned for the future.

Industrial Pathway: ESS Installations → LFP Battery Demand → LFP Cathode Material Production

SMM calculations indicate that each GWh of LFP ESS batteries consumes 2,200 mt of LFP; producing 1 mt of LFP requires approximately 0.9 mt of sulfur.

Accordingly, the hundreds of GWh scale of the energy storage industry directly translates into millions of metric tons of sulfur demand. According to statistics, global LFP ESS battery cell production reached 545 GWh in 2025, corresponding to an annual sulfur demand of approximately 1.2 million mt, with China accounting for over 98% of this production. Against the backdrop of sulfur supply mainly relying on by-products from oil and gas—characterized by rigid growth (annual growth rate only 1–3%)—this marginal increment has become a core driver disrupting the market's tight balance and creating a persistent supply-demand gap.

II. Restructuring Demand Side: Altering Sulfur Market’s Seasonal Linkage, Becoming a Stable Demand Source

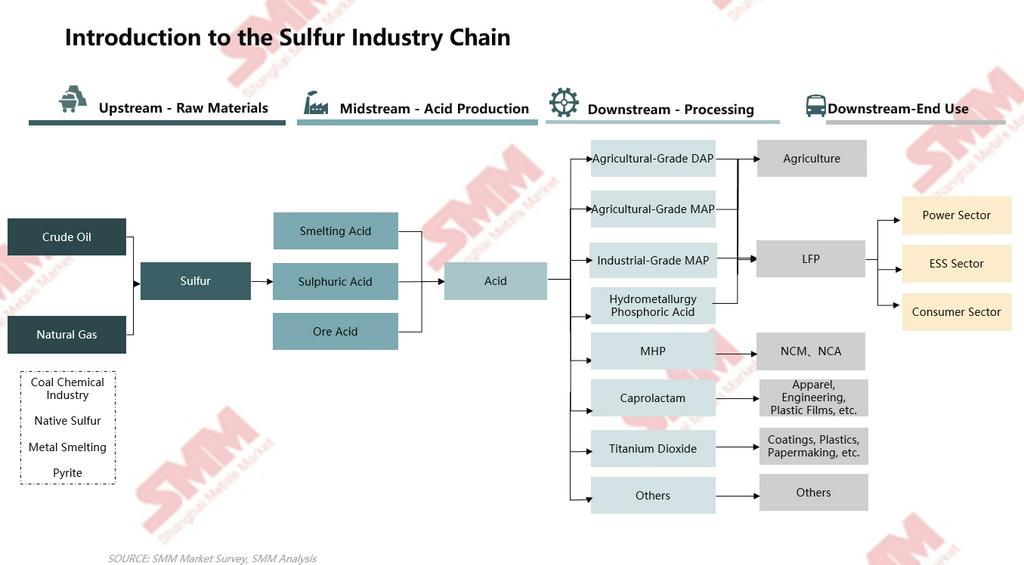

Traditionally, global sulfur demand has been primarily driven by the agricultural chemical sector, such as phosphate fertilizers, with its demand curve highly tied to agricultural production seasonal cycles, exhibiting stable "stock" characteristics. However, the rise of the LFP energy storage industry and Indonesia's nickel intermediate products has introduced a steep, agriculture-cycle-independent demand curve to the sulfur market. III. Long-Term Forecast: Resource Competition and ESS Driving Sulfur Demand in Millions of Metric Tons

SMM forecasts that global LFP ESS battery cell production will reach 827 GWh in 2026, resulting in LFP consumption of 1.82 million mt and ultimately sulfur consumption of approximately 1.64 million mt in the ESS sector. In 2027, global LFP ESS battery cell production is projected to reach 1,065 GWh, leading to LFP consumption of 2.34 million mt and sulfur consumption of approximately 2.11 million mt. Against the backdrop of global sulfur market undersupply and structural supply-demand mismatch, ESS has emerged as the second marginal demand driver.

Looking further ahead, SMM expects global LFP capacity to reach 13 million mt by 2030. The rapid adoption of LFP batteries in ESS and NEV applications has become a core driver of the global energy transition. The rapid expansion of LFP capacity will further influence the global sulfur market's supply-demand pattern.

From a global sulfur market perspective, with rigid supply constraints remaining largely unchanged and continuous demand growth, marginal demand increments represented by LFP-based ESS have become a key variable impacting the supply-demand balance, currently characterized by "small proportion, large impact." Sulfur prices are no longer solely influenced by seasonal agricultural demand and may maintain an upward trend. In the short term, sulfur prices are expected to have further upside room in 2026. Over the medium and long term, attention in emerging demand sectors should focus on Indonesia's RKAB quota policy and new MHP project capacity releases for nickel intermediates, while the ESS sector should monitor the growth rate of installed shipments and the commissioning of new LFP project capacity.