En enero de 2026, la industria de las baterías de iones de sodio entró en un ciclo operativo especial previo al Año Nuevo Chino, mostrando la cadena de suministro una doble característica: "soporte de la demanda por acumulación de inventarios previa a las festividades" y "llegada de la temporada baja tradicional de producción". Sumado al aumento en los precios del carbonato de litio a principios de año, que incrementó los costos de las celdas de baterías de litio, la atención del mercado y la lógica de sustitución por productos de baterías de iones de sodio se fortalecieron aún más. En cuanto al desempeño productivo, todos los segmentos de la cadena de suministro de baterías de iones de sodio lograron un crecimiento interanual significativo, confirmando que la industria mantiene una rápida trayectoria ascendente hacia la comercialización. Sin embargo, el desempeño mensual mostró una divergencia significativa debido al ritmo de acumulación de inventarios, las características de los productos y los impactos de la temporada baja. Shanghai Metals Market (SMM) revisó exhaustivamente las operaciones de toda la cadena de suministro de baterías de iones de sodio en enero, incluyendo materiales de cátodo, ánodos de carbono duro, electrolitos y celdas de baterías para usuarios finales, analizando las características actuales de la industria y proporcionando una perspectiva del mercado a corto plazo.

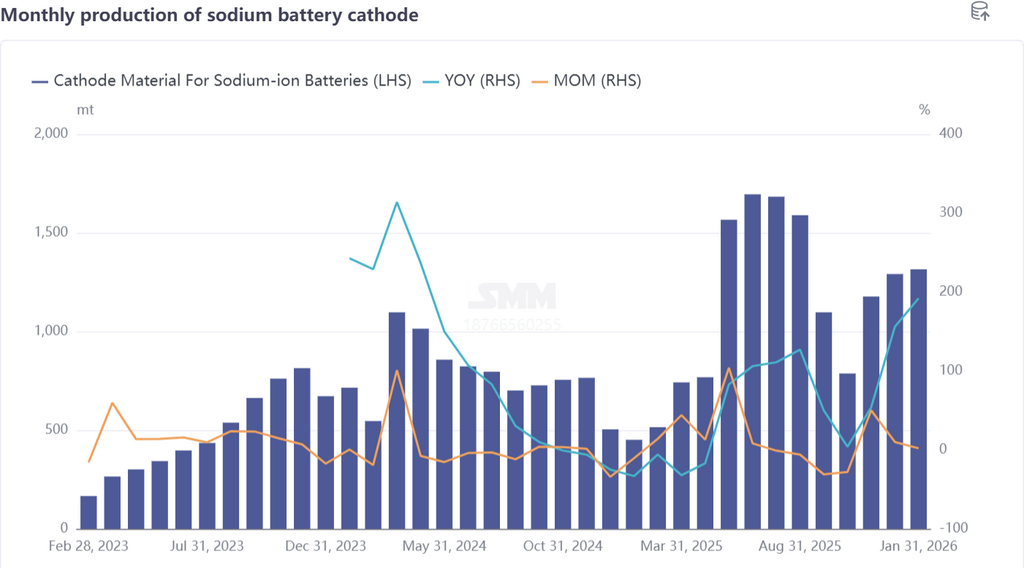

Materiales de Cátodo: La Producción de NFPP se Mantiene Estable en Medio de la Acumulación de Inventarios, los Materiales de Óxido en Capas Siguen Rindiendo por Debajo de lo Esperado

La producción de materiales de cátodo para baterías de iones de sodio aumentó ligeramente un 2% mensual y se disparó un 192% interanual en enero, con una estructura de productos que se concentró aún más en materiales de polianión, representando el 91% del total. Entre ellos, la participación del NFPP aumentó 10 puntos porcentuales mensuales, convirtiéndolo en el absoluto protagonista del mercado. En enero, la producción de NFPP se centró en la entrega de pedidos existentes, mientras que la mayoría de las empresas comenzaron operaciones de acumulación de inventarios previas a las festividades para asegurar el suministro durante el período de transición posterior a las vacaciones, cuando se esperan pedidos temporales. El programa de producción de la industria mantuvo una tendencia favorable. En marcado contraste, la producción de materiales de óxido en capas se mantuvo débil, representando solo el 6% en enero, con niveles de pedidos aún en un punto bajo y sin señales de una recuperación significativa a corto plazo. Mirando hacia adelante, debido a las vacaciones tradicionales del Año Nuevo Chino en febrero, las empresas de materiales de cátodo para baterías de iones de sodio experimentarán aproximadamente medio mes de festividades, con la producción deteniéndose en gran medida. SMM espera que la producción de cátodos para baterías de iones de sodio disminuya significativamente un 70% mensual y un 23% interanual en febrero.

La producción de materiales de cátodo para baterías de iones de sodio aumentó ligeramente un 2% mensual y se disparó un 192% interanual en enero, con una estructura de productos que se concentró aún más en materiales de polianión, representando el 91% del total. Entre ellos, la participación del NFPP aumentó 10 puntos porcentuales mensuales, convirtiéndolo en el absoluto protagonista del mercado. En enero, la producción de NFPP se centró en la entrega de pedidos existentes, mientras que la mayoría de las empresas comenzaron operaciones de acumulación de inventarios previas a las festividades para asegurar el suministro durante el período de transición posterior a las vacaciones, cuando se esperan pedidos temporales. El programa de producción de la industria mantuvo una tendencia favorable. En marcado contraste, la producción de materiales de óxido en capas se mantuvo débil, representando solo el 6% en enero, con niveles de pedidos aún en un punto bajo y sin señales de una recuperación significativa a corto plazo. Mirando hacia adelante, debido a las vacaciones tradicionales del Año Nuevo Chino en febrero, las empresas de materiales de cátodo para baterías de iones de sodio experimentarán aproximadamente medio mes de festividades, con la producción deteniéndose en gran medida. SMM espera que la producción de cátodos para baterías de iones de sodio disminuya significativamente un 70% mensual y un 23% interanual en febrero.

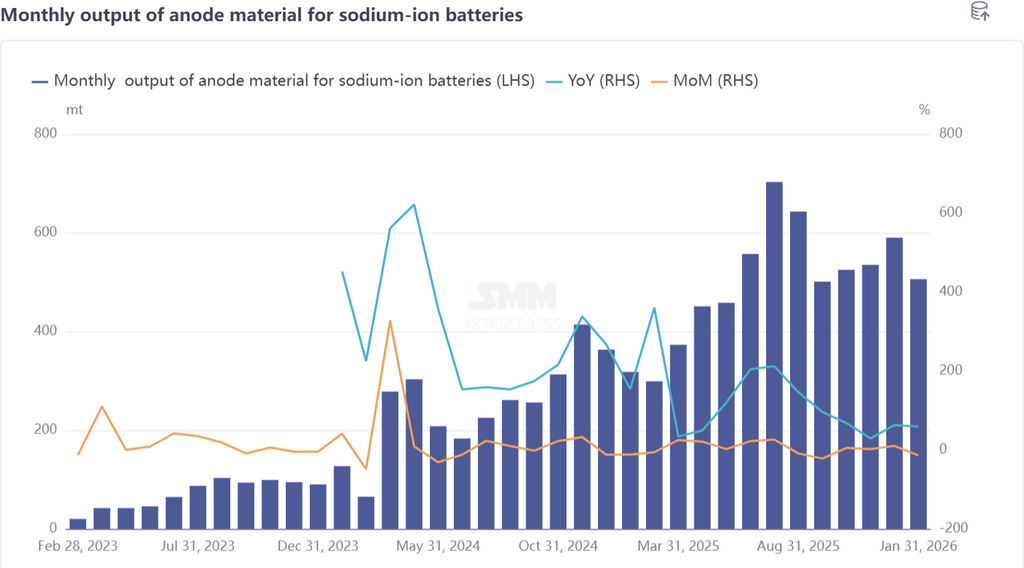

Material de ánodo de carbono duro: Los pedidos se producen según la demanda, la nueva capacidad y la demanda exterior abren espacio de crecimiento

En enero, la producción de materiales de ánodo para baterías de iones de sodio disminuyó un 14% mensual pero se disparó un 59% interanual, manteniendo el mercado general un ritmo de producción basado en la demanda. Actualmente, el mercado de carbono duro muestra un cumplimiento estable de pedidos, con ESS y fuentes de alimentación de arranque-parada como áreas centrales de demanda; algunas empresas incluso enfrentan situaciones de entrega ajustadas. Mientras completan los pedidos existentes, las empresas realizan simultáneamente pequeñas acumulaciones previas a las festividades. En el lado de la capacidad, la nueva capacidad lanzada para fines de 2025 registró envíos parciales en enero. Si la producción posterior se estabiliza gradualmente, aliviará efectivamente la oferta ajustada de carbono duro para iones de sodio en la industria. El lado de la demanda también recibe nuevos puntos de crecimiento, ya que la demanda de clientes externos por ánodos de carbono duro se libera gradualmente, y la expansión exterior de las baterías de iones de sodio muestra una tendencia positiva. Afectada por las vacaciones del Año Nuevo Chino, se espera que la producción de ánodos de carbono duro caiga significativamente en febrero. SMM pronostica que la producción de febrero disminuirá un 47% mensual, manteniendo aún un crecimiento positivo del 10% interanual.

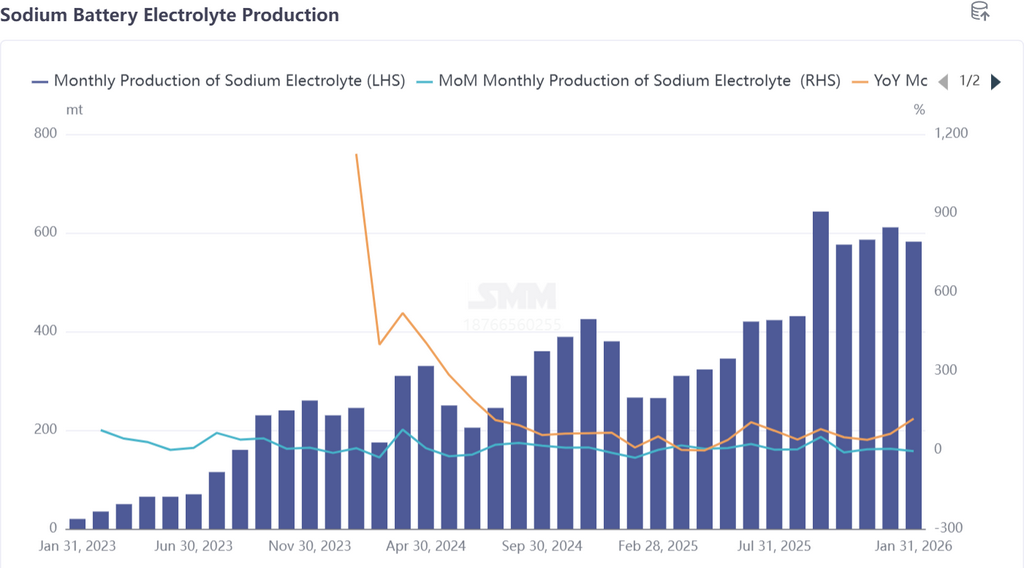

Electrolito para baterías de iones de sodio: Subidas de precios de materias primas impulsan los precios, la demanda de temporada baja suprime el rendimiento productivo

En enero, la producción de electrolito para baterías de iones de sodio cayó un 5% mensual pero aumentó un 119% interanual. El mercado continúa su lógica central de producir según la demanda; como los productos electrolíticos no son aptos para almacenamiento prolongado, la disposición de las empresas para acumular existencias previas a las festividades es mucho menor que para materiales de cátodo/ánodo. Los precios experimentaron ajustes menores: influenciados por aumentos previos de materias primas clave como NaPF6 y NaFSi, los precios del electrolito de iones de sodio subieron ligeramente. Sin embargo, los cambios de precios no son el factor central que afecta la producción; las células de baterías de iones de sodio aguas abajo que entran en la temporada baja de producción condujeron directamente a una contracción de la demanda de electrolito, convirtiéndose en la razón principal de la caída mensual en la producción. En febrero, la producción industrial enfrentará mayor presión. Debido a menos pedidos combinados con las vacaciones del Año Nuevo Chino, parte del personal de las líneas de producción de electrolito de iones de sodio podría ser reasignado a líneas de producción de baterías de litio. SMM espera que la producción de electrolito en febrero disminuya un 43% mensual pero aumente un 26% interanual.

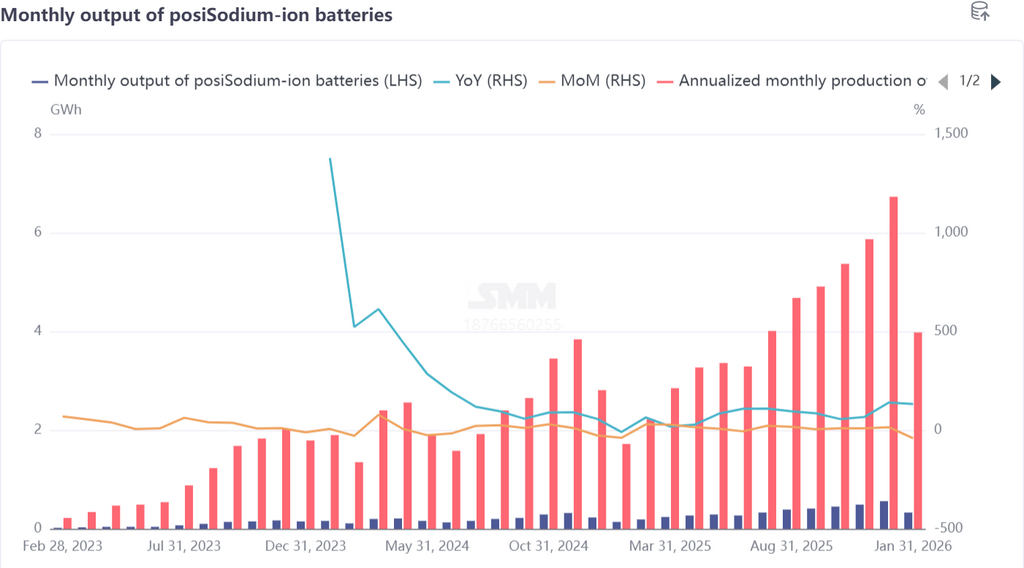

Células y Usuarios Finales: Caída de Producción en Temporada Baja, Subida del Precio del Carbonato de Litio Impulsa Expectativas del Mercado de Baterías de Iones de Sodio

En enero, la producción de células de baterías de iones de sodio disminuyó un 41% mensual pero aumentó un 132% interanual, ya que la industria entró oficialmente en la temporada baja de producción. Solo algunos proyectos de ESS mantuvieron las entregas según lo planeado, con pocos pedidos nuevos confirmados, lo cual es un fenómeno normal durante la transición de la industria entre temporadas altas y bajas. Sin embargo, la temporada baja trajo señales positivas: el aumento de los precios del carbonato de litio a principios de año incrementó los costos de las celdas de baterías de litio, junto con los lanzamientos más recientes de productos de baterías de iones de sodio por parte de las principales empresas de baterías. Las consultas del mercado y los pedidos esperados para celdas de baterías de iones de sodio aumentaron significativamente, y el sentimiento del mercado se volvió optimista al comenzar el año. A largo plazo, una gran cantidad de capacidad de producción de celdas de baterías de iones de sodio comenzará a operar en 2026. SMM espera que la producción de celdas de baterías de iones de sodio aumente gradualmente después del segundo trimestre, y se prevé que los costos de los productos disminuyan aún más debido a las economías de escala, sentando las bases para la expansión del mercado de baterías de iones de sodio en mercados clave como ESS. A corto plazo, el mercado de baterías de iones de sodio permanecerá débil en febrero, ya que las empresas de celdas programarán las vacaciones del Año Nuevo Chino. SMM estima que la producción de celdas de baterías de iones de sodio en febrero disminuirá un 40% mensual pero aumentará un 8% interanual.

Resumen: La industria mostró divergencia en enero, con suficiente impulso de crecimiento a largo plazo

En general, en enero de 2026, el ritmo operativo de la cadena industrial de baterías de iones de sodio se alineó con las características del mercado previas a las vacaciones. El significativo crecimiento interanual de la producción en toda la cadena industrial demostró plenamente la fuerte vitalidad de desarrollo de la industria de baterías de iones de sodio en su proceso de comercialización. La divergencia en el rendimiento mensual se debió principalmente a las diferencias segmentadas en la demanda de abastecimiento prevacacional, la supresión de la demanda durante la temporada baja tradicional de producción y las restricciones debido a la característica del producto de que el electrolito no es adecuado para almacenamiento prolongado.

A corto plazo, afectados por las vacaciones del Año Nuevo Chino, todos los segmentos de la cadena industrial de baterías de iones de sodio experimentarán disminuciones significativas de producción en febrero, entrando en un período de consolidación escalonado. Sin embargo, las expectativas de desarrollo industrial a largo plazo son positivas. El aumento de los precios del carbonato de litio a principios de año fortaleció aún más el papel de las baterías de iones de sodio como complemento de las baterías de litio. Los diseños de productos y los avances tecnológicos de las principales empresas continúan impulsando la confianza del mercado, junto con la puesta en marcha concentrada de la capacidad de producción de celdas de baterías de iones de sodio en 2026, lo que acelerará aún más el proceso de desarrollo a escala de la industria. A medida que la producción de celdas de baterías de iones de sodio aumente gradualmente después del segundo trimestre, la reducción de costos y la expansión del mercado formarán un ciclo positivo. La competitividad de las baterías de iones de sodio en campos como ESS y fuentes de alimentación de arranque-parada seguirá mejorando, y se espera que el ritmo de comercialización de la industria se acelere aún más.