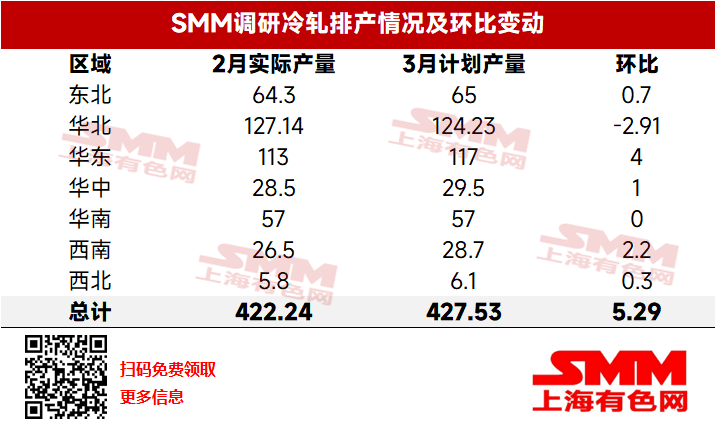

SMM Cold-Rolled Production Schedule:

Daily Average Cold-Rolled Production in March Decreased by 12,900 mt

According to the latest SMM tracking, the planned production of cold-rolled products by 31 mainstream cold-rolled steel mills in March totaled 4.2753 million mt, an increase of 52,900 mt or 1.3% compared to the actual production in February. On a daily average basis, with three more days in March compared to February, the daily planned production was 137,900 mt, down 8.5% MoM from the actual daily average production in February.

Table 1: Planned Production of Cold-Rolled Products by 31 Mainstream Cold-Rolled Steel Mills

Data Source: SMM Steel

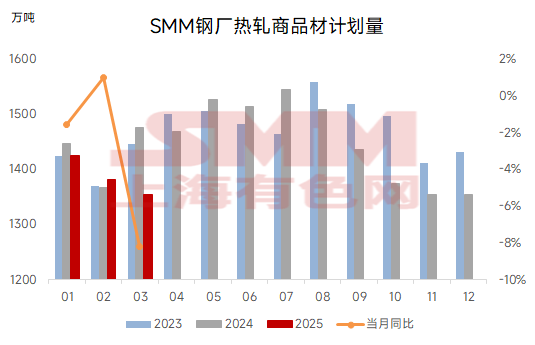

SMM Hot-Rolled Production Schedule:

Impact of Steel Mill Maintenance Rises Daily Average Hot-Rolled Production in March Decreased

According to the latest SMM tracking, the planned production of hot-rolled products by 39 mainstream HRC steel mills in March totaled 13.5438 million mt, a decrease of 203,700 mt or 1.5% compared to the actual production in February. On a daily average basis, with three more days in March compared to February, the daily planned production of hot-rolled products in March was 436,900 mt, down 54,100 mt or 11.0% MoM from the actual daily average production in February.

After sample expansion, the planned production of hot-rolled products by 51 mainstream HRC steel mills in March totaled 16.5138 million mt, with the daily planned production decreasing by 10% MoM from the actual production in February. Currently, steel mill production efficiency has improved, coupled with the seasonal demand boost from the manufacturing sector, leading to moderate production enthusiasm among steel mills. However, annual maintenance at some steel mills in north and south China has significantly reduced the planned hot-rolled production this month.

Chart-1: Planned Production of Hot-Rolled Products by New Sample Steel Mills

Data Source: SMM Steel

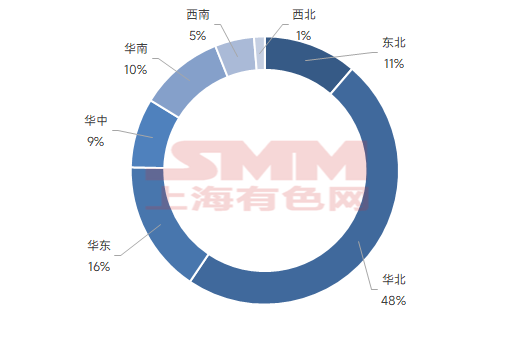

Chart-2: Regional Share of Planned Hot-Rolled Production by Mainstream Steel Mills Nationwide

Data Source: SMM Steel

By Domestic and Export Markets:

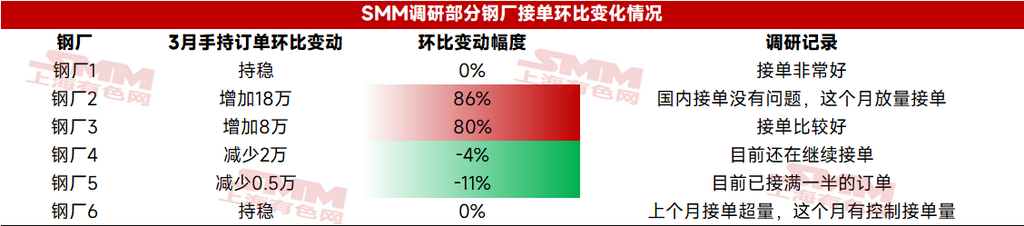

Domestic Trade: The planned domestic production of HRC in March was 12.3158 million mt, with a daily average of 397,300 mt, down 47,700 mt or 10.7% MoM from the actual daily average domestic production in February. In March, manufacturing demand showed strong resilience, and most steel mills reported good domestic order-taking. Considering the current similar profitability between coil and rebar production, some steel mills maintained stable HRC production without significant increases. However, the planned maintenance at some steel mills in north and south China led to a MoM decline in domestic HRC production in March.

Table 2: Comparison of Order-Taking by Some Steel Mills Surveyed by SMM

Data Source: SMM Steel

According to the SMM survey, as of March 6, the average order backlog of sample steel mills increased by 25% MoM, with many mills reporting good domestic order-taking. SMM will continue to track subsequent order-taking conditions.

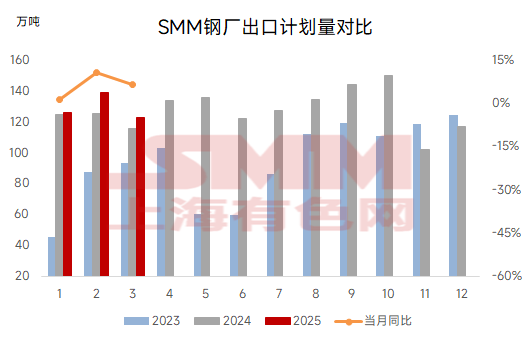

Export Trade: The planned export volume of HRC in March was 1.228 million mt, down 60,000 mt or 4.7% MoM from the actual export volume in February. The planned export volume of HRC by domestic steel mills in March saw a slight decline compared to February.

Regarding new orders, SMM learned that the intensive issuance of anti-dumping measures overseas after the Chinese New Year has heightened market concerns, with some overseas customers canceling orders, increasing export uncertainties and weakening recent order-taking by steel mills. Notably, the impact of Vietnam's anti-dumping measures has intensified. However, for specifications not subject to its sanctions, some steel mills have seen a significant improvement in recent export orders, with active inquiries.

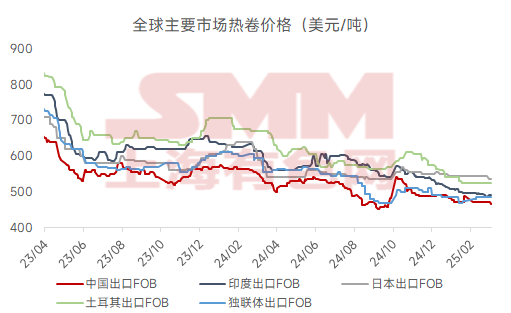

Chart-3: Comparison of HRC Export Prices in Major Global Markets

Chart-4: Planned Export Volume of Hot-Rolled Products by Sample Mainstream Steel Mills

Data Source: SMM Steel

Maintenance:

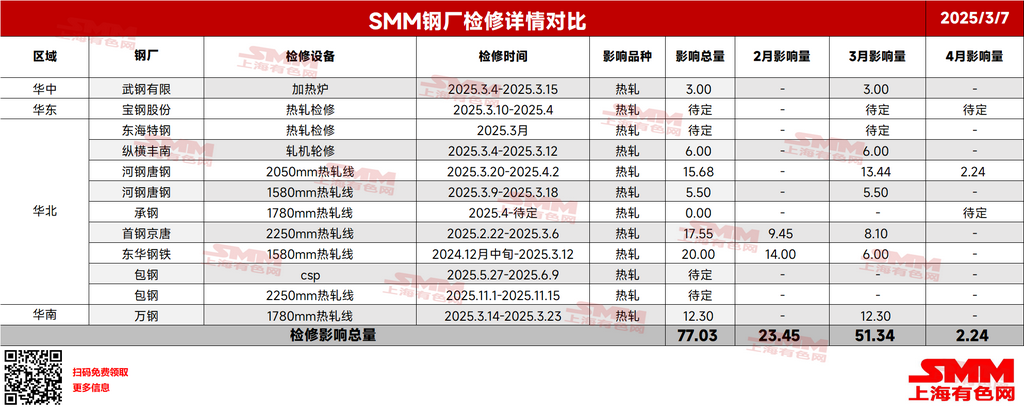

The impact of maintenance on HRC production in March was 513,400 mt, an increase of 278,900 mt MoM. The announced maintenance is mainly concentrated in steel mills in north, south, and east China. SMM will continue to track subsequent developments. Details of the maintenance are shown in the table below:

Table 3: Details of Maintenance at HRC Steel Mills

Data Source: SMM Steel

Profitability:

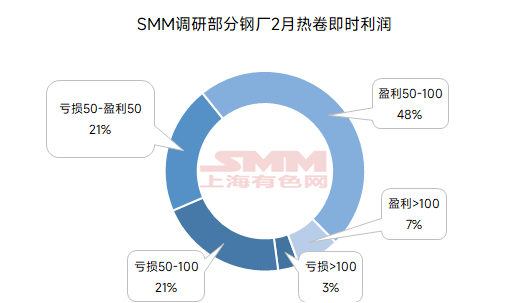

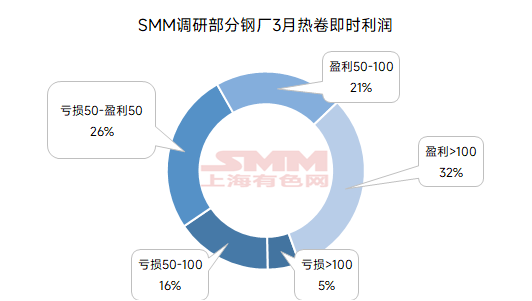

According to the SMM survey on real-time profit of steel mills producing HRC, most steel mills currently report real-time profits of 100 yuan/mt or more, showing an improvement compared to early February. Specifically, about 5% of steel mills reported current losses of over 100 yuan/mt, approximately 16% reported losses of 50-100 yuan/mt, 26% were at the break-even point, 21% reported profits of 50-150 yuan/mt, and 32% reported profits of over 100 yuan/mt. Chart-5: Real-Time Profit of HRC Production by Some Steel Mills Surveyed by SMM Over the Past Two Months

Summary

The daily average planned production of HRC by domestic steel mills in March decreased MoM compared to the actual production in February, mainly due to the impact of concentrated maintenance at some steel mills.

Looking ahead, HRC production in March is expected to decline, easing supply-side pressure. SMM's HRC inventory has already started to decrease this week. On the demand side, domestic order-taking by steel mills remains strong, with downstream operating rates steadily increasing in March-April. Coupled with low raw material inventories at downstream enterprises, demand for sheets & plates still has room for further growth, with relatively small imbalances in fundamentals.

On the macro side, the Two Sessions are currently underway, and the positive policies targeting steel consumption will take time to impact the market. Additionally, the NDRC recently reiterated the "continued implementation of crude steel production control," with increasing market news about policy-driven supply-side production cuts, providing some support for steel prices at the bottom. As March enters the peak demand verification period, with a "policy bottom" supporting prices below and increasing export sanctions above, the price range for HRC in March is expected to remain relatively limited without further news-driven stimuli.

![The most-traded BC copper contract closed down 2.85%, as speculative fervor cooled, weighing on copper prices [SMM BC Copper Review]](https://imgqn.smm.cn/usercenter/CYktX20251217171711.jpg)

![The Black Industrial Chain Lacked Upward or Downward Momentum Before the Holiday [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/FRcmT20251217171746.jpg)

![The most-traded SHFE tin contract plummeted more than 8% in a single day, and tin prices are expected to remain in the doldrums in the short term [SMM Tin Futures Review]](https://imgqn.smm.cn/usercenter/LLUUJ20251217171751.jpeg)