I. Both Rebar and HRC Profits Plunged in June

Since mid-to-late May, steel prices have trended lower amid weakening downstream transactions as the off-season set in. From June to date, SMM spot prices for rebar, hot-rolled coil (HRC), and cold-rolled plate in east China fell by 1.5% to 2% from May levels.

On the cost side, in June, the average of the 61% Fe port spot index fell 6.7% from May, while coke prices surged, with spot market prices up nearly 10% from May. Ore prices declined but coke prices strengthened, and steel scrap prices moved sideways. This resulted in average steel mill costs in June edging down only 0.1%–0.3% from May, while steel prices dropped far more than raw material costs, causing steel mill profits to narrow sharply.

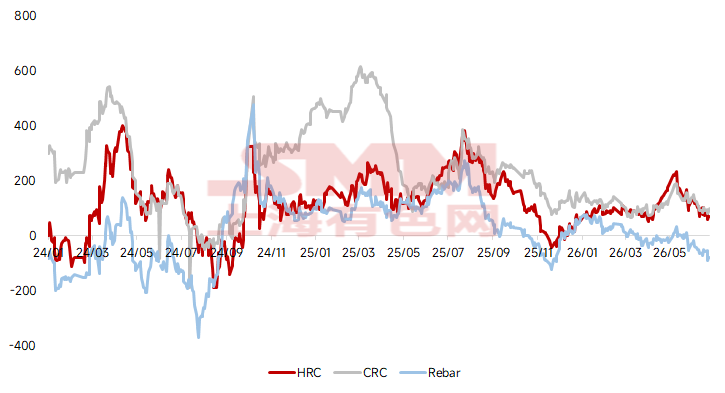

According to SMM data, as of June 25, profits at blast furnace steel mills in east China for rebar, HRC, and cold-rolled products all declined by varying degrees from their early-May peaks. Rebar mt profit dropped from 35 yuan to -80 yuan, down 328%; HRC mt profit fell from 232 yuan to 70 yuan, down 70%; and cold-rolled mt profit slipped from 192 yuan to 100 yuan, down around 48%.

Figure 1 – Profit Trends of Blast Furnace Steel Mills in East China

During this rapid profit contraction, the cost composition of pig iron shifted: the share of iron ore costs fell from 56% to 53%, the share of coke costs rose from 30% to 33%, while the share of PCI coal and other costs changed relatively little. Rising coke prices squeezed steel mill profit margins.

II. Profit Outlook

In the short term, on the steel side, end-use demand will be limited during the off-season, and inventories will gradually build up from July. Steel’s own fundamentals are unlikely to support price strength.

On the cost side, ore prices are expected to remain under pressure as the market anticipates that maintenance impacts at some regional steel mills could widen. For coke, spot prices still have a chance of seeing a ninth round of increases take effect. Overall, steel mill profits are expected to have some further room to narrow in the near term.

![[SMM Steel] Low Prices Spur Surge in Orders, Turkey's Kardemir Cuts Rebar Prices](https://imgqn.smm.cn/usercenter/crVox20251217171717.jpg)

![[Brazilian Steel Distributors Benefit From Antidumping Measures on China]](https://imgqn.smm.cn/usercenter/FFFrV20251217171719.jpg)

![[SMM Steel] SE Asia Import Billet Falls Further as Demand Stays Weak](https://imgqn.smm.cn/usercenter/aPBtI20251217171717.jpg)