Key Points: During the two-week period around the Chinese New Year (2026.2.13-2.26), the solid-state battery industry welcomed a triple breakthrough in "policy + standards + mass production": The National Energy Administration for the first time clearly identified solid-state batteries as a key direction in energy technology competition, and the national standard for vehicle solid-state batteries is on the verge of release (expected to be officially launched in July). On the industrial side, Xingjie Energy's 2GWh lithium metal solid-state battery production line went into operation and delivered satellite batteries, Chang'an Jinchongzhao solid-state batteries are set for Q3 vehicle validation, and Lingge Technology's hundred-ton-level sulphide whole-line tender win marks a breakthrough in the equipment sector. In 2026, solid-state batteries have fully transitioned from "laboratory stories" to being driven by "orders and mass production," with equipment leading, material positioning, and application differentiation becoming the main market trends.

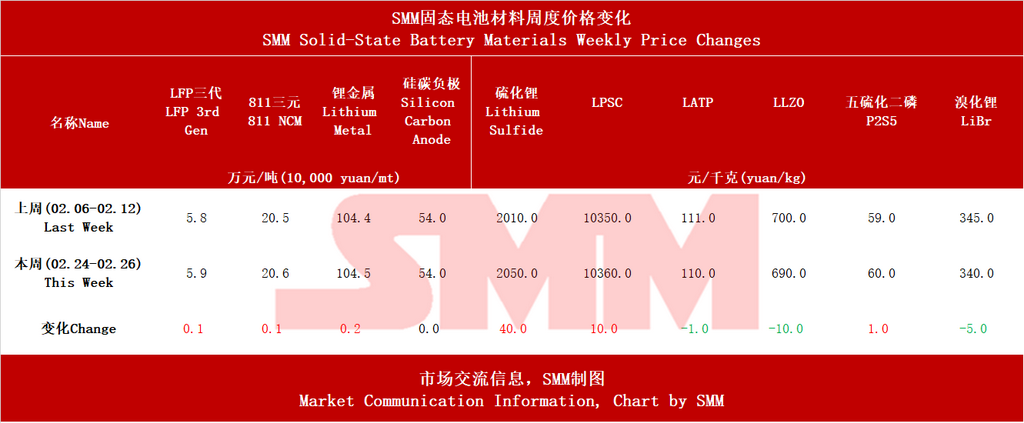

Preface: Biweekly price situation, during the period before and after the Chinese New Year holiday, there were some changes in solid-state battery material prices. Prices of traditional lithium battery shared materials in solid-state batteries rose due to the rebound in lithium chemical prices, while silicon carbon anode prices remained stable; in terms of electrolytes, battery-grade lithium sulfide and P₂S₅ prices increased, as did LPSC; oxide electrolyte and lithium bromide prices decreased.

I. Top-Level Design Sets the Tone: National Standards Imminent, Clear Policy Visibility

During this cycle, the policy level released two key signals. On February 23, Ren Yuzhi, Director of the Planning Department of the National Energy Administration, clearly stated that, against the backdrop of accelerating global energy transformation, cutting-edge areas such as solid-state batteries have become key directions for countries' layouts. This is the first time the national energy authority has elevated solid-state batteries to the core height of energy technology competition. Meanwhile, the standardization process for solid-state batteries is entering its final sprint: According to the China Automotive Technology and Research Center, the GB/T "Solid-State Batteries for Electric Vehicles - Part 1: Terminology and Classification" completed the draft for public comment in December 2025, expected to undergo review and approval in April 2026 and be officially released in July. The introduction of the standard will end the industry's "definition chaos," providing a technical basis for subsequent subsidy policies, safety certifications, and insurance claims, ushering in an era where industrialization is "regulated."

II. GWh-Scale Mass Production Lines Land Intensely, Application Scenarios Accelerate Diversification

In the two weeks following the Chinese New Year, domestic solid-state battery capacity construction showed a "multi-point blooming" trend. The most symbolic event was the full commissioning of Xingjie Energy's 2GWh lithium metal solid-state battery production line in Hangzhou on February 10, which is currently the largest capacity lithium metal solid-state battery project in China, with a total investment of 1 billion yuan. More noteworthy is its application breakthrough: the company has delivered batches of computing power satellite batteries, currently in the orbital validation stage, marking a substantial step towards the commercialization of solid-state batteries in the commercial aerospace field. At the same time, in the low-altitude economy sector, Ganfeng Lithium's 320Wh/kg high specific energy eVTOL battery completed a manned test flight on AEROFUGIA's AE200 model. In the new energy vehicle sector, Chang'an Automobile confirmed that the Jinchongzhao solid-state battery will complete robot and vehicle installation validation by Q3 2026, with an energy density of 400Wh/kg.

Regional capacity layout also accelerated. On February 24, Hunan Shengxin Technology's 60GWh next-generation lithium battery project in Ningxiang started construction, to be built in two phases, expected to meet the demand of about 1 million NEVs. Shandong Ruifu Lithium Industry's sulphide solid-state battery key material project was selected for the provincial technological transformation directory, focusing on battery-grade lithium sulfide (Li₂S). In Shanghang, Fujian, Zijin Mining's solid-state battery lithium battery new material construction project officially commenced. This round of capacity construction has moved from "pilot lines" to "GWh-scale production lines," and the judgment that 2026 will be a critical window for capacity release is being validated.

III. Equipment Sector Benefits First, Hundred-Ton Line Tender Validates "Equipment Leads" Logic

The equipment differences between solid-state and traditional liquid batteries are turning into definite orders. On February 11, Lingge Technology announced winning the bid for the first hundred-ton-level sulphide solid-state electrolyte continuous whole-line project, which can be rapidly expanded to a thousand-ton scale through modular replication, achieving the industry's first full-process whole-line engineering capability from design to commissioning. On the same day, Yuandian New Energy and High Energy Digital Manufacturing signed a 60 million yuan all-solid-state battery automation production line cooperation agreement, customizing solid-state battery production equipment. The change in equipment value is clear: according to Huayuan Securities, the front-end equipment value ratio for solid-state batteries has increased from 31% in traditional liquid to 35%-40%, and the mid-section from 40% to 40%-45%, with the combined front and mid-sections accounting for about 80%. The global solid-state battery equipment market size is expected to reach 12 billion yuan in 2026.

IV. International Competition and Cooperation: South Korea and France Accelerate Catch-Up, Technology Routes Converge

Overseas giants were also active during this cycle. Lotte Energy Materials in South Korea currently operates the world's largest pilot production line for sulphide solid-state electrolytes, with an annual capacity of 70 tons, and is collaborating with top global all-solid-state battery companies to evaluate scaling up to 1GWh. In France, ProLogium Technology's Dunkirk super factory broke ground on February 10, attended by President Macron, introducing the fourth-generation "super-fluidized all-inorganic solid-state lithium ceramic battery" technology, with mass production starting in 2028 and a total capacity of 12GWh by 2032. From a technology route perspective, the sulphide route is becoming the mainstream consensus in the industry—whether it's Lotte in South Korea, Ruifu Lithium in China, or ProLogium in Europe, all are tilting towards the sulphide direction.

V. Investment Mainline Analysis: Differentiation in Equipment, Materials, and Batteries

Based on the industry dynamics of this cycle, we reaffirm the three main lines of solid-state battery investment:

First, the equipment end has the highest certainty. Dry electrode, isostatic pressing equipment, and sulphide electrolyte continuous whole-line equipment are the largest incremental segments, and equipment suppliers tied to leading customers will be the first to realize performance. Focus on Nakanor (dry electrode equipment delivery to leading OEMs), Lingge Technology (sulphide whole-line tender win), and Lito Technology (warm isostatic pressing equipment).

Second, the material end is positioned on lithium sulfide and sulphide electrolytes. Lithium sulfide is the "bottleneck" in the sulphide route, and enterprises like Ruifu Lithium, Shanghai XiBa, and XTC New Energy Materials (Xiamen) possess scarcity. Silicon carbon anode and single-walled carbon nanotube usage increases, with Tianan Technology and BTR benefiting clearly.

Third, the battery end focuses on the differentiation of application scenarios. In the eVTOL sector, Ganfeng Lithium and Xingjie Energy are taking the lead, while in the power battery sector, CATL and BYD maintain their leadership, and automakers like Chang'an Automobile are following through self-research and cooperation. Players in emerging scenarios such as commercial aerospace and embodied robots are worth attention.

VI. Summary: Around the Chinese New Year, the Solid-State Battery Industry Slowed Down

In the two weeks following the 2026 Chinese New Year, the solid-state battery industry made efforts to express a "surge" announcement: the industrialization inflection point has arrived, but in reality, it still needs time. Increased policy visibility, dense landing of GWh-scale production lines, successive release of equipment orders, and multi-faceted application scenarios indicate that solid-state batteries are moving from "laboratory concepts" to being driven by "orders and mass production."

According to SMM forecasts, all-solid-state battery shipments will reach 13.5 GWh by 2028, while semi-solid-state battery shipments will reach 160 GWh. Global lithium-ion battery demand is projected to reach approximately 2,800 GWh by 2030, with the EV sector's lithium-ion battery demand showing a CAGR of around 11% from 2024 to 2030, ESS lithium-ion battery demand at a CAGR of about 27%, and consumer electronics lithium battery demand at a CAGR of roughly 10%. Global solid-state battery penetration is estimated at about 0.1% in 2025, with all-solid-state battery penetration expected to reach around 4% by 2030, and global solid-state battery penetration potentially approaching 10% by 2035.

**Note:** For further details or inquiries regarding solid-state battery development, please contact:

Phone: 021-20707860 (or WeChat: 13585549799)

Contact: Chaoxing Yang. Thank you!