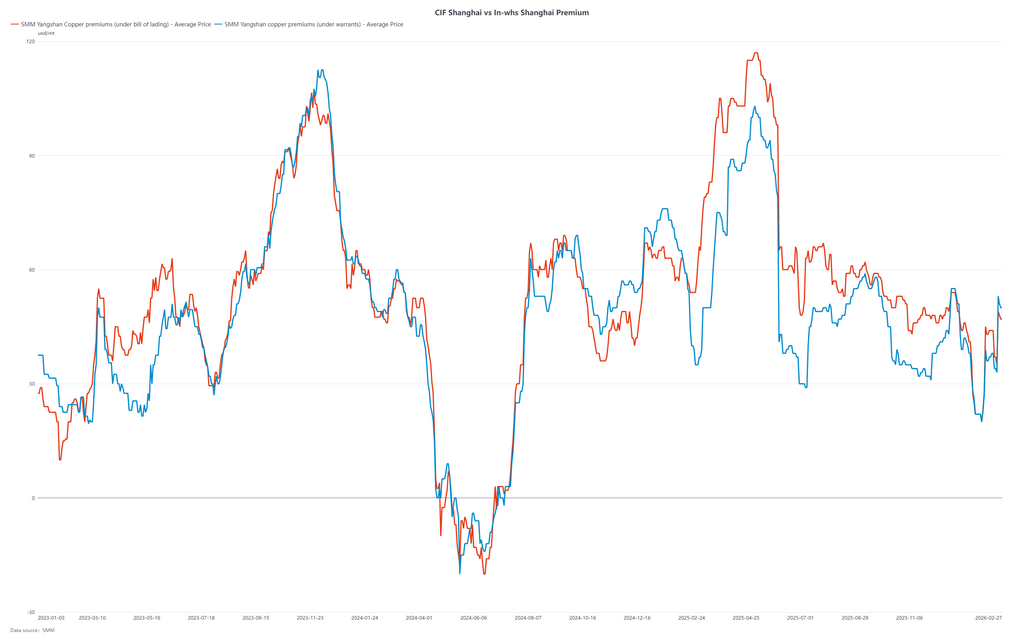

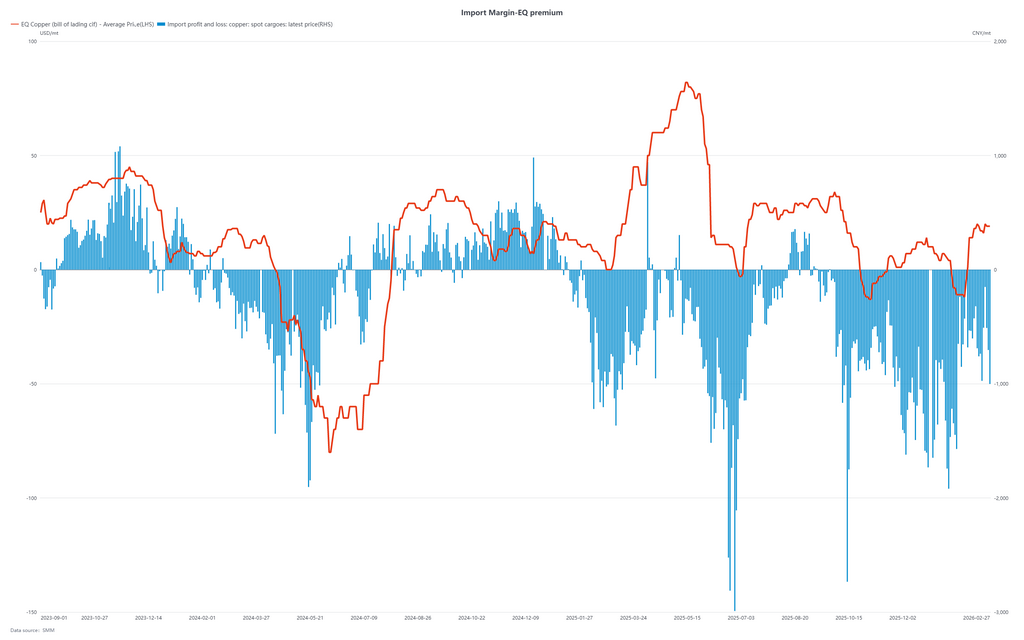

This week marked the first trading week after the Lunar New Year holiday. At the beginning of the week, the import window briefly opened, attracting importers to take cargo. However, as inventories both domestically and overseas continued to build significantly, the import window gradually closed thereafter.

Midweek, some traders showed short-term demand related to long-term contracts. With the LME contango structure still relatively deep, part of the market activity was driven by arbitrage opportunities. Aside from this, overall trading was subdued. As a result, premiums rose at the start of the week and then stabilized.

Looking ahead, post-holiday inventory builds exceeded expectations, and under high copper prices, the market will need time to absorb supply. Given that the proportion of 2026 long-term contracts remains relatively low, cargo circulation is expected to show greater volatility than in previous years. Arrivals in March–April are projected to decline, while implicit inventories at ports or bonded zones in regions such as Africa and Southeast Asia may increase.

According to SMM surveys, as of Thursday (February 27), copper inventories in China’s bonded zones increased by 200 tonnes WoW from February 13 to 72,200 tonnes.

-

Shanghai bonded inventories fell by 1,100 tonnes to 58,200 tonnes;

-

Guangdong bonded inventories rose by 1,300 tonnes to 9,400 tonnes.

During the holiday period, bonded inventories remained largely stable. Although port operations continued as usual, inland trucking logistics were suspended, and warehouse inbound and outbound activities were restricted, resulting in limited overall inventory fluctuations.

Looking ahead to next week, with no arbitrage opportunities in either import or export windows, bonded inventories are expected to remain within the current range.