Fed Hawkish Signals Exceed Expectations; Precious Metals Under Short-Term Pressure but Downside Limited

June 18 — At 2:00 AM Beijing Time on June 18, the Federal Reserve kept the federal funds rate unchanged at 3.50%-3.75%, marking the fourth consecutive hold. The statement was significantly shortened in length and removed language hinting at further rate cuts. The dot plot showed nine officials expect a rate hike this year, while newly appointed Chairman Warsh did not submit a dot plot and declined to provide forward guidance. Hawkish signals pushed market pricing for a year-end rate hike up to 38 basis points.

From a policy perspective, this FOMC meeting delivered hawkish signals that exceeded market expectations. Combined with the return of rate-hike expectations in the dot plot, it signals that the Fed's communication tone has shifted from "pause and watch" to "potential hiking," putting near-term pressure on precious metals. However, the fourth consecutive hold itself was in line with market expectations, and any actual rate hike still requires more data for validation, so the marginal impact of the policy signal itself is relatively limited.

More critically, earlier economic data — U.S. May nonfarm payrolls rose by 172,000, beating expectations, with a combined upward revision of 93,000 for March-April — underscores that labor market resilience remains the most significant headwind suppressing rate-cut expectations and is the core bearish factor for precious metals recently. By contrast, May headline CPI matched expectations while core CPI came in slightly below consensus, meaning inflation data did not reinforce the tightening narrative beyond expectations, and its bearish impact is comparatively moderate.

On balance, precious metals face dual pressure from hawkish policy signals and labor market resilience, but the elevated rate-hike expectations are still in the pricing-in phase, and the market may not form a systemic downward resonance at current levels. The trading logic will continue to hinge on subsequent nonfarm payrolls, CPI data, and actual communication from Warsh.

US-Iran Peace Talks Advance; Geopolitical Risk Premium Unwinds

June 18 — The presidents of the United States and Iran have signed an electronic memorandum of understanding (MoU). The official 14-point text largely matches prior media disclosures, and both sides are set to formally sign the agreement in Switzerland on Friday. Trump stated that if follow-up implementation of the MoU falls short of satisfaction, bombing operations would resume, and also revealed discussions with Syrian leaders on striking Hezbollah. Meanwhile, southern Lebanon witnessed multiple Israeli attacks, and Israel's finance minister indicated no withdrawal on Friday or thereafter. The geopolitical situation remains in a complex tug-of-war characterized by "negotiations alongside conflict."

In the near term, the signing of the MoU marks a substantive phase in ceasefire negotiations, with market expectations for the reopening of the Strait of Hormuz strengthening, leading to further unwinding of the risk premium. Should the formal agreement be finalized on Friday, structural concerns over crude supply would materially ease, putting downward pressure on the oil price center, which in turn would cool global inflation expectations.

From a medium-to-long-term perspective, if sustained oil weakness drives down energy costs, the Fed's monetary policy room would reopen, and market logic could gradually shift from "tightening expectations" toward a "rate-cut cycle," potentially offering new macro support for precious metals. Overall, US-Iran relations are currently in a phase of "peace talks advancing, conflicts unresolved," and market pricing will revolve around Friday's agreement implementation and subsequent execution risks in a repeated back-and-forth manner.

Early Hiking Cycle Pressure Does Not Alter Long-Term Logic; Precious Metals' Allocation Value Remains Prominent

Historical experience shows that in the early stages of every rate-hiking cycle, precious metals typically come under pressure from rising nominal rates and a stronger dollar, but the trend is not unidirectional downward. As the hiking cycle deepens, growing concerns over recession risks and liquidity stress increasingly highlight gold's role as an inflation hedge and safe-haven asset, with its price center tending to rise in the middle-to-late stages. Therefore, even if the Fed continues on a hawkish path, the pressure on precious metals may not be sustained; liquidity conditions and shifts in macro expectations also influence price dynamics.

Of course, our overall bullish long-term logic for precious metals remains unchanged: First, global central banks continue to accumulate gold, with de-dollarization and reserve diversification strategies providing a solid floor for gold prices. Second, the U.S. dollar's credit system faces deep erosion — high interest rates on U.S. Treasuries imply high risk, and over the long run, U.S. debt rollover pressures and fiscal indiscipline are accelerating global de-dollarization. Third, the ever-expanding U.S. government debt stock and deteriorating fiscal sustainability raise the risk of future debt monetization and dollar depreciation. As a non-liability, supra-sovereign hard asset, gold's safe-haven and store-of-value functions hold irreplaceable appeal in the current macro environment.

At the same time, geopolitical conflicts continue to simmer without truly subsiding, while global supply chains and energy markets remain volatile, with inflation persistence lingering. These uncertainties will collectively underpin the demand for gold and silver as safe-haven allocation assets, further boosting their strategic value over the medium-to-long term.

From the Gold/Silver Ratio Perspective: Silver Under Pressure in the Short Term, but Outperforming Gold in the Medium-to-Long Term Remains Intact

Historically, the gold/silver ratio exhibits significant mean-reverting behavior, with its long-term center roughly fluctuating between 60 and 70. However, under extreme macro environments, it can deviate markedly — for instance, the ratio widened sharply after the 2008 financial crisis and approached a historical extreme near 120 during the 2020 pandemic. The underlying dynamic is that during extreme risk-off episodes, the market prioritizes gold as a safe-haven asset, while silver, burdened by its industrial metal characteristics, tends to face systematic selling. Thus, the gold/silver ratio's cyclical movement can be summarized as: widening during crises (silver underperforms) and narrowing during recovery/inflation cycles (silver outperforms). Its essence is a cyclical indicator driven by the alternating dominance of safe-haven attributes versus industrial attributes.

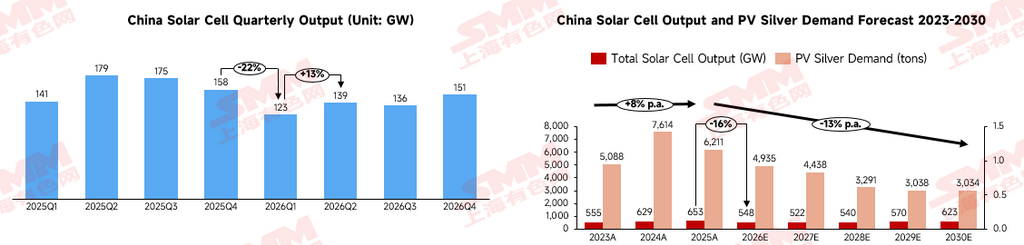

In the near term, the gold/silver ratio is more prone to stage-wise upward moves or range-bound drift with an upward bias. On one hand, silver has already posted notable gains, with crowded positioning making it more vulnerable to pullback pressure. On the other hand, the photovoltaic industry — a key pillar of silver industrial demand — is expected to see cell silver consumption decline by 9.51% year-over-year in 2026, and with ongoing silver-reduction progress and evolving cell product structures, annual silver consumption is projected to maintain a roughly 5 percentage-point decline through 2030.

Although positive terminal installation expectations may boost cell production volumes, translating to some incremental demand, when converted to silver demand, a roughly 20% decline is anticipated this year.

Over the long cycle, 2026 also marks a pivotal turning point in silver's industrial demand structure. The low-voltage electrical equipment sector, as a rigid support segment, exhibits strong irreplaceability in its silver demand. Emerging sectors such as new energy vehicles, PCBs, and SiC chips are rapidly expanding their end-market bases, and despite unchanged unit silver consumption, overall demand continues to grow steadily.

Therefore, we maintain our core view that the gold/silver ratio will trend downward in the medium-to-long term — i.e., we are constructive on silver outperforming gold. The driving logic will gradually shift from rates and liquidity toward energy transition and industrial demand. Silver is transforming from a traditional precious metal into a strategically important industrial metal with rising exposure to photovoltaics, AI data centers, and grid upgrades, while supply remains highly inelastic due to its heavy dependence on lead-zinc and copper byproduct production. Once the global economy enters a rate-cutting cycle or real rates decline, silver's industrial elasticity will significantly amplify its upside potential, whereas gold, supported more by central bank buying and safe-haven demand, tends to follow a smoother trajectory.