[SMM Hot Topic] Middle East Steel Export Flows Shift: Finished Products Stall and Steel Billet Counterattacks

Looking back at 2025, the Middle East market was undoubtedly the most dazzling "emerging dynamic market" in China's overseas steel landscape. In 2025, China's total steel exports to the Middle East reached 15.81 million mt, with monthly shipments basically stable in the high range of 1.2–1.3 million mt. Against the backdrop of total annual steel exports of 134 million mt, up 14% YoY, the Middle East market accounted for 11%–12% of China's total overseas steel export share. This means that in a single geo-economic region, its share and strategic reliance were second only to Southeast Asia, serving as the "second largest core pillar" for China's steel going global. In terms of product mix, high-added-value HRC (29% share), steel pipes essential for oil and gas projects (18% share), and medium-thickness plates (14% share) formed the three dominant players, reflecting the region's strong diversified industrial and infrastructure throughput capacity. However, it was precisely due to such a massive trade base in 2025 and high reliance on conventional Persian Gulf shipping lanes that when geopolitical storms suddenly struck and straits were dramatically blocked, the resulting "broad market stall" and supply chain disruption were so severe. Below, we will analyze in order: the specific situation of China's steel exports to the Middle East, how cargo pressure was shifted through port replacements during the strait blockade, and how the export landscape will be reshaped after the latest US-Israel negotiations?

The "Stall" and Structural Anomaly of China's Steel Exports to the Middle East

Data Source: SMM, China's General Administration of Customs

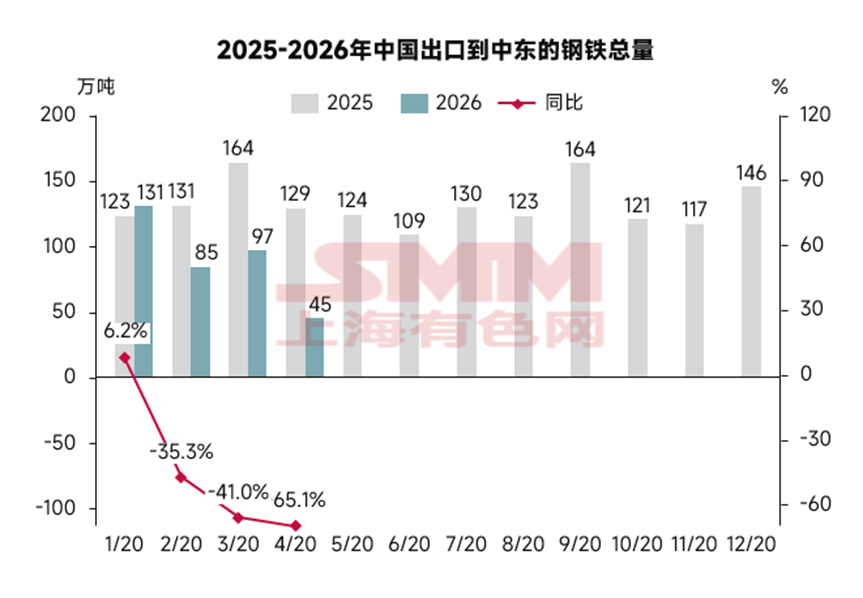

First, let's look at total export performance. According to SMM historical data and the latest customs export trends, China's total steel exports to the Middle East in the first four months of 2026 plummeted from 5.47 million mt in the same period of 2025 to 3.57 million mt, with April exports directly halving.

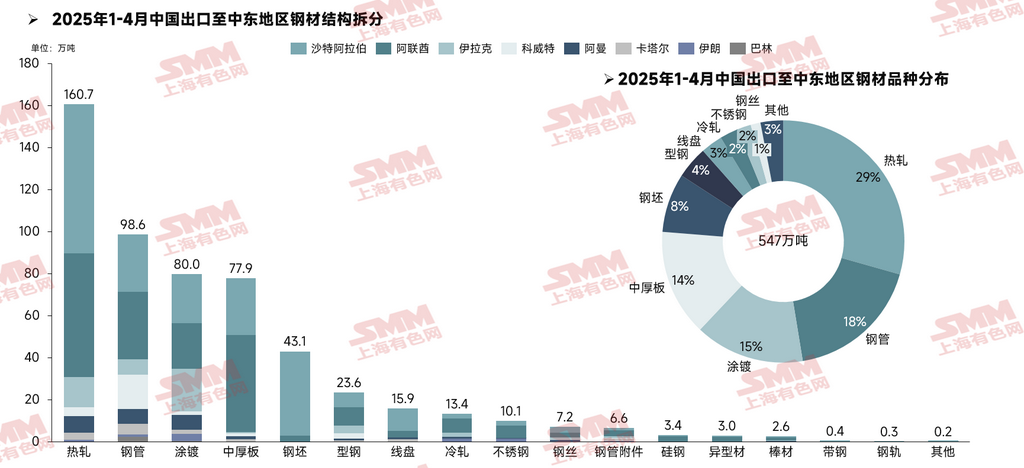

Specifically, among China's 5.47 million mt of steel exports to the Middle East from January to April 2025, a highly advanced finished-product-oriented export characteristic was evident. HRC (29%), steel pipe (18%), coated steel (15%), and medium-thickness plates (14%) constituted the four mainstays of China’s steel trade. In terms of destination countries, Saudi Arabia’s rigid demand for offshore/oil & gas pipe (986,000 mt) and the UAE’s strong processing throughput of general HRC (1.607 million mt) and medium-thickness plates (779,000 mt) jointly established the traditional “dual-core consumption hinterland” within the Persian Gulf.

Data source: SMM, General Administration of Customs of China

Supply Shock and Physical Scissors Gap: The “Billet Export Bonanza” Under a Double Squeeze

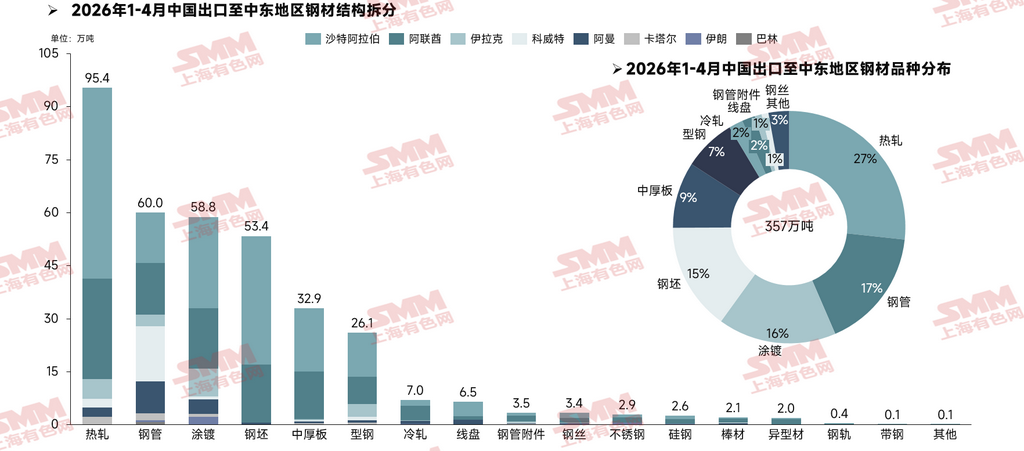

Since the start of 2026, the blockade of the Persian Gulf Strait caused by geopolitical conflicts significantly weakened overall shipments, while a dramatic “underlying mutation” simultaneously unfolded in the product mix. Steel billet, a minor product that previously accounted for only an 8% share (431,000 mt), registered a strong countertrend increase of 24% in the first four months of 2026. According to the SMM survey, the underlying driver of this anomaly originated from a localized supply shock induced by geopolitical shifts in Iran.

If the closure of the Persian Gulf Strait severed the “aorta” of Middle Eastern steel imports, the sudden destruction of Iran’s two largest steel giants—Mobarakeh Steel Company (MSC) in Isfahan and Khuzestan Steel Company (KSC)—on March 27, 2026, completely ignited a “raw material upheaval” within the region. Iran is the world’s tenth-largest and the Middle East’s largest crude steel producer (accounting for over 50% of the region’s total crude steel output), with annual steel exports exceeding 10 million mt, among which semi-finished steel billets are the absolute mainstay. Mobarakeh (MSC) has an annual capacity of 11.8 million mt (20% of Iran’s total capacity), making it the undisputed “King of Flat Products/Sheets & Plates” in the Middle East; Khuzestan (KSC) is Iran’s second-largest steel producer and its most critical production base for slabs and billets.

Data source: SMM, General Administration of Customs of China

Under normal conditions, Iran was the primary supplier of low-priced steel billets to local rolling mills in the Middle East. With the sharp contraction in Iran's external supply, rolling mills in the Middle East, particularly in Oman and parts of the UAE outside the Gulf that were not directly affected by the blockade, faced severe raw material supply disruption risks. To maintain production, local buyers quickly released a large number of urgent inquiries to the international market. According to SMM survey, the huge demand gap for steel billets created by Iran's exit was filled and shared by supplies from China, India, and Russia. Because the local shortage was mainly crude steel raw material for rolling sheets and plates, and the equipment destruction from explosions meant that rolling lines were the first to restart, the main incremental product in these counter-trend orders was steel slab.

This situation shares similarities with the article at https://mp.weixin.qq.com/s/bsrZaRRSRDHC_FmGLulJOQ (Middle East turmoil triggers "mismatch", China accelerates filling a supply vacuum of about 2.3 million mt in Southeast Asia), which mentioned that China would accelerate taking over steel billet supply gaps. That is, despite the decline in steel exports this year, billet exports also achieved counter-trend growth.

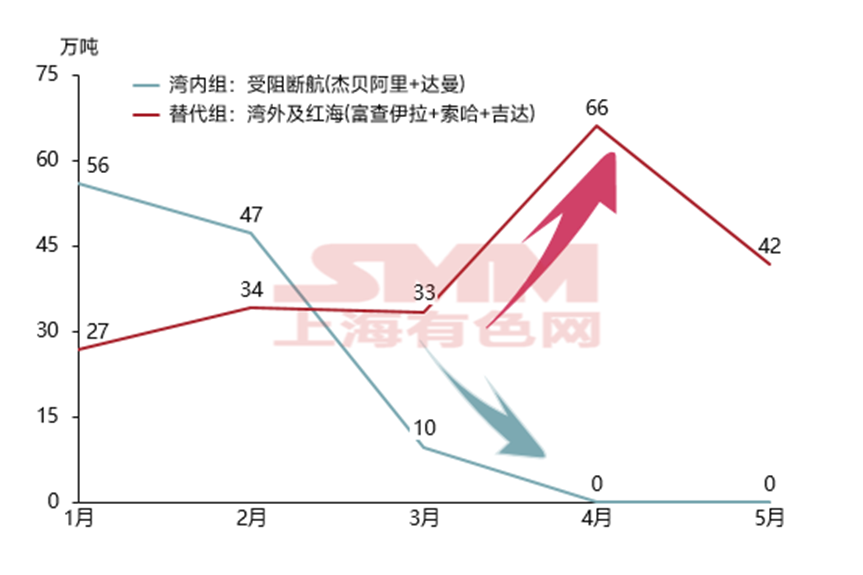

Stock Game: The "X-Shaped Crossover" of Inside-Gulf Shutdowns and Outside-Gulf Safe Havens

Verified by SMM through freight forwarders, steel trade (especially medium-thickness plates, pipes, and steel billets) relies heavily on bulk or breakbulk vessels. When container liners encounter blockades, they can easily reroute by amending bookings via computer systems, but the diversion of bulk carriers faces rigid constraints from destination port drafts, specialized handling equipment (such as large quay cranes), and inland truck connections. Therefore, over the past two months, the supply chain staged a dramatic "port drift" inside and outside the Persian Gulf. The following uses SMM's panoramic shipping data to explain in detail the changes in cargo flow between ports.

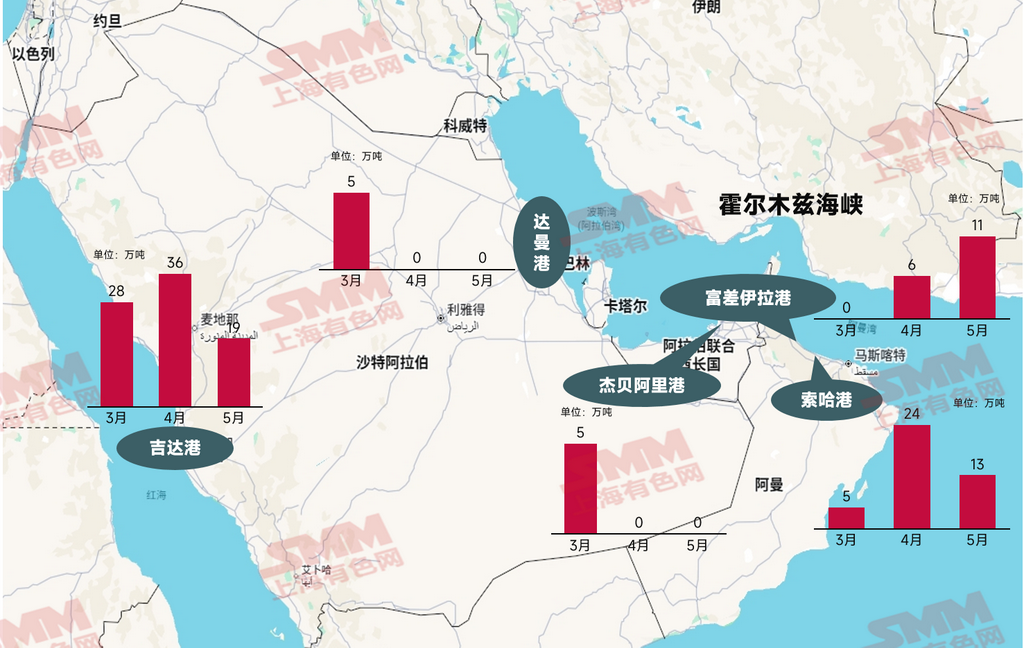

Under normal conditions, over 70% of China's steel shipments to the Middle East converged densely on Jebel Ali Port inside the Persian Gulf and Dammam Port on the eastern coast of Saudi Arabia. But after the strait blockade, steel port arrivals at these two traditional hubs showed a historic "physical shock" in SMM's high-frequency shipping data (falling to zero from April to May).

Meanwhile, the diverted cargo, fighting to survive, surged wildly toward alternative ports outside the strait, tearing open a "lifeline of safety" spatially:

① "Overload Surge" at Oman's Port of Sohar: As the most critical cross-border multimodal transshipment hub outside the Gulf, its port arrivals in April surged nearly fivefold MoM. Large batches of Chinese HRC and steel billet originally destined for the inner Gulf were forced ashore here, causing massive congestion at the port in May as cross-border heavy truck capacity collapsed.

② "Western Route Counterflow" at Saudi Arabia's Jeddah Port: Saudi Arabia abandoned its eastern sea route (Dammam Port) nationwide, forcibly redirecting all Chinese orders to Jeddah on the Red Sea side, causing its throughput to surge to a peak of 361,000 mt in April.

Source: SMM, Google Maps

However, it should be noted that while cargo can be transferred via other ports in the short term, port arrivals in May have already shown a weakening trend again. The reason is that alternative ports outside the Gulf simply cannot handle such massive and concentrated cargo volumes, leading to extremely severe congestion. According to SMM's survey, because navigation within the Gulf is no longer possible, some shipping lines originally bound for Jebel Ali had to divert to Fujairah, but are still queuing for berths. Jeddah Port faces similar issues. With tight capacity, prices keep surging, and transportation faces severe obstacles.

Source: SMM

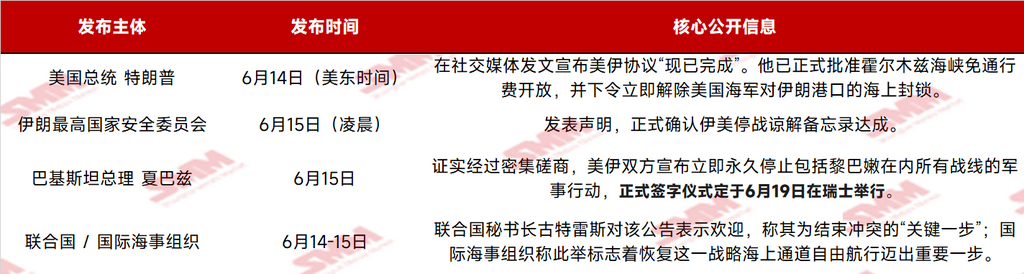

After 108 days of the "dual blockade" (Iran's blockade of the strait and the US's counter-blockade of Iranian ports) that gripped the lifeline of global energy and commodities, the US and Iran officially issued successive high-profile statements announcing a ceasefire memorandum of understanding. The relevant timeline is summarized below.

Data source: Compiled by SMM from public channels

The news, once released, triggered a strong market reaction. On one hand, there are expectations for export increments from shipping recovery; on the other hand, there are certain demand expectations for post-disaster reconstruction.

According to the latest SMM survey, most exporters have not responded enthusiastically to the lifting of the blockade and remain skeptical about its actual implementation. Therefore, from the perspective of actual order-taking, shipments to the Middle East still need 3 to 4 weeks to be verified. If a full lifting is confirmed, the "demand backlog" caused by the earlier shipping disruptions will see a concentrated release. Based on past customs data and the local supply-demand balance table, SMM roughly predicts that finished steel products will experience strong growth expectations, potentially filling a disaster-induced gap of approximately 1.7-2.1 million mt. Among them, HRC accounts for the highest proportion (29%) of China's finished steel exports to the Middle East. Although the Middle East's largest flat steel giant, Iran's Mobarakeh Steel Company (MSC), has reported production resumptions for its blast furnace previously damaged by war, its capacity is in a post-disaster repair phase and is not expected to fill the local gap in the short term. However, recent market rumors suggest that Indian resources are seizing the Middle Eastern market at lower prices, which will also pose some impact on China's export order-taking.

However, for semi-finished products, the reason Chinese steel billets have been "hot" in recent months is the supply gap caused by the strait blockade and the bombing of Iranian steel mills. Once Iran's logistics fully recover, Chinese steel billets will lose their advantage in absolute price, logistics distance, and surrounding multilateral competition, and the demand gap in Southeast Asia previously filled by substituting Iranian sources may also be reclaimed. Recently, according to SMM surveys, billet resources are already circulating in the Middle Eastern market. Through the following comparison of comprehensive landed costs (CFR) for billets in the Middle East, it can be clearly seen that Chinese resources are under comprehensive pressure:

Therefore, steel billet exports to the Middle East are expected to be somewhat limited, with competition only possible at lower prices. Preliminary forecasts indicate a pressure reduction of 50,000–250,000 mt.

However, we need to broaden our perspective to the global multilateral trade context, and we must not fall into excessive pessimism due to localized marginal reductions. Although the billets exported to the Middle East are under pressure, the incremental steel billet volumes that previously replaced Iranian exports to Southeast Asia may not necessarily be wiped out. Given the uncertainty of the Middle East situation and based on considerations of a more stable supply chain, Southeast Asian buyers may continue to source from Chinese suppliers. Therefore, against the backdrop of an overall steel recovery and resilience in steel billet prices, SMM maintains its earlier view, holding a moderately optimistic stance on annual steel exports, with expectations of "steady incremental growth."

Finally, it needs to be added that, currently, due to severe port congestion, even if the strait is confirmed passable, it will still take a long time for actual cargo to arrive and cannot immediately be reflected in the data. At the same time, ocean freight rates will also maintain high-level fluctuations in the short term due to unfavorable port cargo pick-up. SMM will continue to track subsequent developments...

Copyright and Intellectual Property Statement:

This report is independently created or compiled by SMM Information & Technology Co., Ltd. (hereinafter referred to as "SMM"), and SMM legally enjoys complete copyright and related intellectual property rights.

The copyright, trademark rights, domain name rights, commercial data information property rights, and other related intellectual property rights of all content contained in this report (including but not limited to information, articles, data, charts, pictures, audio, video, logos, advertisements, trademarks, trade names, domain names, layout designs, etc.) are owned or held by SMM or its related right holders.

The above rights are strictly protected by relevant laws and regulations of the People's Republic of China, such as the Copyright Law of the People's Republic of China, the Trademark Law of the People's Republic of China, and the Anti-Unfair Competition Law of the People's Republic of China, as well as applicable international treaties.

Without prior written authorization from SMM, no institution or individual may:

1. Use all or part of this report in any form (including but not limited to reprinting, modifying, selling, transferring, displaying, translating, compiling, disseminating);

2. Disclose the content of this report to any third party;

3. License or authorize any third party to use the content of this report;

4. For any unauthorized use, SMM will legally pursue the legal responsibilities of the infringer, demanding that they bear legal responsibilities including but not limited to contractual breach liability, returning unjust enrichment, and compensating for direct and indirect economic losses.

Data Source Statement:

(Except for publicly available information, other data in this report are derived from publicly available information (including but not limited to industry news, seminars, exhibitions, corporate financial reports, brokerage reports, data from the National Bureau of Statistics, customs import and export data, various data published by major associations and institutions, etc.), market exchanges, and comprehensive analysis and reasonable inferences made by the research team based on SMM's internal database models. This information is for reference only and does not constitute decision-making advice.

SMM reserves the final interpretation right of the terms in this statement and the right to adjust and modify the content of the statement according to actual circumstances.

![[SMM HRC Daily Trading Volume] Spot trading pulled back significantly](https://imgqn.smm.cn/usercenter/GGaSo20251217171716.jpg)