SMM, June 18:

Metals markets:

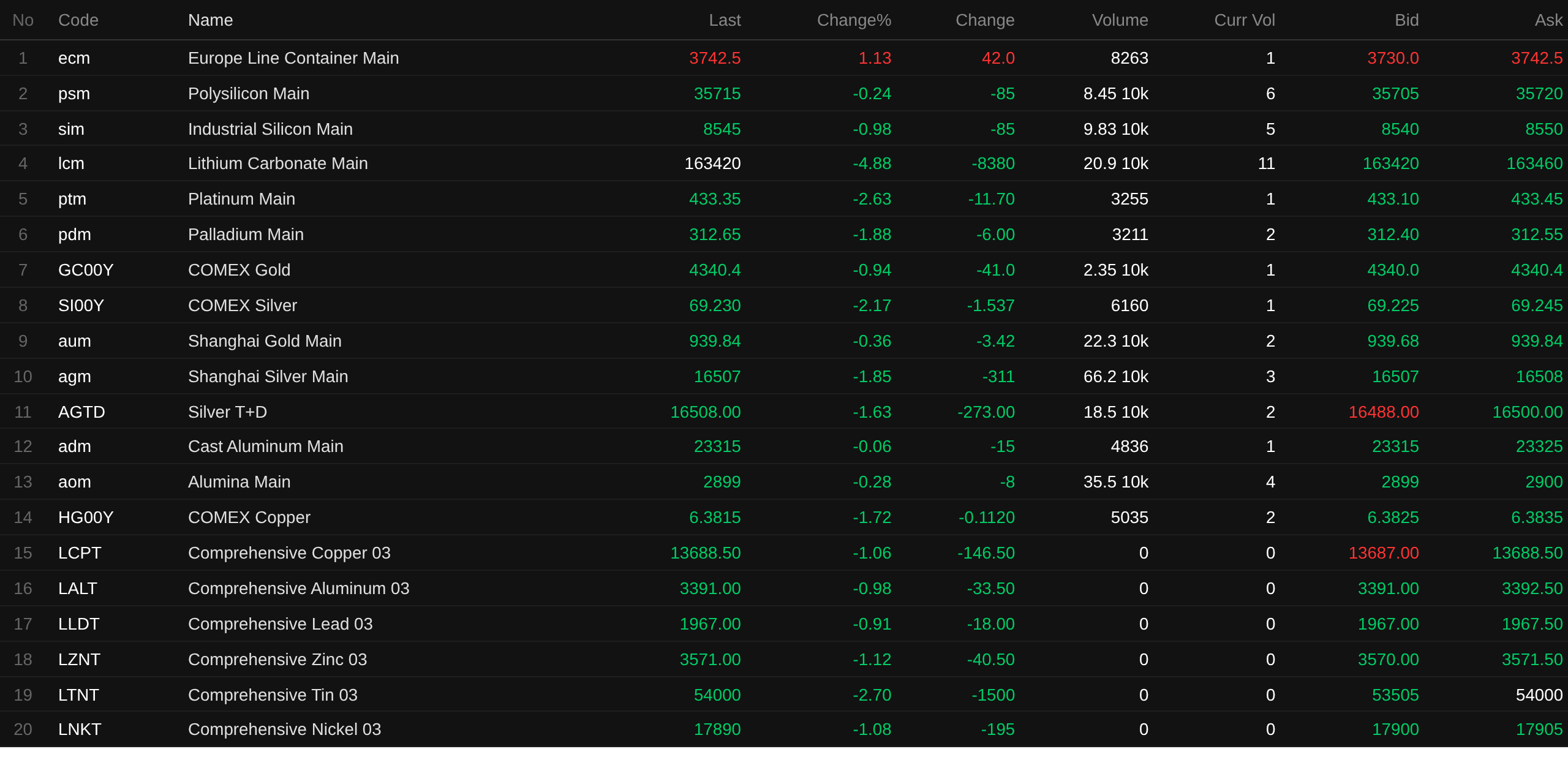

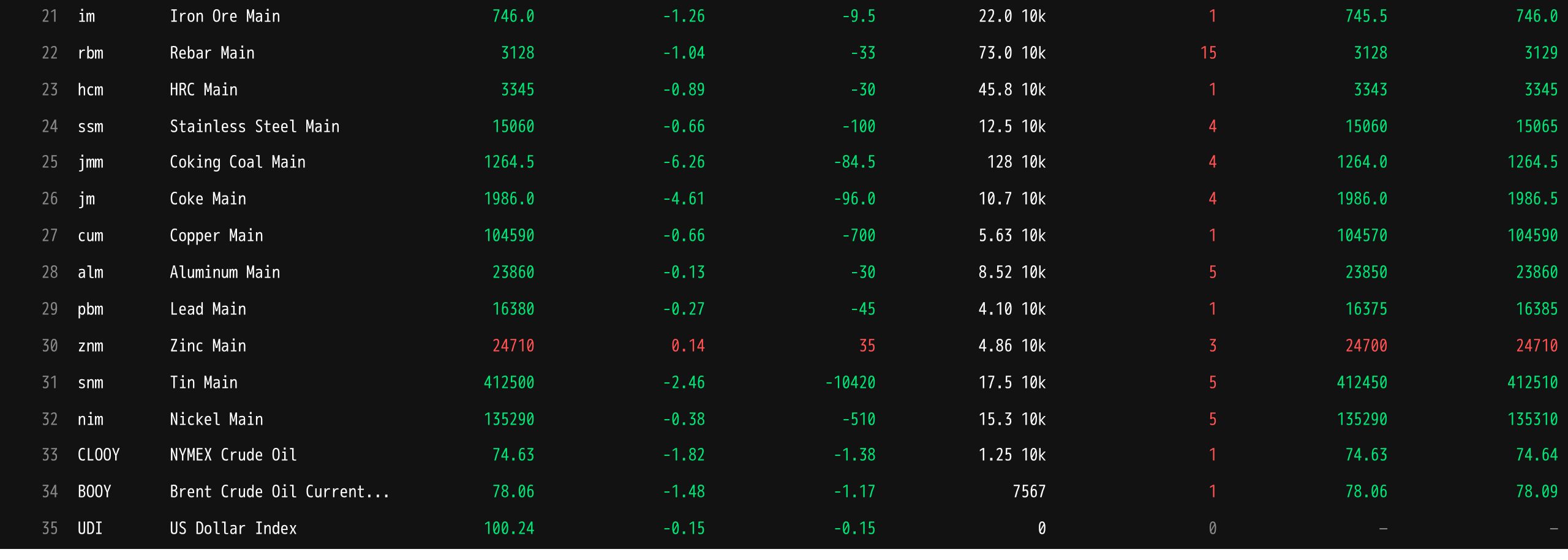

As of midday close, base metals on the domestic market were nearly all down. SHFE copper fell 0.66%, SHFE aluminum fell 0.13%. SHFE lead fell 0.27%. SHFE zinc rose 0.14%. SHFE tin fell 2.46%. SHFE nickel fell 0.38%.

In addition, the most-traded cast aluminum futures edged lower, the most-traded alumina futures fell 0.28%. The most-traded lithium carbonate futures fell 4.88%. The most-traded silicon metal futures fell 0.98%. The most-traded polysilicon futures fell 0.24%.

Ferrous metals all fell. Iron ore fell 1.26%, rebar fell 1.04%, HRC fell 0.89%, and stainless steel fell 0.66%. Coking coal and coke: the most-traded coking coal futures contract fell 6.26%, and the most-traded coke futures contract fell 4.21%.

On the overseas base metals front, as of 11:45, LME metals fell across the board. LME copper fell 1.06%, LME aluminum and LME lead fell nearly 1%. LME zinc fell 1.12%, LME tin fell 2.7%. LME nickel fell 1.08%.

Precious metals: as of 11:45, COMEX gold fell 0.94%, and COMEX silver fell 2.17%. Domestic precious metals: the most-traded SHFE gold futures fell 0.36%, and the most-traded SHFE silver futures fell 1.85%.

In addition, as of midday close, the most-traded platinum futures fell 2.63%, and the most-traded palladium futures fell 1.88%.

As of the midday close, the most-traded container shipping freight futures (European route) rose 1.13% to 3,742.5 points.

As of June 18, 11:45, selected futures midday quotes:

Spot and fundamentals

Zinc: The mainstream brand 0# zinc traded around 24,680-24,790 yuan/mt in the Ningbo market. Ningbo regular brands were quoted at a discount of 20 yuan/mt against the 2607 contract, and at a premium of 30 yuan/mt against Shanghai spot cargoes. The mainstream in Ningbo was quoted against the 2607 contract...

Macro front

Domestic side:

[Five Departments: Launch of 2026 NEV Promotion Campaign in Rural Areas] The General Offices (Comprehensive Departments) of the Ministry of Industry and Information Technology, the Ministry of Commerce and three other departments are launching the 2026 NEV promotion campaign in rural areas, deepening the auto trade-in program in villages. Within the NEV rural promotion campaign, a trade-in special section will be set up to publicize and promote subsidy policies, and provide "one-stop" services such as old vehicle inspection, evaluation and recycling, and assistance with subsidy applications, to further increase policy awareness and coverage and facilitate rural consumers' participation and access to subsidies. Rural consumers who trade in old cars for NEVs can apply for auto trade-in subsidies according to policy requirements, without any limit on the number of subsidy qualifications.

[NDRC: to Strengthen Coordinated Planning of Computing Power Network, New-Type Power Grid, and New-Generation Communication Network During 15th Five-Year Plan Period] Li Chao, Deputy Director of the Policy Research Office and Spokesperson of the National Development and Reform Commission (NDRC), said at a press conference that during the 15th Five-Year Plan period, greater emphasis will be placed on supply-demand matching and coordinated planning and construction of the computing power network, new-type power grid, and new-generation communication network. On the "hard investment" front, more effective computing-electricity synergy models will be explored to strengthen computing with electricity and promote electricity with computing; computing-network integration innovation will be enhanced, and direct connection lines between national hubs will be appropriately expanded to further reduce network transmission latency. On the "soft development" front, the monitoring and market-based scheduling of computing resources will be strengthened, and the construction of a nationwide integrated computing power network that is interconnected, universally accessible and easy to use, green, and secure will be accelerated. (from Wallstreetcn APP)

[Shanghai Clearing House and CFETS to Launch Optimized Foreign Currency Repo Service from June 22] The Interbank Market Clearing House Co., Ltd. (Shanghai Clearing House) and the China Foreign Exchange Trade System (CFETS) issued a notice stating that to further optimize foreign currency repo trading and clearing services and meet market participants' needs for collateral management and diversified settlement methods, Shanghai Clearing House and CFETS will launch an optimized foreign currency repo service on June 22, 2026. During the term of a foreign currency pledged repo transaction, both parties may initiate substitution of pledged bonds for trades not yet due for settlement through the Shanghai Clearing House integrated business system or the CFETS foreign exchange trading system, subject to counterparty confirmation. Prior to the settlement date, both parties may initiate cash settlement through the Shanghai Clearing House integrated business system, and Shanghai Clearing House will complete the buyout repo maturity settlement based on the cash settlement instruction. The specific launch arrangements by CFETS will be announced separately. (from Wallstreetcn APP)

[PBOC Reverse Repos Net Inject 59.5 Billion Yuan Today] The PBOC conducted 248 billion yuan seven-day reverse repo operations in the open market at an interest rate of 1.40%, unchanged from the previous day. Today, 188.5 billion yuan of reverse repos matured.

US dollar:

As of 11:45, the US dollar index fell 0.15% to 100.24. US Fed officials hinted on Wednesday that they may need to raise interest rates soon rather than cut them, a sharp shift in thinking amid rapidly climbing inflation. Evercore ISI analyst Krishna Guha stated that the pullback in energy prices may offer some relief in the coming months. However, he cautioned that the interest rate outlook has already decoupled from oil prices, which indicates deeper uncertainty over whether underlying inflation will cool enough to spare the US Fed from having to hike rates eventually. Beyond energy, Guha noted, two pressures remain: the ongoing pass-through from tariffs and cost spillovers from the investment boom in AI infrastructure. Claudia Sahm, chief economist at New Century Advisors and former Fed economist, said conditions that would normally prompt the Fed to respond to supply-driven inflation—namely an overheated labour market or unanchored inflation expectations—have yet to be seen. But she acknowledged that the case for action is building. “I can understand the view that the Fed should be ready to step in and hike if things worsen,” she said, adding that the Fed could move more swiftly than during the pandemic-era inflation surge because “they are already having that debate now.”

According to CME FedWatch, the probability of the US Fed holding rates steady through July stands at 64.0% (versus 91.0% before the decision), with a 35.1% chance of a cumulative 25bp hike (versus 8.9%) and a 1% chance of a cumulative 50bp hike (versus 0%). For the year-end, the probability of unchanged rates is 14.2% (versus 38.2%), while the odds of cumulative hikes stand at 25bp (36.4%, versus 43.0%), 50bp (33.8%, versus 16.2%), 75bp (13.5%, versus 2.4%), and 100bp (2.1%, versus 0.1%).

Citi expects the Fed to deliver 25bp rate cuts in October 2026, December 2026, and January 2027, shifting from its previous forecast of cuts in September, October, and December this year.

Goldman Sachs Vice Chairman and former Dallas Fed President Kaplan said the Fed may need to raise rates as early as September if inflation remains persistently elevated. “If the inflation data do not cool between now and September, it would be wise for the Fed to act in September or in the autumn. That would be the more prudent course,” Kaplan said. Markets turned hawkish after Fed Chairman Walsh signalled that the central bank remains focused on fighting inflation. Traders dumped short-term Treasuries, pushing some yields higher. Walsh’s remarks were reinforced by the personal projections of Fed members, half of whom pencilled in rate hikes by the end of 2026. Kaplan stated that if inflation remains stubborn, it indicates that monetary policy is still too loose. He also pointed out, “Fed policy actions are rarely one-offs; rate hikes often come in series of two or three. So I think if you’re going to act in September, you need to be prepared. There may be one or two more.” (Jin10 Data APP)

Data Releases:

Today will see the release of US initial jobless claims for the week ending June 13, the US June Philadelphia Fed manufacturing index, the US May Conference Board leading index month-on-month change, Switzerland’s May trade balance, the Swiss National Bank policy rate as of June 18, the UK ILO unemployment rate for the three months to April, the UK May unemployment rate, the UK May claimant count change, the UK Bank of England rate decision as of June 18, and the eurozone April seasonally adjusted current account, among other data.

Additionally, attention should be paid to: China’s refined oil products will open a new round of price adjustment window. The Fed’s FOMC will release its interest rate decision and summary of economic projections, Fed Chairman Warsh will hold a monetary policy press conference, the Swiss National Bank will announce its rate decision, and the Bank of England will release its rate decision and meeting minutes.

It is worth noting that on June 18, China’s SGE, SHFE, ZCE, and DCE will have no night session trading due to the eve of the Dragon Boat Festival. On June 19, the NYSE will be closed for Juneteenth. CME Group’s precious metals, energy, forex, equity indexes, and US Treasury futures contracts trading will close early at 01:00 Beijing time on June 20 for the Juneteenth holiday, while ICE’s Brent crude oil futures contract trading will close early at 01:30 Beijing time on June 20 for the Juneteenth holiday.

Crude Oil:

As of 11:45, oil prices in both markets fell, with WTI down 1.82% and Brent down 1.48%. Trump signed a memorandum of understanding with Iran at the Palace of Versailles in France on Wednesday, declaring an end to the war and the reopening of the Strait of Hormuz. A US official stated that the agreement had officially taken effect, but it remained unclear whether Iran had immediately taken steps to fully reopen the strait. "Trump's signing of the MOU after the G7 meeting is another important step in the process of reopening the Strait of Hormuz," said Rajeev De Mello, Global Macro Portfolio Manager at Gama Asset Management, "This will further compress energy risk premiums, ease inflation concerns, and provide support for bond and equity markets after the Fed's initial reaction." (Wall Street CN)

An Iranian Foreign Ministry spokesperson stated: Iran must be able to sell its oil smoothly, with no obstacles in transportation and insurance, and must receive the proceeds from oil sales. Jinshi Data APP)

According to the latest data from the U.S. Energy Information Administration (EIA), U.S. EIA crude oil inventories fell by 8.26 million barrels last week, compared with estimates of a 5.2 million barrel decline by Bloomberg users and a 3.6918 million barrel draw by analysts, following a 7.227 million barrel drop the prior week. Inventories at the Cushing hub in Oklahoma have declined for eight consecutive weeks to around 20 million barrels, a level that most traders consider the operational minimum. The Strategic Petroleum Reserve also fell this week to about 340 million barrels, the lowest since 1983. (Wallstreetcn)

Spot market overview:

►

►

►

►

►

►

►

►

►

►

![Decline in arrivals and restocking increase amid lower copper prices drive spot premiums sharply higher [SMM South China Copper Cathode Spot Weekly Review]](https://imgqn.smm.cn/usercenter/LbxVx20251217171714.jpeg)

![End-use demand was sluggish, suppliers cut prices to sell, and overall trading sentiment weakened [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/CaDcj20251217171711.jpg)

![US Fed Releases Hawkish Signals, Most-Traded SHFE Tin Contract Center Slips to Around 412,000 [SMM Tin Midday Commentary]](https://imgqn.smm.cn/usercenter/bYFQn20251217171752.jpg)