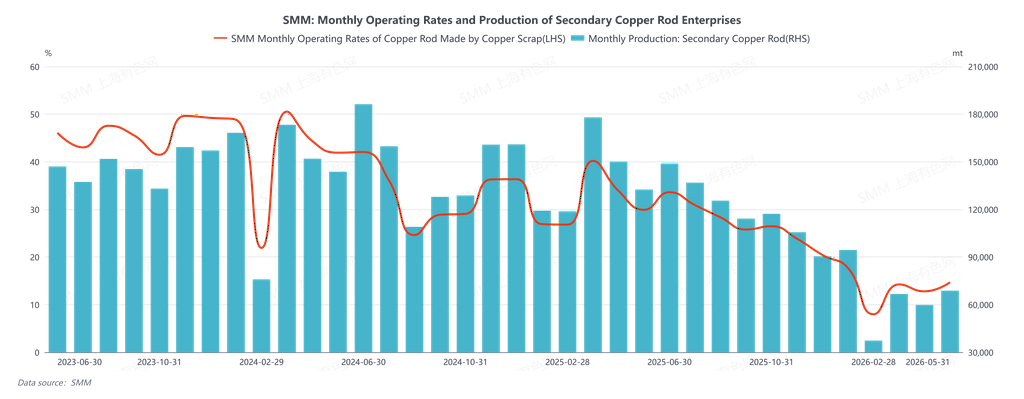

In May 2026, the operating rate of secondary copper rod was 14.7%, higher than expectations of 12.17%, up 1.91 percentage points MoM and down 15.22 percentage points YoY. During May, China's secondary copper rod market as a whole remained caught in a combination of high copper prices, sharp fluctuations, and regulatory compliance pressure. The month was marked not by a one-sided shortage or surplus, but by a more intractable structural stalemate: the industry chain saw supply that existed but moved sluggishly and demand that was present but could not be released in volume. Transactions were mostly triggered by price pace and funding conditions, rather than by spontaneous expansion of end-use demand. From a total volume perspective, based on SMM data, the weekly operating rate throughout the month largely seesawed back and forth within a 6%–11% range (with an intraweek high of 10.89% and a low of 6.76%), remaining significantly lower YoY, indicating that supply capacity was not truly unleashed. On the profit side, gross margins fluctuated along with the widening and narrowing of the price difference between copper cathode rod and secondary copper rod, generally swinging around a few hundred to a thousand yuan within a week—nominally positive but lacking stability. Enterprises prioritized survival and risk control above all else.

The hard constraint on the supply side primarily stems from the "compliance-capital-logistics" triangle of copper scrap. After the holiday, copper prices once surged at the market open, igniting the willingness to sell among raw material suppliers. However, the downstream scrap-consuming sector did not follow suit in procurement, leaving the market in a high-price stalemate where "supply wants to sell, but demand does not take it." Subsequently, copper prices experienced violent swings, and the social inventory of raw materials was not effectively destocked. Instead, due to low operating rates at national rod producers, concentrated delivery destinations, and slow turnaround in unloading and quality inspection, a sense of congestion emerged—"goods stuck in warehouses, payments failing to return." This increased the capital tied up for traders, further weakening their ability to make further purchases. More importantly, regional divergence was amplified by invoicing and payment collection: differences in the operating environment between the north and south led to relatively faster capital turnover in the north, while southern yards were forced to push down prices to offset capital costs. The anomalous structure of "same material, different prices"—with the purchase price of bare bright copper in south China being 400–600 yuan/mt lower than in the north—indicates that the market is not pricing based solely on supply and demand, but on settlement feasibility. Entering the mid-to-late period, after the earlier fluctuations, traders' visible inventory may not necessarily be high, but "available supply" remained tight—because the precondition for releasing volume is the willingness to sell on credit. When credit sales are not dared, even if there is stock in warehouses, the market will still feel a "shortage."

The demand side was more like a "pulse driven by price spreads" rather than steady restocking. Throughout the month, the price difference between copper cathode rod and secondary copper rod repeatedly widened to 1,700–2,500 yuan/mt or even higher. In theory, the economic viability of secondary copper rod appeared repeatedly, but orders from end-users (cable and engineering sectors) did not expand simultaneously. Downstream players were doubtful about high absolute copper prices and the market direction, and their purchases were characterized by rigid demand, buying on dips, and short cycles. Copper rod enterprises themselves saw slower shipments, which in turn constrained raw material procurement, as they were "willing to buy but unwilling/unable to continuously chase higher prices at market levels." By the latter part of the month, a more prominent contradiction emerged: under the background of "reverse invoicing / rectifying the invoicing economy," insufficient input invoices began to shift from a cost issue to a production constraint. Some enterprises, even if they wanted to produce, were stuck in the invoice chain, and their procurement volume was forcibly compressed. There even emerged a structure where "enterprises with rigid demand were forced to raise prices to grab goods to avoid running out of supply, but payment terms were forcibly extended" -- traders, knowing the rising risk of payment recovery, still closed deals under profit and turnover pressure. The market then descended from a "price game" into a capital game of "whoever can withstand the payment terms gets the goods."

Looking at the spread structure, the common feature of both the price difference between primary metal and scrap and the price difference between copper cathode rod and secondary copper rod in May was "wide range but poor stability": spreads were able to widen but often narrowed quickly due to copper price pullbacks or raw material price support (e.g., retreating from the 2,500 yuan/mt level to the 1,000 yuan/mt level), meaning the economic viability window for secondary copper rod was more of a trading opportunity than a sustained demand bonus. At the same time, raw material prices were "stickier" relative to copper cathode—they did not collapse by the same magnitude on the way down, which conversely also indicates that the cost floor was not solely provided by supply-demand dynamics, with part of it being "locked in" by compliance and capital costs.

Overall, the core issue in the secondary copper rod market in May was not whether there was a shortage of copper, but rather “whether there is a shortage of settleable, compliant supply, and whether a stable closed-loop payment collection can be formed.” As long as invoices and payment cycles remain hard constraints, the operating rate will struggle to trend upward, and transaction activity will continue to exhibit a pulse-like pattern of “when copper prices surge, raw material circulation expands; when copper prices fall, holders hold back from selling and circulation contracts.” Even if the price difference between copper cathode rod and secondary copper rod looks attractive at times, it is more easily consumed by account period risks and end-user order ceilings.

Looking ahead to June, for the market to break out of this “high volatility—low throughput” state, the key lies not in how high copper prices can reach, but in whether there can be marginal improvements: the easing of enforceable invoice criteria across regions and the unblocking of payment collection chains (otherwise, the discount structure in south China will be hard to eliminate, and social inventory will remain “nominally plentiful but effectively tight”). Otherwise, the secondary copper rod segment is highly likely to continue walking a tightrope within the triangle of “need to produce—invoicing bottlenecks—control of account periods,” where high prices mean no shortage of material, falling prices mean material disappears first, and transactions rely on volatility rather than demand.