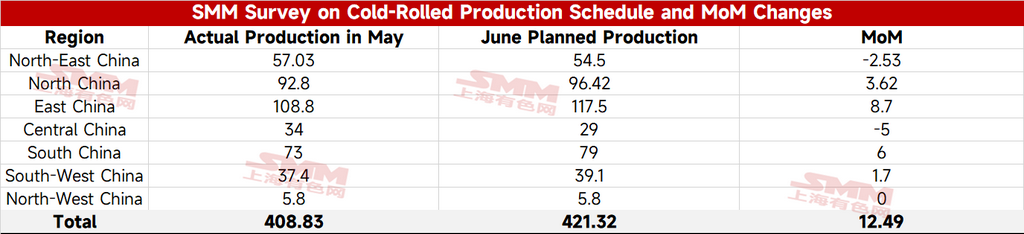

- SMM Cold Rolling Production Schedule: June Steel Mill CR Schedule Up 3%, Daily Average Schedule Up 7%

According to the latest SMM tracking, the planned total volume of commercial CR products from 31 mainstream CR sheet mills this month stands at 4.2132 million mt, up 124,900 mt or 3.1% from last month's actual outpu

On a daily basis, June has one fewer day than May, with the average daily CR commercial products schedule for June reaching 140,400 mt, up 6.5% MoM from last month's actual daily average output.

- SMM HRC Production Schedule: June HRC Production Schedule Down 0.5% MoM, Daily Average Up 3%

According to the latest SMM tracking, the planned commercial HRC volume of 39 mainstream steel mills this month totals 13.2679 million mt, down 69,000 mt or 0.5% from the actual commercial HRC production last month.

On a daily average basis, as June has one day less than May, the daily average commercial HRC production schedule stands at 442,300 mt, up 2.8% MoM from the actual daily average production of May.

In June, as some steel mills that underwent earlier maintenance gradually resumed production, coupled with HRC profit margins being relatively better than those of rebar in most regions, the total HRC production schedule volume saw relatively small fluctuations MoM compared with the actual level in May. As June has fewer days than May, on a daily average basis, the HRC production schedule increased MoM.

Summary: Total hot-rolled commercial material production schedules at steel mills in June were basically flat MoM. As June has fewer days than May, the daily average production schedule edged up MoM. Demand side, with the arrival of the off-season for steel consumption, end-use demand is expected to gradually weaken in June, and HRC inventory may see an inventory buildup inflection point in late June.

Other aspects, short-term ferrous metals ore, coke, and steel price trends have diverged. As steel's own demand is under pressure, its price initiative is weak. Monitor whether there are new drivers from the raw material coal and coke side to cause finished steel prices to follow in fluctuating. HRC prices are expected to move sideways within a range in June, with limited upside and downside room.

![[SMM HRC Daily Trading Volume] Spot HRC trading improved slightly](https://imgqn.smm.cn/usercenter/vhvTQ20251217171715.jpg)

![[SMM Sheets & Plates Daily Review] Near-Term Sheets & Plates May Fluctuate Weakly](https://imgqn.smm.cn/usercenter/JdqON20251217171718.png)