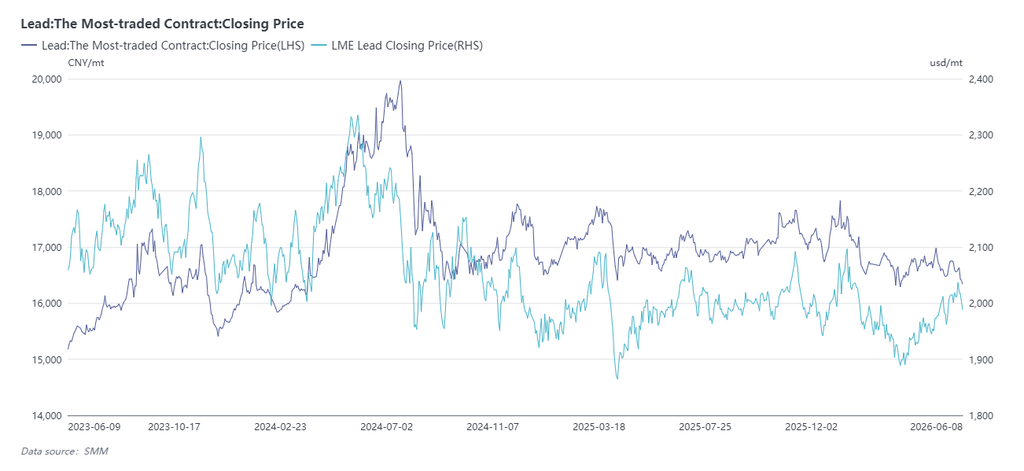

SMM June 9 News: As of the close at 11:30 a.m. today, the main SHFE lead contract 2607 was reported at 16,070 yuan/mt, down 305 yuan/mt, a decline of 1.86%, hitting an intraday low of 16,055 yuan/mt, the lowest since March 8, 2024. Meanwhile, the SHFE lead 2607 contract saw a single-day open interest increase of 18,783 lots, with total open interest reaching 83,834 lots. This downward trend accompanied by rising open interest has focused market attention on the 16,000 yuan/mt "lifeline."

Aside from the weak macroeconomic backdrop, the biggest bearish factor from a fundamental perspective is the mismatch between the concentrated resumption of production at secondary lead smelters and the off-season consumption period. Going forward, the lead price trend requires close attention to the following key points:

1. Will the falling lead prices force secondary lead smelters to cut production again?

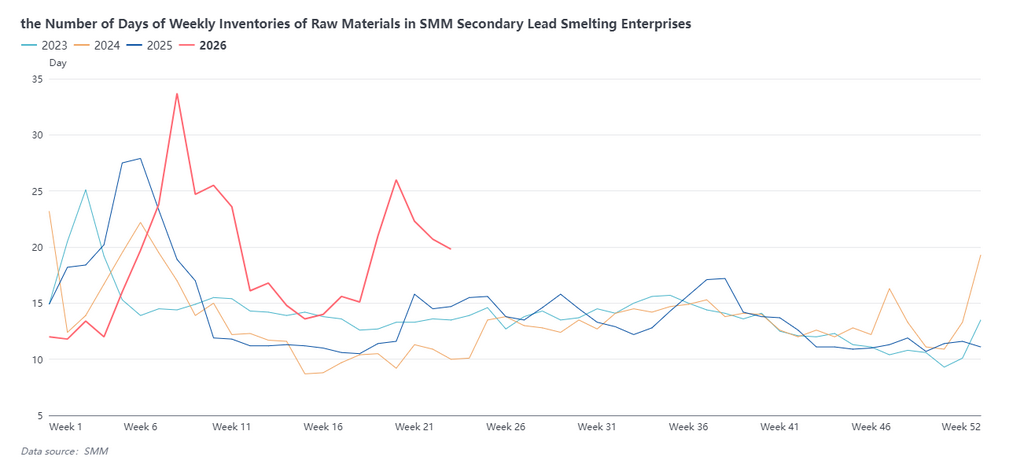

It is understood that since mid-to-late May, secondary lead smelters in East China and other regions have gradually resumed production after maintenance. The latest data shows that as of June 4, SMM's weekly operating rate for secondary lead stood at 28.4%, rising for four consecutive weeks. As secondary lead smelters ramped up production, demand for raw materials such as scrap batteries also expanded, and raw material inventories at secondary lead smelters have likewise declined for four consecutive weeks. Meanwhile, with lead prices falling repeatedly recently, scrap battery prices have limited room to follow the decline due to tight supply, further widening losses for secondary lead smelters. At present, losses at secondary lead smelters have reached 500–700 yuan/mt. Market participants need to monitor production trends at secondary lead smelters and their impact on lead prices going forward.

2. The lead-acid battery market off-season and downstream purchasing expectations at lower prices

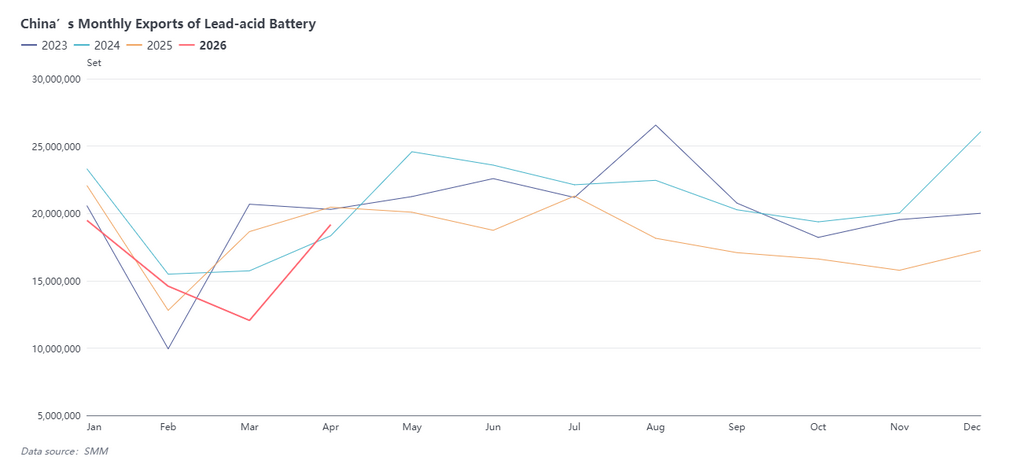

By traditional convention, the second quarter of each year is the traditional consumption off-season for the lead-acid battery market. Lead-acid battery companies are generally in a state of production cuts, with large enterprises unable to achieve full production, and small-to-medium sized enterprises operating at 50–70% capacity. As of June 4, SMM's weekly operating rate for lead-acid batteries was 65.69%, down 1.18 percentage points from the previous week. In addition, the internal-to-external lead price is unfavorable for lead-acid battery exports. Issues such as overseas geopolitical tensions and shipping disruptions have weakened battery exports compared to the same period last year. According to data, China's cumulative exports of lead-acid batteries from January to April 2026 fell by 12.01% year-on-year.

Today, the average price of SMM 1# lead was reported at 16,000 yuan/mt, the lowest since March 11, 2024. The weakening lead price has led to some downstream companies showing interest in purchasing at lower levels. However, due to the large and rapid decline in lead prices, market risk aversion is high, and the vast majority of downstream companies are adopting a wait-and-see attitude. The easing of downstream risk aversion and the realization of buying-at-lows expectations could serve as signals for lead prices to stop falling.

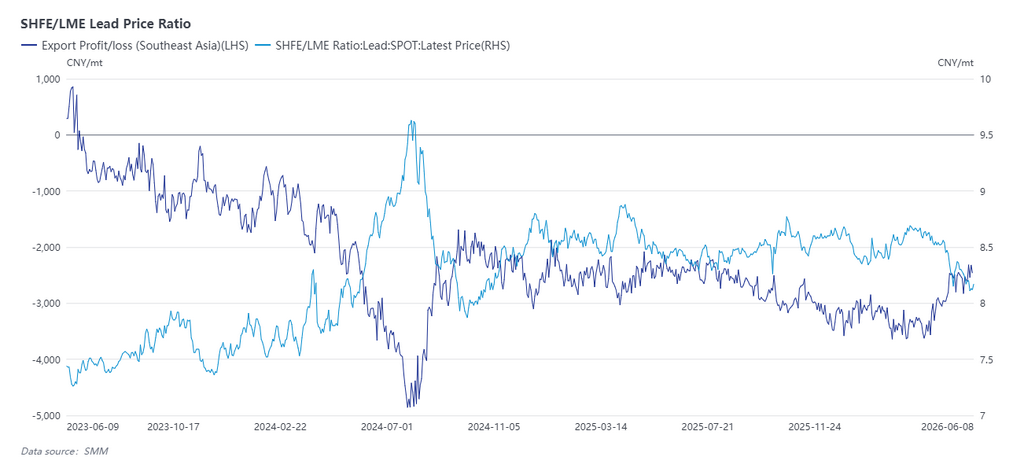

3. Expectations for the shift from a lead ingot import window to an export window in H2

Since the beginning of this year, China's lead ingot import window has been open for a relatively long period, with a large volume of overseas lead ingots flooding into the Chinese market. According to data, China's total imports of lead ingots (including refined lead, crude lead, etc.) from January to April reached 188,100 mt, a surge of 299% year-on-year. Until the second quarter, overseas markets saw phased reductions in lead ingot supply due to shipping disruptions, environmental inspections, and insufficient scrap battery supply. Meanwhile, overseas lead demand, particularly from Southeast Asian markets, has been on the rise, with a widening supply gap for high-quality lead ingots. Spot premiums in Southeast Asia have been rising continuously. China's lead ingot import window closed in May and has since moved toward narrowing export losses. Given the significant supply gap for high-quality lead ingots in Southeast Asia and the limited electrolytic lead smelting capacity overseas, it is difficult to rely solely on non-Chinese lead ingot supply to meet the rapidly growing lead consumption. Expectations for China's lead ingot exports are rising, which will become a key factor in destocking China's lead ingot market in H2 this year.

In the short term, SHFE lead is experiencing concentrated open interest growth alongside a downward trend, with strong market risk aversion. The stability of the 16,000 yuan/mt level carries uncertain risks. For the time being, the foreseeable and quickly realizable signals for a price halt will require close attention to downstream purchasing-at-lows and production trends at secondary lead smelters. Once stop-falling signals emerge, lead prices could stabilize and rebound. Otherwise, the downtrend is likely to persist, and attention should turn to the next lead ingot export window.

![Supply Increase and Off-Season Demand Weigh on Lead Prices, Cost Support Limits Downside Room [Lead Futures Brief Review]](https://imgqn.smm.cn/usercenter/XMxKT20251217171720.jpeg)