Dữ liệu: Biến động thị trường SHFE, DCE (ngày 8 tháng 6)

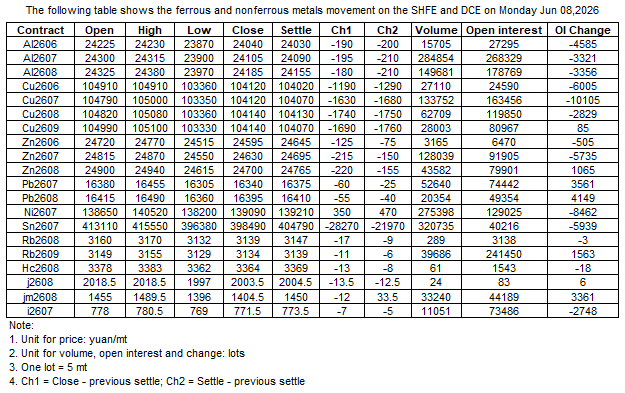

Bảng dưới đây cho thấy diễn biến của kim loại đen và kim loại màu trên SHFE và DCE vào ngày 08 tháng 6 năm 2026

Tuyên bố về Nguồn Dữ liệu: Ngoại trừ thông tin công khai, tất cả dữ liệu khác được SMM xử lý dựa trên thông tin công khai, giao tiếp thị trường và dựa trên mô hình cơ sở dữ liệu nội bộ của SMM. Chúng chỉ mang tính chất tham khảo và không cấu thành khuyến nghị ra quyết định.

Để biết thêm thông tin hoặc có thắc mắc gì, vui lòng liên hệ: lemonzhao@smm.cn

Để biết thêm thông tin về cách truy cập báo cáo nghiên cứu, vui lòng liên hệ:service.en@smm.cn

Tin Liên Quan

![[Southern Taiwan steel mills turn to direct negotiations to revive rebar sales]](https://imgqn.smm.cn/usercenter/crVox20251217171717.jpg)

1 phút trước

[Southern Taiwan steel mills turn to direct negotiations to revive rebar sales]

Đọc thêm

[Southern Taiwan steel mills turn to direct negotiations to revive rebar sales]

Rebar producers in southern Taiwan have stopped issuing official price quotes this week, shifting to flexible individual negotiations to attract buyers. Distributors have lowered retail rates in response to the sluggish market. The trading pause threatens to extend market stagnation to a ninth consecutive week without significant deals. Mills face severe order shortages and rising inventory backlogs from delayed shipments, leaving producers open to any offer without a fixed baseline. Despite this, distributor interest remains minimal. After two months of inventory reduction, most smaller traders are depleted, leaving only large-scale distributors still operational.

1 phút trước

![[AISI: US raw steel production in week ending July 4 rises w-o-w, y-o-y]](https://imgqn.smm.cn/usercenter/FGavQ20251217171717.jpg)

1 phút trước

[AISI: US raw steel production in week ending July 4 rises w-o-w, y-o-y]

Đọc thêm

[AISI: US raw steel production in week ending July 4 rises w-o-w, y-o-y]

US raw steel output reached 1.856 million net tons (approx 1.684 million tonnes) for the week ending July 4, 2026, at an 80.4% capability utilization rate. This represented a 4.3% increase from 1.780 million net tons (78.9%) in the same period last year, and a 0.8% increase from the previous week's 1.842 million net tons (79.8%). Year-to-date production through July 4 totaled 48.112 million net tons (approx 43.65 million tonnes) at 78.8% utilization, up 6.0% from 45.400 million net tons (76.8%) in the same period last year.

1 phút trước

![[SMM Steel] Domestic Mills Slashing Prices Fails to Stimulate Buying; Wait-and-See Stance Dominates Vietnam HRC Market](https://imgqn.smm.cn/usercenter/mpffV20251217171715.jpg)

4 phút trước

[SMM Steel] Domestic Mills Slashing Prices Fails to Stimulate Buying; Wait-and-See Stance Dominates Vietnam HRC Market

Đọc thêm

[SMM Steel] Domestic Mills Slashing Prices Fails to Stimulate Buying; Wait-and-See Stance Dominates Vietnam HRC Market

[Vietnam] ASEAN hot-rolled coil (HRC) import offers ticked down to 535 USD/tonne CFR this week, with overall regional trading activity remaining deeply subdued in the thick of the seasonal doldrums. Facing an intersection of weak end-user demand and competitive import alternatives, local producers in Vietnam have been forced to lower their quotes to stimulate sales. However, as the substantial price reductions by the two major domestic mills last week were widely anticipated and import offers from international traders continue to hold a price advantage, local buyers showed little urgency to restock and largely maintain a strict wait-and-see stance. Notably, only isolated Indian HRC deals were reported closed at 525 USD/tonne CFR recently. Overall, given the reality of high regional inventory levels and sluggish downstream consumption, flat steel prices in Vietnam and neighboring nations will continue to face near-term headwinds.

4 phút trước

Tin Liên Quan

[Southern Taiwan steel mills turn to direct negotiations to revive rebar sales]

Jul 07, 2026 16:47

[AISI: US raw steel production in week ending July 4 rises w-o-w, y-o-y]

Jul 07, 2026 16:47

[SMM Steel] Domestic Mills Slashing Prices Fails to Stimulate Buying; Wait-and-See Stance Dominates Vietnam HRC Market

Jul 07, 2026 16:43

[Nhật Bản dự kiến áp thuế chống bán phá giá tạm thời đối với thép không gỉ cán nguội từ Trung Quốc và Đài Loan]

Jul 07, 2026 16:36