SMM June 5 News:

Metals market,

as of the midday close, domestic base metals all declined. SHFE copper, aluminum, and lead each fell within 0.5%. SHFE zinc fell 0.88%, SHFE tin fell 4.29%, and SHFE nickel fell 1.68%.

Additionally, the most-traded casting aluminum futures contract edged down, alumina most-traded contract fell 0.75%, lithium carbonate most-traded contract rose 1.37%, silicon metal most-traded contract fell 1.15%, and polysilicon most-traded futures contract fell 1.76%.

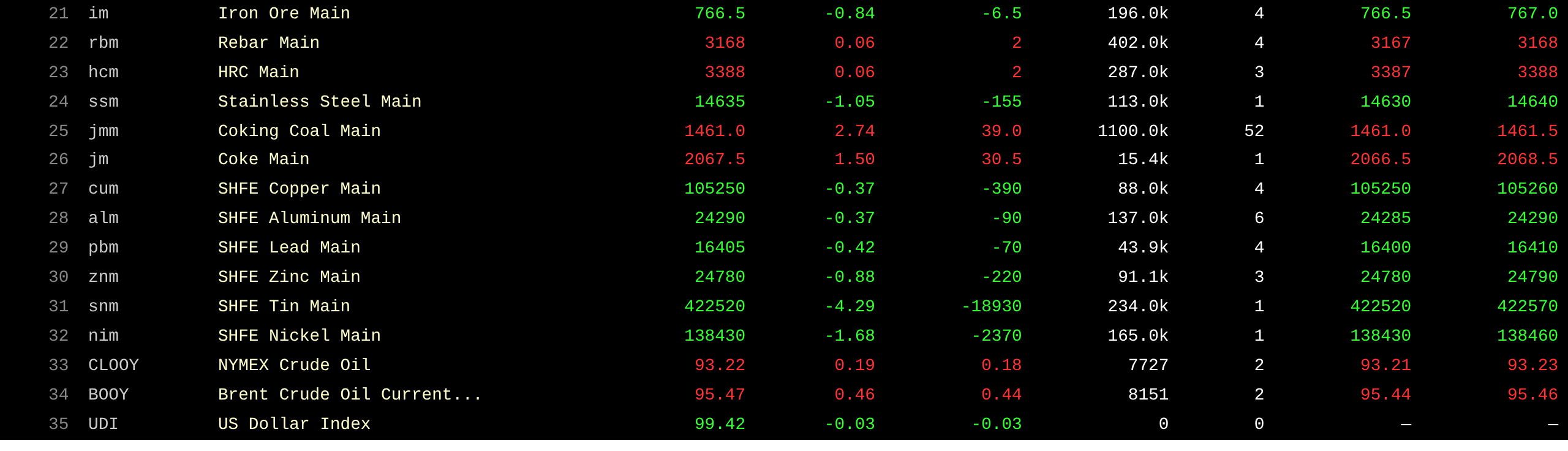

Ferrous metals mostly rose, with iron ore falling 0.84%, rebar and HRC both edging up 0.06%, and stainless steel falling 1.05%. Coking coal and coke: the most-traded coking coal contract rose 2.74%, and the most-traded coke contract rose 1.5%.

Overseas base metals market, as of 11:39, LME metals fell across the board. LME copper fell 1.05%, LME aluminum fell 0.98%, LME lead fell 0.4%, LME zinc fell 0.99%, LME tin fell 2.05%, and LME nickel fell 0.21%.

Precious metals, as of 11:39, COMEX gold fell 0.9% and COMEX silver fell 1.77%. Domestic precious metals: the most-traded SHFE gold contract fell 0.53%, and the most-traded SHFE silver contract fell 1.75%.

Additionally, as of the midday close, the most-traded platinum futures contract fell 0.02%, and the most-traded palladium futures contract fell 2.4%.

As of the midday close, the most-traded European container freight futures contract fell 0.68% to 3,660 points.

As of 11:39 on June 5, selected futures midday quotes:

Spot and fundamentals

Copper: Today, Guangdong #1 copper cathode spot prices against the front-month contract: high-quality copper quoted at a premium of 50 yuan/mt, up 20 yuan/mt from the previous trading day; standard-quality copper quoted at a discount of 20 yuan/mt, up 10 yuan/mt; SX-EW copper quoted at a discount of 70 yuan/mt, up 10 yuan/mt. The average price of Guangdong #1 copper cathode was 105,335 yuan/mt, down 65 yuan/mt from the previous trading day, while the average for SX-EW copper was 105,250 yuan/mt, down 70 yuan/mt. Spot market: Guangdong inventory continued to decline today, marking four consecutive days of decline...

Macro front

Domestic side:

[Strengthening fair competition: China Anti-Monopoly Enforcement Annual Report (2025) released] The State Administration for Market Regulation (the National Anti-Monopoly Bureau) released the China Anti-Monopoly Enforcement Annual Report (2025). The report noted that in 2025, the SAMR continued to step up anti-monopoly enforcement, filing 20 monopoly cases and concluding 22 throughout the year, with total fines and confiscations reaching 653 million yuan; steadily improved the quality and efficiency of business concentration regulation, concluding 706 merger cases, up 9.8% YoY; intensified efforts to remove local protectionism and market segmentation, issued the Implementation Measures for the Fair Competition Review Regulations, strengthened gatekeeping at the source for fair competition review, and market regulation departments at all levels reviewed nearly 60,000 policy measures during the year. (CCTV)

[PBOC Reverse Repo Injects Net 92 Billion Yuan Today] The PBOC conducted a 215 billion yuan 7-day reverse repo operation at an interest rate of 1.4%, unchanged from the previous operation. Today, 123 billion yuan in reverse repos matured.

On the dollar front:

As of 11:39, the US dollar index edged down 0.03% to 99.42. US initial jobless claims for the week ending May 30 came in at 225,000, above the expected 213,000 and the revised prior reading of 212,000, the highest since the first week of February. The four-week moving average was 214,750, up from 208,250 the previous week. Continuing claims stood at 1.777 million, slightly below the expected 1.78 million. The rise in initial claims indicates some softening in the labor market, though they remain at relatively low and stable levels. Continuing claims edged down. It should be noted that continuing claims data are reported with a one-week lag, so next week's data will correspond to this week's initial claims. (Jin10 Data APP)

According to the CME FedWatch Tool: The probability that the Fed will keep interest rates unchanged through June is 96.4%, while the probability of a cumulative 25-basis-point cut is 3.6%. Through July, the probability of rates staying unchanged is 88.5%, the probability of a cumulative 25-bp rate hike is 8.2%, and the probability of a cumulative 25-bp cut is 3.2%.

The Fed's Mary Daly said that monetary policy is currently in a good place, but the economic situation is too uncertain to clearly determine the path of interest rates. Daly stated that providing forward guidance is not appropriate at this time because it is impossible to predict how the economy will evolve, and the most concerning issue is inflation, with the focus on rising energy and food prices. Bringing inflation back to target is the Fed's top priority. Daly also said that while there is no clear evidence in the economic data yet that AI is boosting productivity, she remains optimistic about the technology and believes 2027 will be a litmus test; at the same time, she sees no financial stability concerns related to AI investment. (Jin10 Data APP)

Data:

Today, data including the US unemployment rate for May, US seasonally adjusted non-farm payrolls for May, US average hourly earnings year-over-year for May, US average hourly earnings month-over-month for May, UK Halifax seasonally adjusted house price index month-over-month for May, French industrial production month-over-month for April, French trade balance for April, Eurozone Q1 revised GDP annual growth rate, and Eurozone Q1 final seasonally adjusted employment change quarter-over-quarter will be released.

Additionally, 2028 FOMC voting member and Kansas City Fed President Schmid participated in a fireside chat, while 2027 FOMC voting member and San Francisco Fed President Daly delivered a speech.

Crude Oil:

As of 11:39, oil prices on both exchanges moved sideways, with WTI up 0.19% and Brent up 0.46%. The market focused on developments in the geopolitical conflict.

UK-based maritime analytics firm Windward reported on the 4th that satellite imagery showed loading operations had resumed at Iran’s key oil export hub, Kharg Island. The report stated that satellite images captured on June 2 showed a very large crude carrier (VLCC) moored near the western offshore terminal of Kharg Island, marking the first confirmed vessel to berth since the facility halted operations in early May due to a suspected oil leak. On June 3, loading operations were underway simultaneously for the VLCC at the western berth and a Panamax tanker at the eastern T-jetty. By the 4th, the VLCC had completed loading and departed, while the Panamax remained berthed at the terminal. Windward noted that the simultaneous resumption of services at both terminals indicates Iran is actively working to restore crude export capacity. The report also highlighted continued frequent activity by small fast-attack craft of Iran’s Islamic Revolutionary Guard Corps (IRGC) throughout the Strait of Hormuz. The ongoing high tempo of operations suggests that the IRGC Navy remains on heightened alert to support Iran-linked vessels in the Strait. (Xinhua News Agency)

On Friday, an explosion occurred near the Mina Al Fahal crude terminal in Oman. Details on the cause and scale remain limited, but the incident was reportedly a drone attack. The spillover of geopolitical risks has drawn close attention from multiple parties. (Jin10 Data App)

Furthermore, eight OPEC+ member countries will hold an online meeting on Sunday to review supply policy for March. According to delegates, OPEC+ is still prepared to approve the suspension of production increases, even after US threats against member Iran helped push oil prices to $70. A delegate previously suggested that a major supply disruption could prompt the group to act, but for now, their stance appeared unaffected by this week’s crude price rally. OPEC+ faces a more uncertain choice at its subsequent monthly meeting, which will likely be held in early March, when it must decide on a course of action after the Q1 production-increase pause expires. Other members like Saudi Arabia and the UAE have already shown notable signs of eagerness to continue restoring output. However, whether further increases are feasible is another question. (Jin10 Data App)

Spot Market Overview:

►

►

►

►

►

►

►

►

►

►

![Delivery Logic Underpins, Shanghai Spot Copper Premiums Narrow Slightly [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/fEiiq20251217171711.jpg)

![Market Buying Sentiment Recovers, Premiums Rise [SMM Spot Aluminum Midday Review]](https://imgqn.smm.cn/usercenter/kxYyQ20251217171651.jpg)

![Downstream Procurement Increased, Suppliers Held Prices Firm to Sell [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/mPNrH20251217171709.jpg)