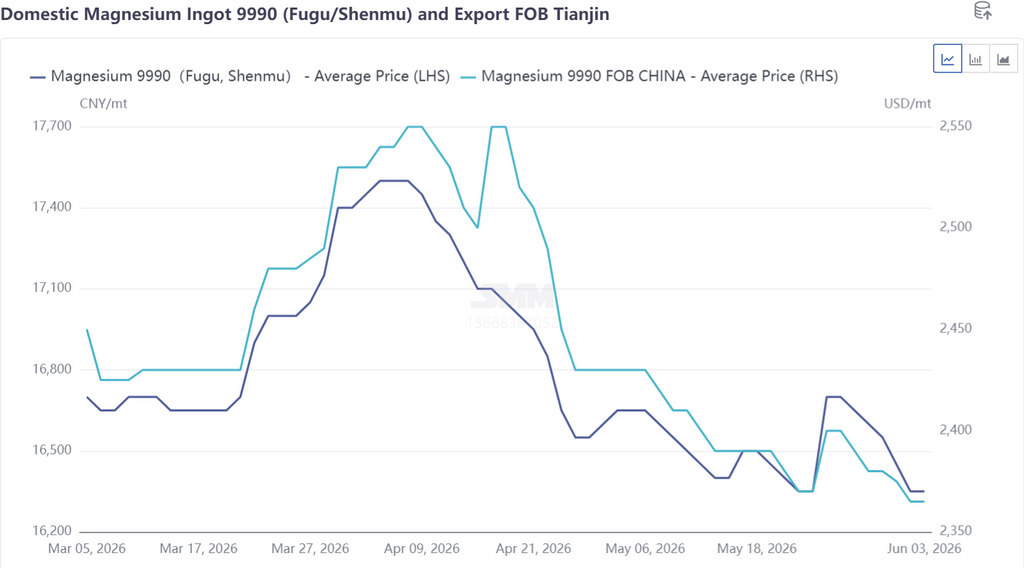

Vào tháng 5/2026, giá magiê đi ngang trong biên độ 16.300-16.700 NDT/tấn, giá trung bình tháng đạt 16.516 NDT/tấn, giảm 3,21% so với tháng trước. Biên độ biến động giá tiếp tục thu hẹp trong tháng 5, thị trường rơi vào thế tiến thoái lưỡng nan giữa tăng và giảm, xu hướng được dẫn dắt bởi hai yếu tố cốt lõi: cung cầu cơ bản và hỗ trợ chi phí. Cung cầu duy trì cân bằng động. Nhờ tình hình sản xuất và tiêu thụ bán cốc cải thiện, các nhà luyện magiê nguyên sinh giảm bớt áp lực vốn ở biên, ý muốn bán giá thấp để thu hồi vốn nguyên liệu suy yếu, hỗ trợ giá chào giao ngay. Sự phân hóa cơ cấu tồn kho trở nên nổi bật: trong giai đoạn giá tăng, các nhà luyện kim lớn giảm tồn kho thành công, trong khi các doanh nghiệp nhỏ và vừa tích lũy tồn kho bị động; trong giai đoạn điều chỉnh, các nhà máy quy mô trung bình giao hàng bằng cách giảm giá để chốt đơn, trong khi các nhà máy lớn linh hoạt điều chỉnh giá chào theo hợp đồng tương lai, sự lên xuống của tồn kho duy trì cân bằng cung cầu thị trường. Về phía chi phí, hỗ trợ đáy hiệu quả được hình thành khi giá giao ngay tiếp cận đường chi phí luyện kim, hạn chế tâm lý bi quan của thị trường và tiếp tục nén không gian giảm giá thỏi magiê, cuối cùng kiềm chế đà giảm mạnh và dẫn đến xu hướng đi ngang suốt tháng.

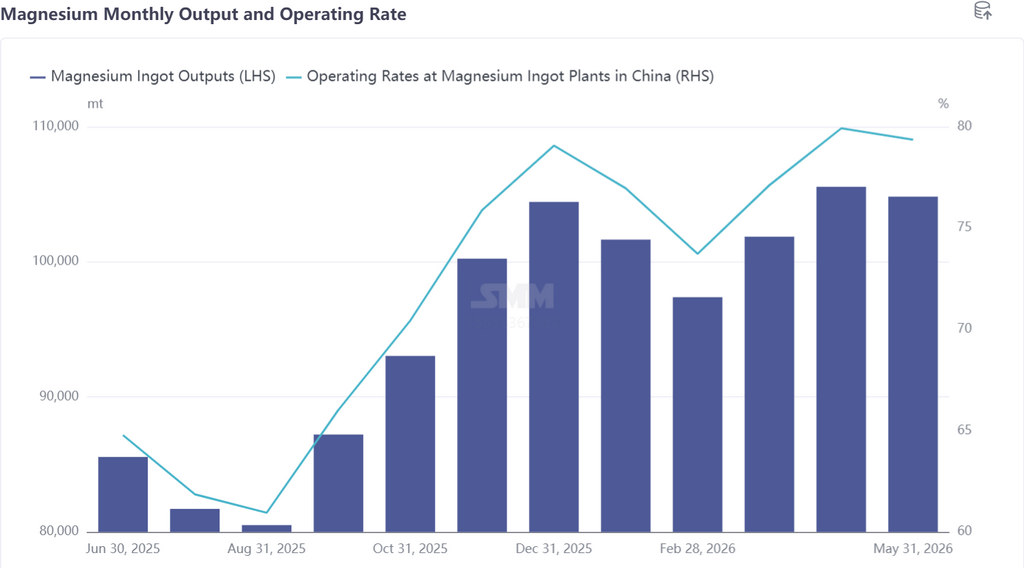

Trong tháng 5/2026, sản lượng magiê nguyên sinh giảm 0,69% so với tháng trước. Sản lượng giữa các vùng phân hóa trong tháng 5, việc bảo trì tập trung tại một số nhà luyện kim ở các khu vực sản xuất chính kéo giảm tổng sản lượng, trong khi các doanh nghiệp tại Tân Cương và An Huy tăng sản lượng, thu hẹp mức giảm ở một mức độ nhất định. Cụ thể, hầu hết các nhà luyện magiê nguyên sinh duy trì sản xuất ổn định trong tháng 4. Một nhà luyện kim tại Thiểm Tây ngừng hoạt động để bảo trì vào đầu tháng 5, trong khi một doanh nghiệp Thiểm Tây khác tăng nhẹ sản lượng hàng ngày. Một doanh nghiệp Sơn Tây tiến hành bảo trì định kỳ cuối tháng, giảm sản lượng khoảng 100 tấn, trong khi một nhà sản xuất Sơn Tây khác tăng nhẹ sản lượng. Mỗi doanh nghiệp tại Hắc Long Giang, An Huy và Tân Cương đều tăng nhẹ sản lượng, trong khi một nhà luyện kim khác tại Tân Cương ngừng sản xuất cả tháng. Nhìn chung, mức giảm sản lượng trên thị trường vượt mức tăng, tổng sản lượng magiê nguyên sinh tháng 5 giảm nhẹ.

Nhìn về tháng 6, giá magiê dự kiến duy trì cân bằng yếu được hỗ trợ bởi chi phí sản xuất. Theo lịch sử, nhu cầu xuất khẩu tháng 6 có xu hướng suy giảm, có thể phá vỡ cân bằng giá hiện tại và tạo thêm áp lực giảm giá magiê. Chịu ảnh hưởng từ tình hình thị trường, một số nhà luyện kim dự kiến sắp xếp bảo trì vào cuối tháng 6; tuy nhiên, công suất mới tiếp tục đi vào hoạt động, kết hợp với việc khôi phục sản xuất từ các cơ sở bảo trì trong tháng 5, sản lượng thỏi magiê tháng 6 dự kiến cơ bản đi ngang so với tháng trước.

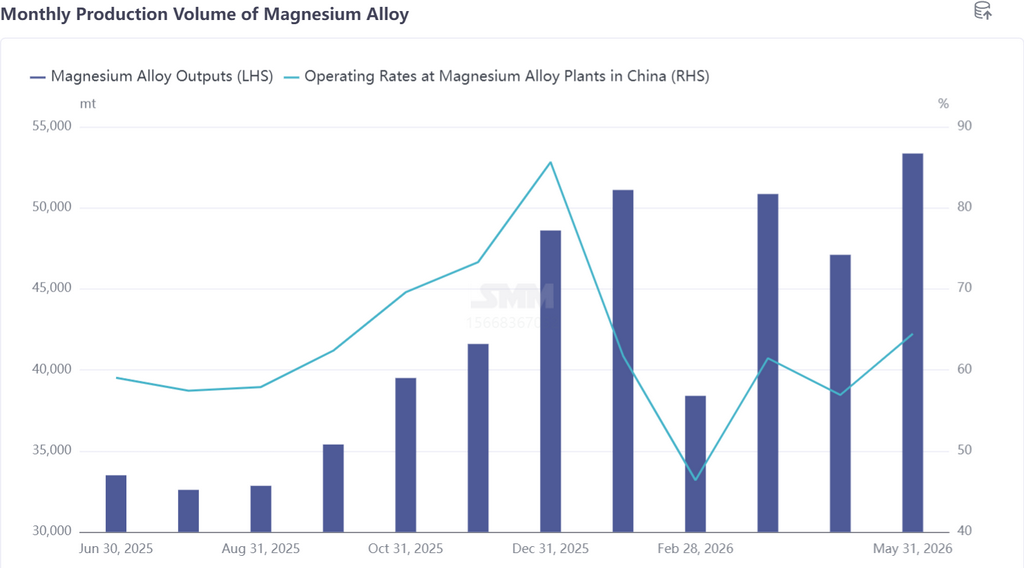

Vào tháng 5/2026, sản lượng hợp kim magiê của Trung Quốc tăng 13,27% so với tháng trước, do nhiều nhà sản xuất hợp kim magiê lần lượt đẩy mạnh sản xuất trong tháng, thúc đẩy sản lượng tăng nhanh. Theo khu vực sản xuất, An Huy, Thiểm Tây và Sơn Tây dẫn đầu về mức tăng sản lượng, trong đó một nhà sản xuất magiê nguyên sinh tại Thiểm Tây đã vận hành thành công dây chuyền sản xuất hợp kim magiê mới. Nhìn về tháng 6, đơn hàng hợp kim magiê cho ô tô đang cải thiện ổn định, trong khi đơn hàng xe hai bánh vẫn trì trệ. Nhu cầu hạ nguồn nhìn chung tăng đều, hỗ trợ sản lượng hợp kim magiê tiếp tục tăng trưởng.

Trong tháng 6, cục diện cung mạnh cầu yếu trên thị trường magiê khó có thể cải thiện. Mười ngày đầu tháng, giá magiê tạm thời tiếp tục xu hướng dao động trì trệ của tháng 5. Bị kéo xuống bởi ngoại thương suy yếu, mức giá sàn dần dịch chuyển thấp hơn và thị trường nhìn chung rơi vào xu hướng giảm dao động. Bước vào cuối tháng 6, giá magiê tiếp tục giảm, liên tục thu hẹp biên lợi nhuận của các nhà luyện kim. Lợi nhuận sản xuất của ngành dần tiến sát ngưỡng hòa vốn, áp lực sản xuất và vận hành tại hầu hết các nhà máy luyện kim tăng đáng kể. Trong bối cảnh này, kỳ vọng bảo trì

tiếp tục gia tăng, và các kế hoạch dừng sản xuất để tránh rủi ro cùng cắt giảm sản lượng để hỗ trợ giá có khả năng hiện thực hóa một cách tập trung. Về phía cung, kỳ vọng thu hẹp nguồn cung gia tăng có thể giảm bớt hiệu quả áp lực cung mạnh cầu yếu hiện tại trên thị trường, tạo hỗ trợ đáy theo giai đoạn cho giá magiê liên tục suy yếu và hạn chế dư địa giảm thêm. Về dài hạn, hoạt động nghiên cứu phát triển và thương mại hóa các loại hợp kim magiê đa dạng tiếp tục khai thác tiềm năng nhu cầu hạ nguồn. Ngành sẽ bước vào giai đoạn mở rộng đồng thời cả cung và cầu, và cục diện dư cung hiện tại có thể được đảo ngược trong tương lai.