SMM, June 2:

According to SMM data, China's refined zinc production in May 2026 was down 0.41% MoM and up over 5.8% YoY. Cumulative smelter production from January to May was up nearly 5.8% YoY, higher than expectations. Entering May, domestic smelters saw production increases exceeding expectations. Apart from routine maintenance at smelters in Guangxi, Shaanxi, and Yunnan, unplanned maintenance at smelters in Henan, Hunan, and Yunnan also contributed some output reductions. Meanwhile, maintenance recovery and production ramps at smelters in Inner Mongolia, Gansu, Xinjiang, Sichuan, Yunnan, and Hubei contributed the main output increases. SMM estimates that China's refined zinc production in June 2026 is expected to be down nearly 1.5% MoM and up over 2% YoY. Cumulative smelter production from January to June is expected to reach 3.881 million mt, up 4.36% YoY cumulatively. The decline in smelter production in June is mainly attributable to maintenance at smelters in Hunan, Inner Mongolia, Guangxi, Gansu, Henan, and Liaoning, while output increases are mainly concentrated in maintenance recovery and production ramps at smelters in Xinjiang, Henan, Gansu, Shaanxi, and Guangxi.

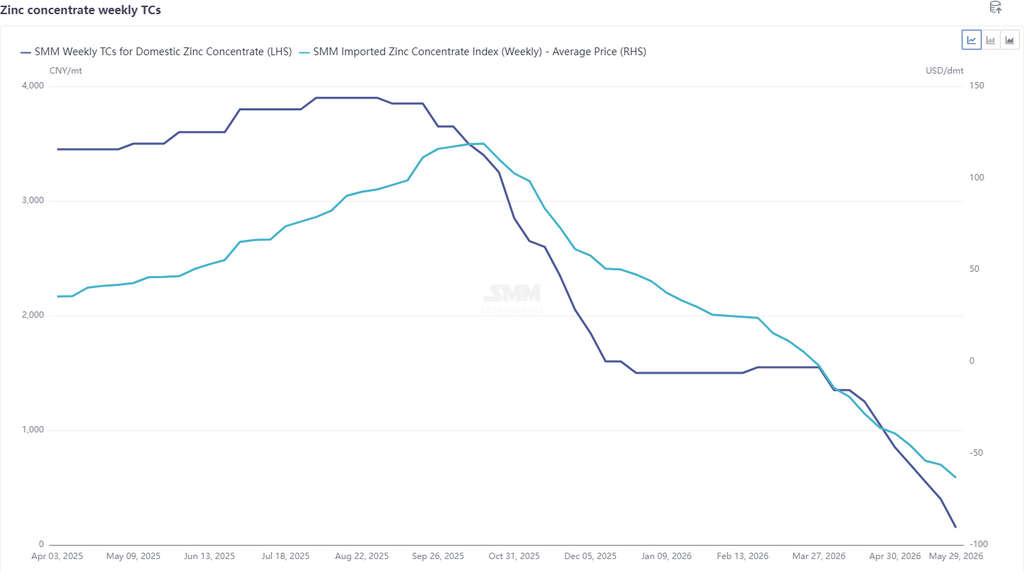

Overall, due to high sulphuric acid and minor metal prices providing certain returns, some smelters postponed maintenance, and May smelter production exceeded expectations. June zinc smelting production continued to be revised down, but the magnitude of reductions was mostly due to routine maintenance adjustments. In terms of current TCs, recent TCs accelerated their decline, with imported TCs falling again to $63.44/dmt, and domestic weekly TCs dropping to a historical low of 150 yuan/mt (metal content). Under low TCs, smelters basically relied on sulphuric acid and by-product profits for support, and some enterprises with low comprehensive recovery rates were already incurring losses. Meanwhile, under low TCs, smelters mostly purchased high-grade ore as raw materials, and days of raw material inventories declined again. Combined with Middle Eastern ore transportation not yet fully restored and Cuban mine supply also being constrained, raw material pressure on smelters increased again.

Looking ahead, from a profitability perspective, high sulphuric acid and minor metal prices provided support, but smelters' comprehensive revenue margins remained thin. However, as south China gradually enters the rainy season, electricity prices are expected to decline, reducing enterprise production costs to some extent. Smelter production is expected to stay high in the short term, but correspondingly, demand for ore will increase. Against the backdrop of low days of raw material inventories, expectations for TC cuts are rising, directly squeezing smelter profits. Comprehensive revenue will turn to losses, and if losses persist, the probability of smelter maintenance and production cuts will increase.