The global steel industry is entering a much harsher environment than the one that fueled its expansion over the past two decades. Global crude steel output has remained broadly stagnant at around 1.83-1.84 billion tonnes, yet competition continues intensifying as weak demand, oversupply, trade barriers and decarbonization costs squeeze margins across the industry. For many steelmakers, producing more steel no longer guarantees stronger profitability.

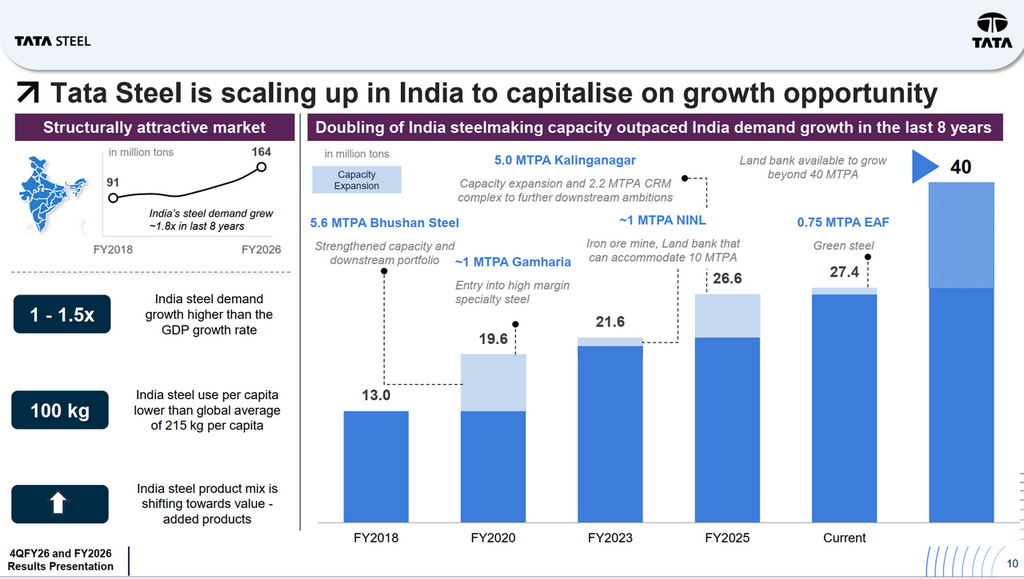

India, however, is telling a very different story. The country’s steel demand expanded from 91 million tonnes in FY2017-18 to 164 million tonnes in FY2025-26, growing nearly 1.8x within eight years. Steel consumption growth has continued to outpace GDP growth by around 1-1.5x, while per capita steel use remains only 100 kg, less than half of the global average of 215 kg. In other words, India is still one of the few major steel markets globally where long-term demand growth appears structurally supported rather than cyclical.

This changing landscape sits at the center of Tata Steel’s transformation. The company is increasingly becoming a two-speed story: India is driving growth, margins and cash flow, while Europe is testing the economics of green steel transition.

Operational Performance: Tata Steel’s Future Is Increasingly Being Built Around India

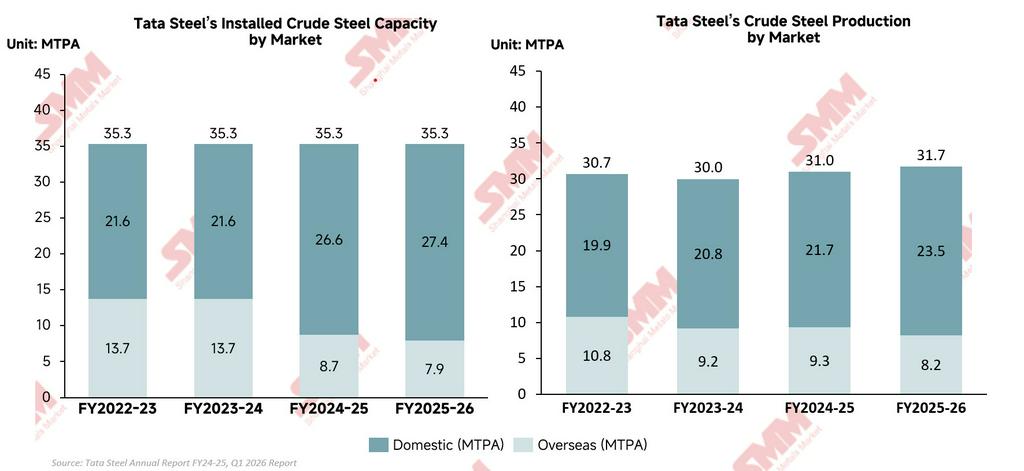

The operational performance of Tata Steel has revealed a much deeper structural shift inside the company. While consolidated crude steel production increased only moderately from 30.92 million tonnes in FY2025 to 31.67 million tonnes in FY2026, the real story was the accelerating rise of India as the company’s core growth and earnings engine. India is no longer simply Tata Steel’s largest market, it is becoming the foundation of the company’s long-term strategy. Domestic crude steel production climbed from 21.67 million tonnes in FY2025 to a record 23.48 million tonnes in FY2026, while overseas production declined from 9.3 million tonnes to 8.2 million tonnes. This contrast clearly highlights how Tata Steel’s operational momentum is shifting away from Europe and becoming increasingly concentrated in India, where infrastructure spending, manufacturing growth, and urbanization continue to support stronger steel demand fundamentals.

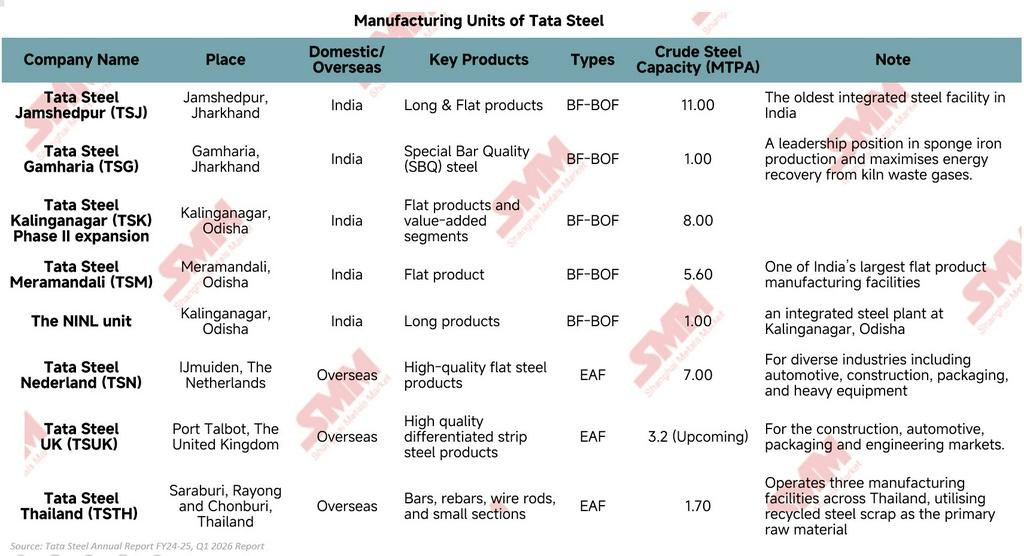

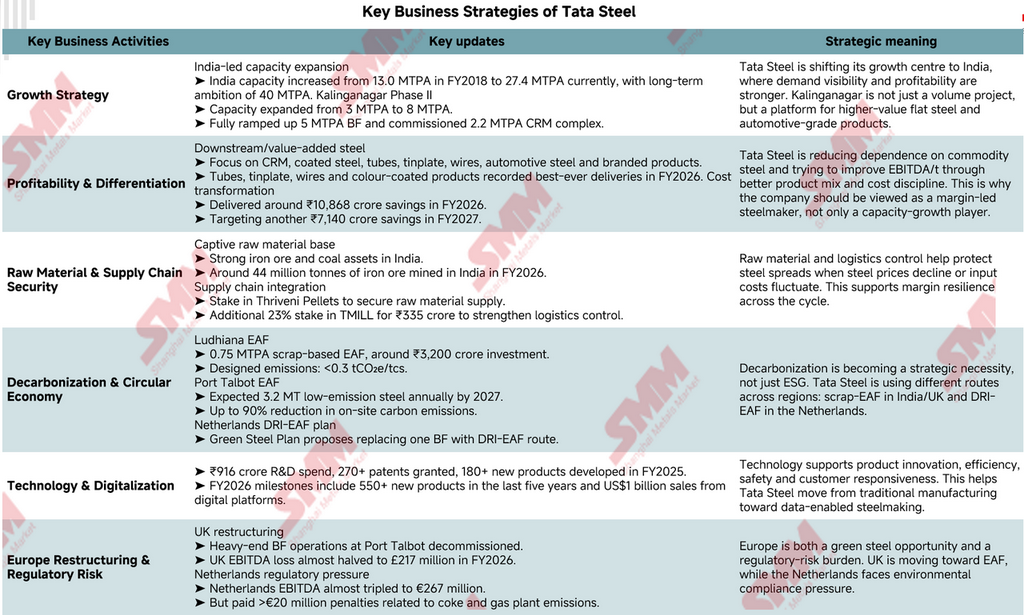

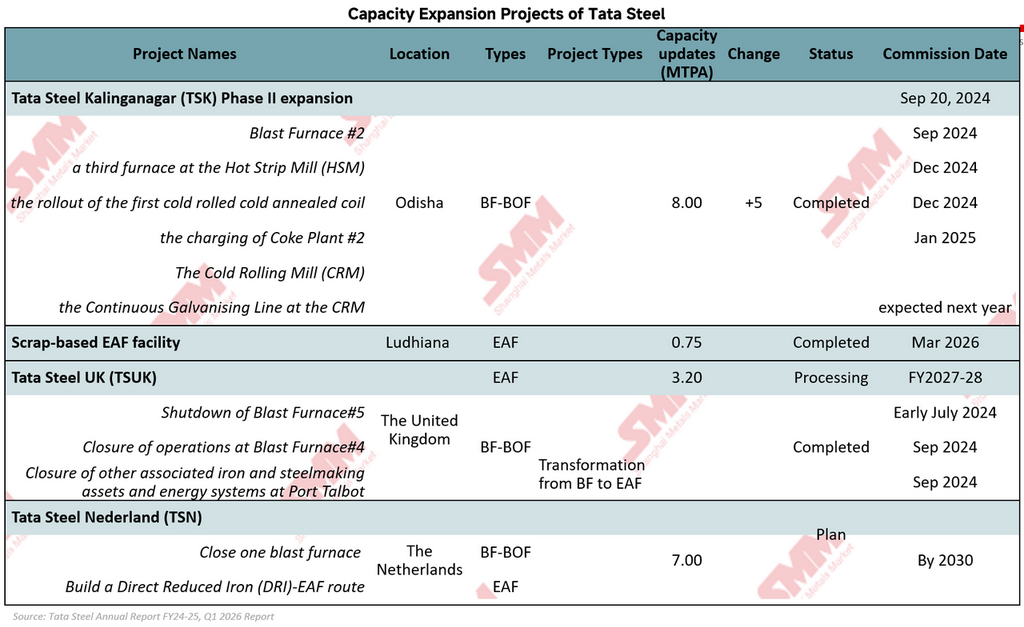

To capture India’s strong steel demand growth, Tata Steel has aggressively expanded its domestic steelmaking footprint over the past decade. India's crude steel capacity more than doubled from 13.0 MTPA in FY2018 to around 27.4 MTPA currently, with long-term ambitions toward 40 MTPA. Kalinganagar remains the centerpiece of this strategy, with Phase II expansion increasing capacity from 3 MTPA to 8 MTPA and strengthening Tata Steel’s downstream and automotive-grade steel capabilities.

In contrast, Europe remained primarily a restructuring story. Tata Steel UK continued transitioning toward EAF-based steelmaking, while Tata Steel Netherlands remained under pressure from high operating costs and environmental regulations. As a result, Tata Steel’s business structure is becoming increasingly divided: India is driving growth and profitability, while Europe is focused on decarbonization and operational transition.

Financial Performance: Tata Steel’s Earnings Recovery Was Driven by Margin Expansion and Cost Transformation

Tata Steel’s financial performance was not simply a cyclical rebound from weak steel markets. More importantly, it showed early signs that the company’s profitability structure is beginning to improve after several difficult years marked by weak spreads, European losses, and heavy transition costs.

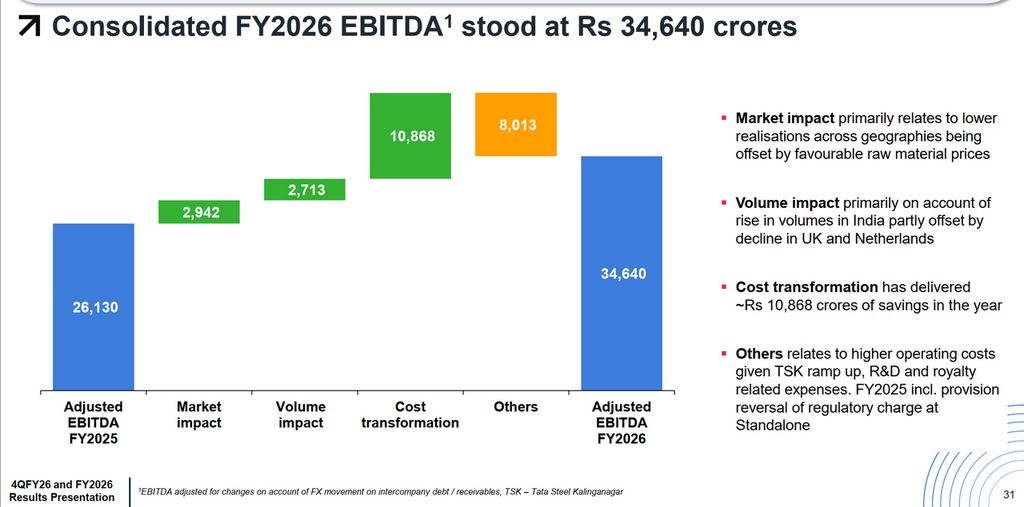

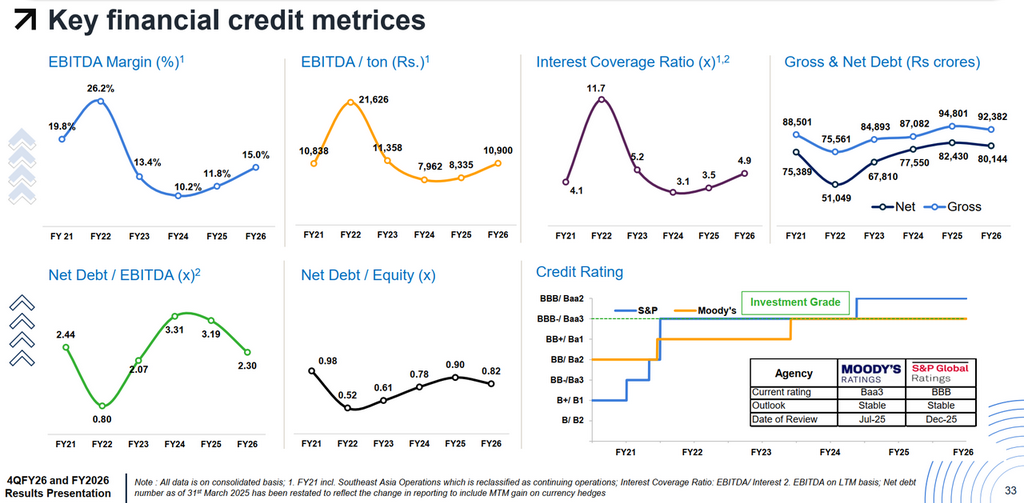

At first glance, the revenue growth looked relatively modest. Consolidated revenue increased by around 6% YoY to ₹2,32,140 crore. However, beneath the surface, profitability improved much faster than sales. EBITDA surged 35% YoY to ₹34,848 crore, while reported PAT jumped from ₹3,174 crore to ₹10,886 crore. This gap between revenue growth and profit growth is critical because it signals that Tata Steel was not merely selling more steel, it was operating more efficiently and extracting better profitability from its business. The clearest evidence of this came from EBITDA per tonne, which increased sharply from around ₹8,335/tonne in FY2025 to ₹10,900/tonne in FY2026. In practical terms, Tata Steel earned substantially more profit from each tonne sold despite ongoing pressure from volatile steel prices and weak global demand conditions. This suggests that the company’s recovery is becoming increasingly driven by internal improvements rather than external steel cycles alone.

A major reason behind this shift was Tata Steel’s aggressive cost transformation programme. The company disclosed that cost transformation contributed approximately ₹10,868 crore to EBITDA improvement in FY2026, far larger than the benefit from higher volumes. In fact, cost savings became one of the single biggest drivers of earnings recovery across the group. This reflects a broader strategic shift inside Tata Steel: management is no longer focused only on scale expansion, but increasingly prioritizing operational discipline, margin protection, and cash flow generation.

India once again remained the financial backbone of the group. Tata Steel India generated EBITDA of ₹34,272 crore with an EBITDA margin of around 24%, significantly outperforming the consolidated group margin of 15%. The contrast is increasingly striking: India is generating strong cash flows and healthy profitability, while Europe continues consuming capital as it undergoes restructuring and decarbonization.

At the same time, Tata Steel’s balance sheet also began to stabilize. Net Debt/EBITDA improved from 3.19x to 2.30x, while interest coverage increased to 4.9x. Despite maintaining elevated capex of more than ₹14,000 crore for India expansion and downstream projects, the company still generated positive free cash flow of around ₹10,738 crore. Maintaining investment-grade credit ratings from both Moody’s and S&P further reinforced improving market confidence in Tata Steel’s financial position.

However, the company’s financial story remains unusually complex compared with many global steelmakers. Tata Steel is effectively trying to finance two transformations simultaneously: a large-scale growth expansion in India and a costly green transition in Europe. This creates a delicate balancing act between growth, decarbonization, leverage, and shareholder returns. Therefore, while FY2026 marked a meaningful recovery year financially, the bigger question is whether Tata Steel can sustainably maintain this stronger profitability profile while continuing to absorb Europe’s transition costs over the next several years.

Key Business Activities: Tata Steel is Quietly Redefining What Kind of Steelmaker It Wants to Become

Tata Steel’s recent business moves reveal a company preparing for far more than the next steel cycle. Behind the capacity additions and restructuring headlines, the group is steadily rebuilding itself for an industry that is becoming tougher, greener, and far more margin-sensitive than before.

The clearest shift can be seen in the company’s product strategy. Tata Steel is moving deeper into automotive steel, coated products, tubes, tinplate, branded steel and downstream processing rather than relying heavily on commodity-grade output. Projects such as the Kalinganagar CRM complex are part of this push. The logic is straightforward: commodity steel is vulnerable to oversupply and violent price swings, while specialized steel products typically offer stickier customer relationships and stronger pricing power. Tata Steel is trying to move closer to end-users and further away from pure volume competition.

The company is also tightening control over its industrial ecosystem. Its captive iron ore and coal assets in India already provide a major advantage compared with many steelmakers exposed to volatile seaborne raw material markets. But Tata Steel is going further. Investments in Thriveni Pellets and TM International Logistics Limited (TMILL) strengthen control over pellet supply, transportation and logistics infrastructure. In a business where margins can disappear quickly, this kind of integration matters because it reduces exposure to external shocks across the supply chain.

Yet the biggest change is unfolding in decarbonization. Tata Steel is no longer discussing green steel as a distant ambition. It is already redesigning major parts of its production network around lower-emission technologies. In India, Tata Steel commissioned a 0.75 MTPA scrap-based Electric Arc Furnace (EAF) facility at Ludhiana in March 2026, backed by around ₹3,200 crore of investment and designed to achieve emissions below 0.3 tCO₂e per tonne of crude steel. In the UK, Tata Steel is transforming Port Talbot from blast furnace-based operations to EAF steelmaking, with the future facility expected to produce around 3.2 million tonnes of low-emission steel annually by FY2027-28 while reducing on-site carbon emissions by up to 90%. Meanwhile, Tata Steel Netherlands has proposed a Green Steel Plan based on closing one blast furnace and developing a Direct Reduced Iron–Electric Arc Furnace (DRI-EAF) route by 2030. These projects demonstrate that decarbonization is no longer treated as a standalone ESG initiative, but increasingly as a strategic requirement for long-term competitiveness and regulatory survival. What makes Tata Steel particularly interesting is that the company is not betting everything on one single decarbonization model. Instead, it is adapting different technologies depending on geography, regulation, energy economics and raw material availability. This gives Tata Steel more flexibility than many competitors still struggling to define a realistic transition roadmap.

Technology is becoming another important layer of this evolution. Tata Steel continues investing heavily in R&D, digital platforms and product innovation, not only to improve efficiency, but also to make the business more responsive to customers and changing market conditions. Over time, this could gradually push Tata Steel away from the image of a traditional steel producer and closer toward becoming a more advanced industrial materials company.

Taken together, these activities point to a broader reality: Tata Steel is no longer competing only on how much steel it can produce. The company is preparing for an industry where competitive advantage will increasingly depend on product quality, supply chain control, carbon intensity, technological capability and the ability to protect margins during volatile market cycles.

Conclusions

Tata Steel is no longer simply expanding steel capacity. It is rebuilding itself for a steel industry that will be more competitive, more carbon-constrained, and far more margin-sensitive than before. India has become the company’s main engine for growth, profitability and cash generation, while downstream expansion, supply-chain integration and cost transformation are strengthening earnings resilience across cycles. At the same time, Tata Steel is accelerating its transition toward low-carbon steelmaking through EAF and DRI-EAF investments across India, the UK and the Netherlands. However, this transformation also creates a difficult balancing act. The company must simultaneously fund aggressive expansion in India, absorb Europe’s restructuring and decarbonization costs, and maintain financial discipline in an increasingly volatile global steel market. Ultimately, Tata Steel’s future will depend on one critical question: Can the strength of its India business generate enough profitability and cash flow to successfully finance its transition into a more value-added and lower-carbon steel producer over the next decade?

![[SMM Steel Market Flash] Mexico Pushes to Drop 50% US Steel Tariffs in USMCA Review, More Talks Due in June-July](https://imgqn.smm.cn/usercenter/wSpkX20251217171718.png)

![[SMM Hot Topic] Against the Backdrop of Declining Global Steel Prices, Chinese Steel Companies See Profit Recovery](https://imgqn.smm.cn/usercenter/rKOND20251217171716.jpg)

![[SMM Steel] Tata Steel Sees Long-Term Growth Opportunity in India](https://imgqn.smm.cn/usercenter/UqlZJ20251217171717.jpg)