On May 26, 2026, the "2026 SMM Ferrous Salon — Hangzhou Session" event, jointly hosted by Zheshang Futures Co., Ltd. and SMM Information & Technology Co., Ltd., was successfully held. Nearly forty clients from the ferrous industry chain attended the conference, sharing and exchanging views on topics such as the current status of the ferrous industry, steel export opportunities, market trading hot topics, and steel enterprise risk management, inspiring future cooperation and trading ideas in the steel industry.

Chen Kaihang, Chief Black Series Analyst at Zheshang Futures Research Center, believes:

1. Rebar demand is declining, with supply adjusting to match demand. Electric furnace production remains resilient, while blast furnaces cannot deliver profits;

2. HRC is driven by international steel prices, but China's FOB needs to be in a price depression to gain export advantages;

3. Iron ore supply is increasing, demand is unlikely to grow, inventory is at high levels, costs are falling, and the downtrend is pronounced;

4. Coking coal speculation cannot drive steel, delivery issues persist, and risks will be greater after speculation ends;

Summary: HRC FOB determines the price ceiling of HRC futures, and the HRC-rebar spread will stay high or even continue to widen slightly. Steel raw material prices face downward pressure. Overall, the strategy for steel remains shorting on rallies. Bottom-fishing will only be feasible when blast furnace rebar production pulls back again.

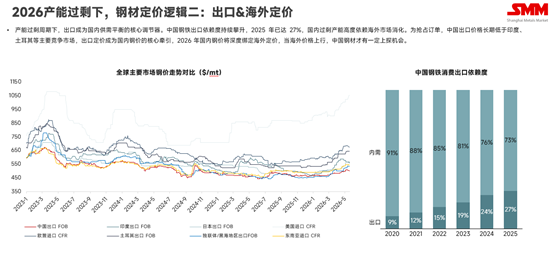

SMM senior ferrous metals analyst Ding Xiaoli stated:

In an overcapacity cycle, exports have become the core regulator of China's supply-demand balance. China's dependence on steel exports has continued to climb, reaching 27% in 2025, with domestic surplus capacity highly reliant on markets outside China for absorption. To secure orders, China's export prices have long remained below those of major competing markets such as India and Turkey, making export pricing the core driver of domestic steel prices. In 2026, domestic steel prices will be deeply tied to ex-China pricing, and only when prices outside China rise will Chinese steel have some upside potential.

![[SMM Analysis] Construction Steel Demand Shifted from Decline to Growth This Period](https://imgqn.smm.cn/usercenter/exdqc20251217171717.jpg)

![[SMM Analysis] India–Oman CEPA: Zero Tariffs and a Weaker Rupee Reshape Middle East Steel](https://imgqn.smm.cn/usercenter/ikbxI20251217171718.jpg)

![[SMM Steel] Brazil Steel Import Quota Utilization Reaches 60% Average Rate](https://imgqn.smm.cn/usercenter/ocJKj20251217171717.jpg)