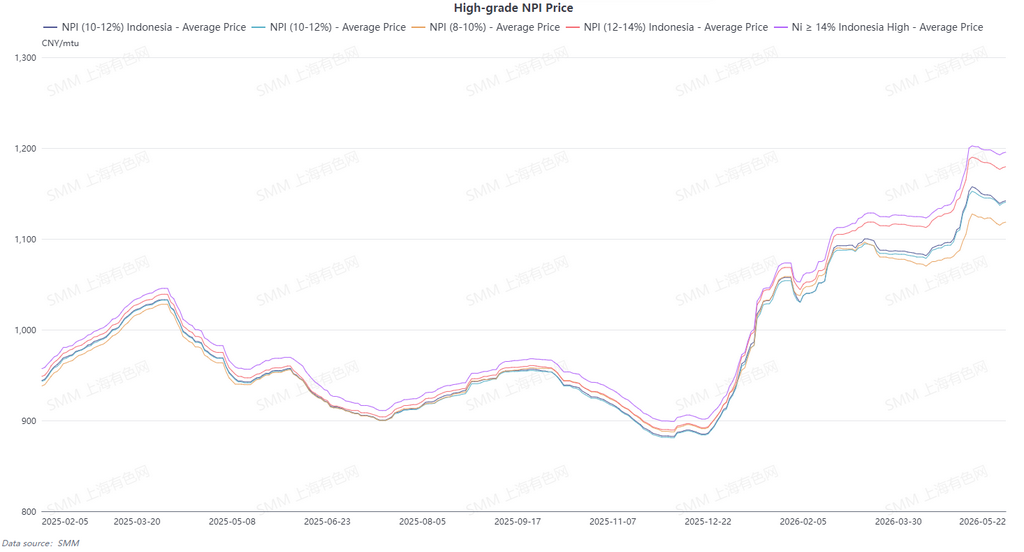

The SMM 10-12% high-grade NPI average price fell 5.7 yuan/nickel unit WoW to 1,140.3 yuan/nickel unit (ex-factory, tax included), while the Indonesian NPI FOB index average price fell 1.23 $/nickel unit WoW to 146.52 $/nickel unit. Downstream purchasing sentiment saw a more pronounced decline, with the divergence in mindset between upstream and downstream intensifying.

Supply side, NPI production cut plans, coupled with disruptions from Indonesian export policies, led to a gradual tightening of spot cargo availability. Upstream enterprises had a strong willingness to hold back from selling and hold prices firm, with overall quotes staying high. Quotes only softened slightly when futures came under pressure, and willingness to sell at lower levels was generally low. The expectation of tight market supply provided floor support for prices. Demand side, the stainless steel market struggled to rise, and steel mills became increasingly cautious in procurement, mainly restocking on a just-in-need basis. The price advantage of steel scrap continued to widen, with downstream buyers clearly pushing for lower prices. Their intended purchase prices remained concentrated at 1,120–1,130 yuan/nickel unit for an extended period, showing a significant price spread from upstream quotes, making it difficult to bridge the supply-demand price divergence. Looking ahead, supply contraction expectations are expected to underpin spot prices, but futures weakness and raw material SHFE/LME price ratio constraints will continue to suppress prices. High-grade NPI prices are expected to hover at highs next week.

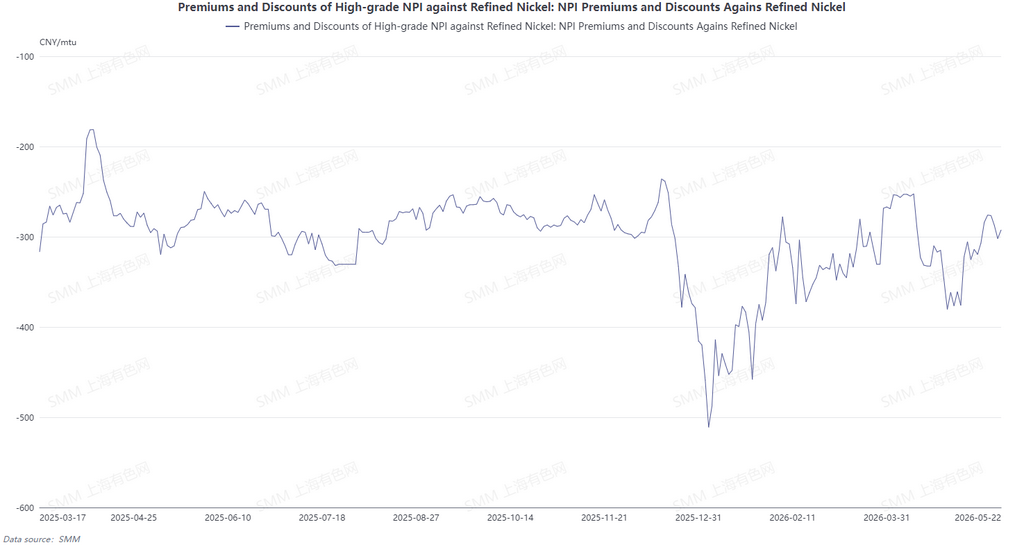

From the perspective of conversion of NPI to high-grade nickel matte, the refined nickel price center moved lower this week, and high-grade NPI prices edged down. The average discount of high-grade NPI to refined nickel narrowed to 286.9 yuan/nickel unit. High-grade NPI prices are expected to continue fluctuating at highs next week, while refined nickel prices are expected to edge down. The average discount of high-grade NPI to refined nickel is expected to continue converging, and the profitability of NPI-to-nickel-matte conversion is expected to turn negative.

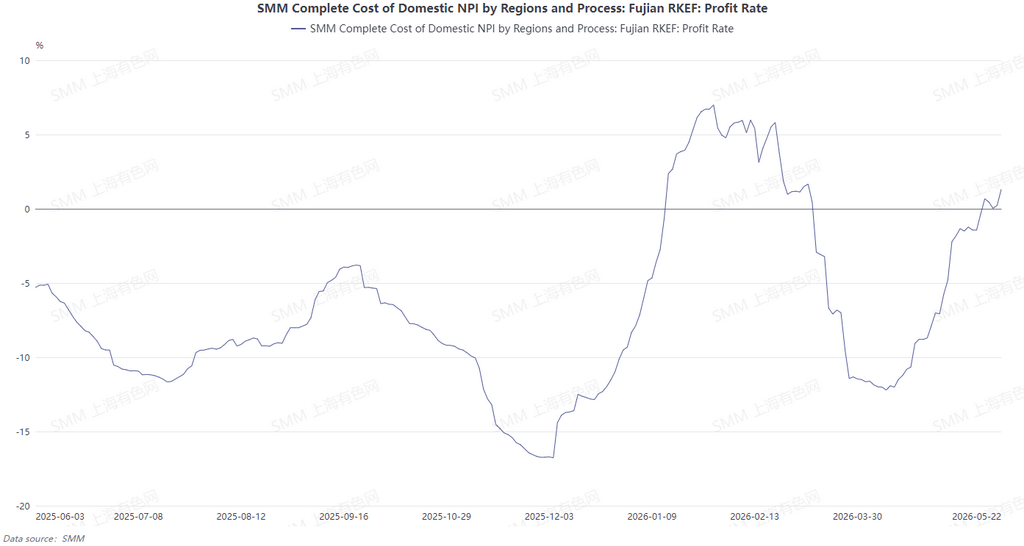

Based on the cash cost of high-grade NPI calculated using nickel ore prices from 25 days ago, high-grade NPI smelter profits continued to recover during the week. Raw material side, auxiliary material prices fluctuated slightly this week, and Philippine nickel ore prices remained flat at lows. The continued decline in Philippine nickel ore prices kept driving down domestic production costs in China, while high-grade NPI prices stayed at highs, with some domestic smelters' profits already surpassing those in Indonesia. Next week, high-grade NPI prices are expected to still fluctuate at highs, and smelter profits will be maintained.

![[SMM Analysis] Macro Uncertainty Weighs on Stainless Futures; Low Inventory and Demand Underpin Cash Market](https://imgqn.smm.cn/production/admin/votes/imageshyuTG20260522182711.png)

![[SMM Analysis] Overseas Stainless Steel Weekly Review: Indonesia Export Control Policy Ignites Market Expectations](https://imgqn.smm.cn/usercenter/biBGl20251217171733.jpg)