In April 2026, China's copper cathode import and export market exhibited a clear pattern of "rising imports and falling exports." As some domestic consumption demand recovered and the price spread between domestic and overseas markets adjusted, copper cathode imports registered double-digit growth MoM, while exports pulled back notably after a high base in the prior period. Notably, inflows of EQ copper cathode from countries such as the DRC and Russia remained elevated, pushing the share of EQ copper imports in April to above 70%, hitting a record high for the same period in recent years.

Based on the total import and export data released by the General Administration of Customs, China's copper cathode exports in April were 25,600 mt, down 56.01% MoM and down 67.05% YoY. Although single-month exports saw a notable seasonal pullback, combined with overall Q1 performance, cumulative exports from January to April still maintained positive growth of 30.84% YoY. On the import side, China's copper cathode imports in April rebounded to 270,500 mt, up 15.27% MoM and up 8.19% YoY. The rebound in April imports effectively eased the tight spot cargo conditions in parts of the domestic market. However, from a longer-term perspective, cumulative imports from January to April were still down 21.10% YoY, reflecting structural adjustments in overall long-term contract and spot cargo flows this year compared with previous years.

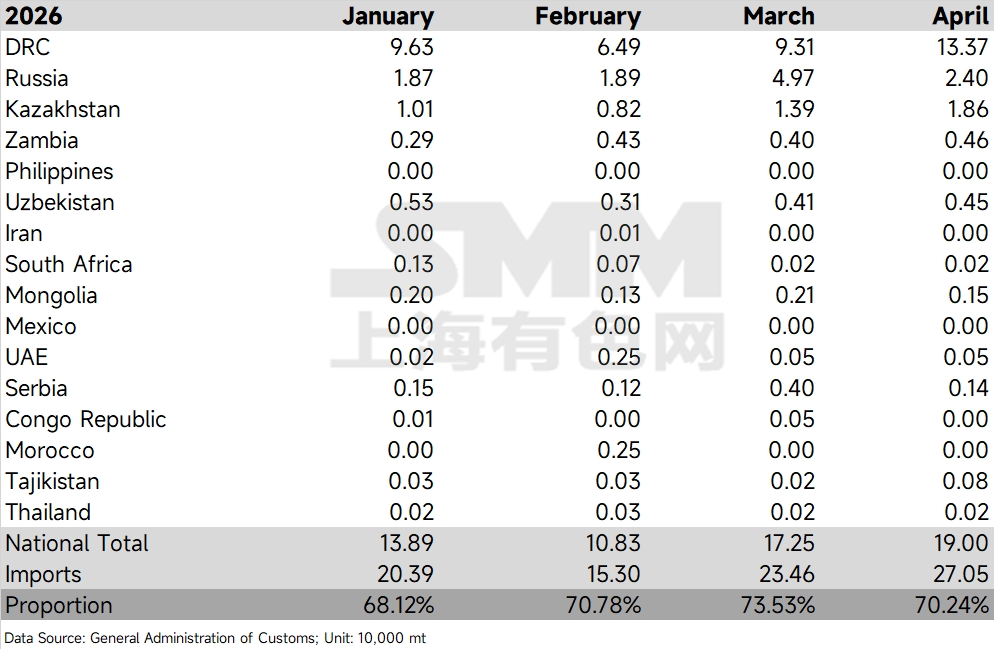

A deeper analysis of the import structure reveals that the major EQ copper cathode source countries within the statistics collectively contributed the vast majority of the incremental volume, with the DRC continuing to stand out as the top performer. In April, China's copper cathode imports from the DRC reached 133,700 mt, a significant increase of over 40,000 mt from March's 93,100 mt, representing a notable MoM gain and solidifying its position as the largest supplier of EQ copper to China. In comparison, April copper cathode imports from Russia came in at 24,000 mt, a pullback from March's 49,700 mt; supply from Kazakhstan rose steadily to 18,600 mt; others such as Zambia recorded 4,600 mt and Uzbekistan recorded 4,500 mt, maintaining an overall stable inflow.

Guided by this flow pattern, total imports from major EQ source countries reached 190,000 mt in April, showing a continuously rising trend compared to 138,900 mt in January, 108,300 mt in February, and 172,500 mt in March. In terms of the share trend, EQ copper cathode imports accounted for 70.24% in April. Although this pulled back slightly by 3.29 percentage points from March's historical high of 73.53%, a comparison over a longer timeframe against historical data from 2022 to 2026 shows that this ratio is far above the typical fluctuation range of 45%–65% during the same period from 2022 to 2024, basically flat with the 2025 highs with a slight breakthrough. This indicates that EQ sources have become the de facto absolute dominant supply in China's current copper cathode imports.

Looking ahead, the proportion of EQ copper cathode imports has remained at a high level above 70% for three consecutive months, indicating that the penetration of geopolitical flow shifts and new ex-China smelting capacity into the Chinese market is deepening further. The MoM rebound in April imports was primarily driven by some rigid restocking demand during China's traditional Q2 peak season and a phased improvement in the import window. EQ copper, with its certain price advantage, has been absorbed smoothly within the current copper cathode system. Going forward, close attention should be paid to the pace of ex-China EQ cargo arrivals at ports from May to June, as well as changes in operating rates of downstream enterprises in China toward the end of the peak season. If consumption fails to continuously absorb the high inflow of EQ copper, visible inventory in China may face localized inventory buildup pressure.

It is worth noting that in Africa, taking the DRC as an example, copper is basically produced through SX-EW. Earlier issues such as sulphuric acid and sulphur shortages may have led to production cuts, and the volume flowing into China is expected to see limited significant increase going forward. In addition, it has recently been observed in the spot market that some EQ cargo originates from countries such as Chile that primarily produce registered copper, which means the actual proportion of EQ copper cathode entering China is estimated to be higher than the statistics above suggest.

![BC Copper Closed Slightly Lower Intraday as Persistent Rate Hike Expectations Continued to Weigh on the Market [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/EOMNB20251217171709.jpg)

![[SMM Analysis] Regional price gaps stay high. Why have the high-price and low-price regions of sulfuric acid shifted?](https://imgqn.smm.cn/usercenter/tXxfd20251217171713.jpg)