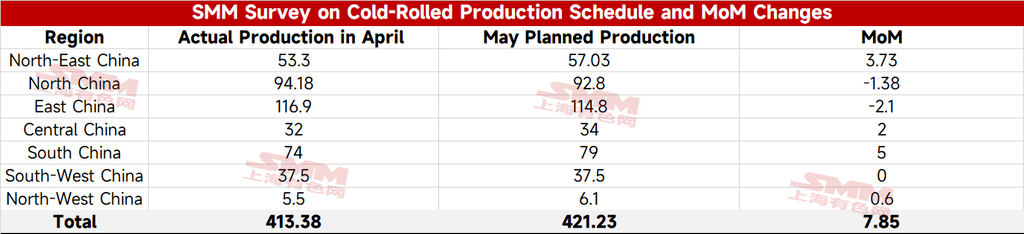

- SMM Cold-Rolled Production Schedule: May Steel Mill Cold-Rolled Production Schedule Up 2%, Daily Average Production Schedule Down 1.4%

According to the latest SMM tracking data, the total planned cold-rolled commercial steel volume from 31 mainstream cold-rolled sheet and coil steel mills was 4.2123 million mt this month, up 78,500 mt MoM from actual cold-rolled commercial steel production, an increase of 1.9%.

On a daily average basis, May had one more day than April. The daily average cold-rolled commercial steel production schedule in May was 135,900 mt, down 1.4% MoM from the daily average actual cold-rolled commercial steel production in the previous month.

- SMM HRC Production Schedule: May HRC Production Schedule Up 0.3% MoM, Daily Average Down 3%

According to the latest SMM tracking data, the total planned HRC commercial steel volume from 39 mainstream steel mills was 13.3564 million mt this month, up 37,400 mt MoM from actual HRC commercial steel production, an increase of 0.3%.

On a daily average basis, May had one more day than April. The daily average HRC commercial steel production schedule in May was 430,900 mt, down 3.0% MoM from April's actual daily average production.

Currently, steel mill profits and order conditions were favorable, and production enthusiasm was high. The overall May production schedule was basically flat MoM compared to April's actual production. May had fewer days than April, and on a daily average basis, steel mills' HRC production schedule declined MoM.

Summary: Total production schedule for hot-rolled commercial steel at steel mills in May was basically flat MoM. However, since May has more days than April, the daily average production schedule decreased MoM, and supply pressure was slightly lower than previous expectations.

Demand side, sheets & plates demand is expected to weaken marginally in mid-to-late May. Hot-rolled coil inventory is expected to continue destocking over the next 2–3 weeks, and the accumulation of supply-demand imbalance before month-end in May will be limited.

Other aspects, the ex-China energy premium is unlikely to ease in the short term, and hot metal production continues at elevated levels. HRC prices are expected to fluctuate at highs before late May. During this period, the pullback in coking coal prices driven by expectations of easing Middle East conflicts and the periodic weakening in export order-taking for hot-rolled coils are expected to put prices under pressure temporarily, though the downside is limited.

![[SMM Iron & Steel] US Iron & Steel Scrap Exports Fall 27.1% MoM in April 2026](https://imgqn.smm.cn/usercenter/Zznfn20251217171716.jpg)