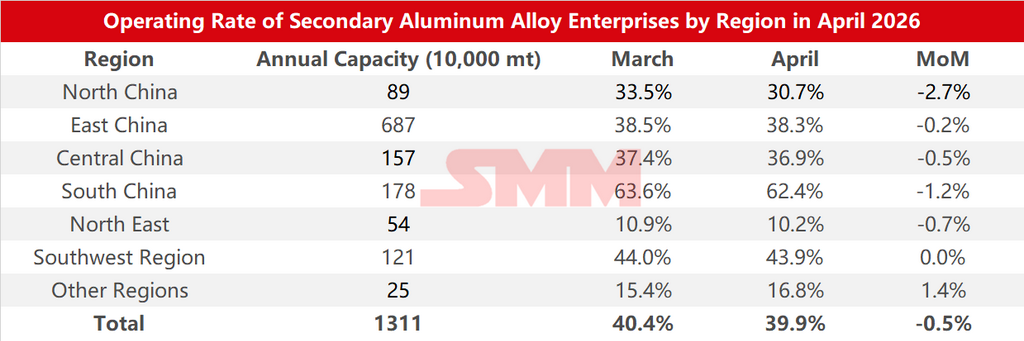

Survey Data on Operating Rates of Secondary Aluminum Alloy Enterprises by Region in April 2026:

According to SMM survey statistics, the operating rate of the secondary aluminum industry in April 2026 edged down 0.5 percentage points MoM from March to 39.9%.

Production divergence among enterprises was evident in April. The relatively stable operating rate was mainly supported by three factors: first, the spot price center of ADC12 shifted downward in April, stimulating some price-sensitive clients and driving a partial recovery in order demand;

Second, the price spread between domestic and overseas markets continued to widen, improving export profits. Some enterprises actively adjusted their order structures and increased export proportions, offsetting the pressure from declining domestic orders;

Third, against the backdrop of weakening spot prices, traders entered the market at low prices to purchase alloy ingots, partially filling the order gap caused by weakening end-use consumption.

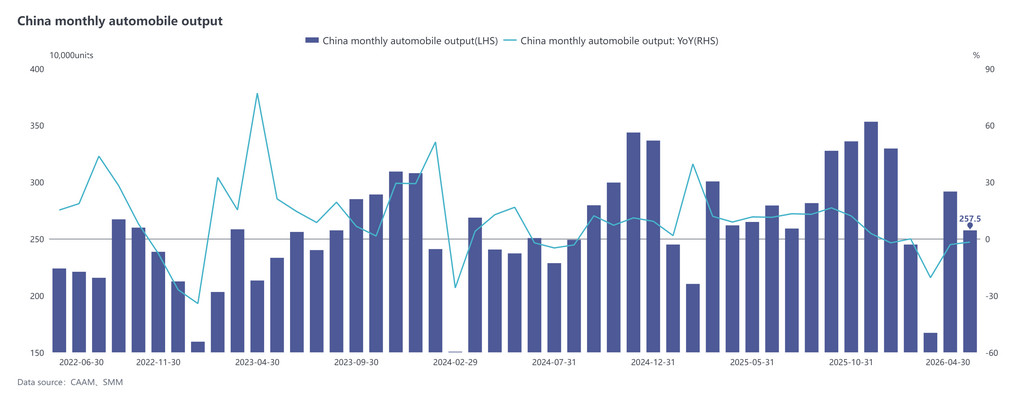

However, production cuts were also fairly widespread across the industry, primarily due to weakening end-use consumption. According to CAAM data, automobile production and sales in April reached 2.575 million units and 2.526 million units respectively, down 11.7% and 12.9% MoM, and down 1.7% and 2.5% YoY respectively. End-use demand under pressure led to order contraction at secondary aluminum plants and mounting sales pressure, passively dragging down operating rates. However, some enterprises did not adjust their production pace accordingly, and the mismatch between production and sales resulted in continued accumulation of finished product inventories.

Raw material pressure should not be overlooked either. In early April, rising primary aluminum prices drove up aluminum scrap costs. Stricter supervision on reverse invoicing, combined with an inverted price spread between domestic and overseas markets, led to tight supply of invoiced goods and low market circulation volumes. From mid-April onward, aluminum prices turned downward, but aluminum scrap declined only marginally as suppliers held back from selling, causing the industry's theoretical profit-loss balance to shift from profit to loss, further highlighting operational pressure on enterprises. Against this backdrop, some enterprises were forced to reduce load or even halt production due to insufficient raw material supply or compliance policy constraints.

Overall, production divergence among enterprises in the secondary aluminum alloy industry was significant in April, with the overall operating level edging down within a narrow range.

Entering May, demand continues the weakening trend since mid-April, and the subdued pattern is unlikely to change in the short term. Downstream enterprises hold cautious expectations for the market outlook, believing prices have not yet reached a phased low, with weak restocking willingness and wait-and-see sentiment continuing to dominate the market. The phased reduction in orders during the Labour Day holiday directly weighed on enterprise production. Although the operating rate rebounded slightly after the holiday, the recovery was limited. Under the combined pressures of a prolonged demand off-season, tight compliant raw material supply, and restrictions on reverse invoicing, the industry's overall operating rate in May still has room for further decline.