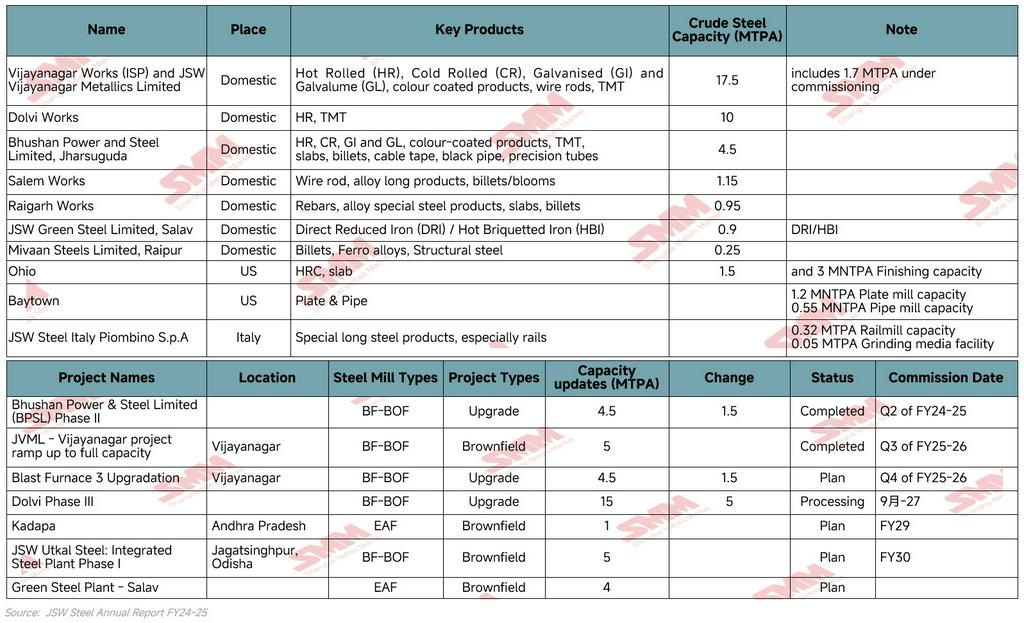

JSW Steel remains India’s largest steelmaker, with 34.2 MTPA domestic crude steel capacity, including 1.7 MTPA under commissioning, and 35.7 MTPA consolidated capacity. The company is supported by 23 captive iron ore mines and 3 coking coal mines, giving it an increasingly integrated position across the steel value chain.

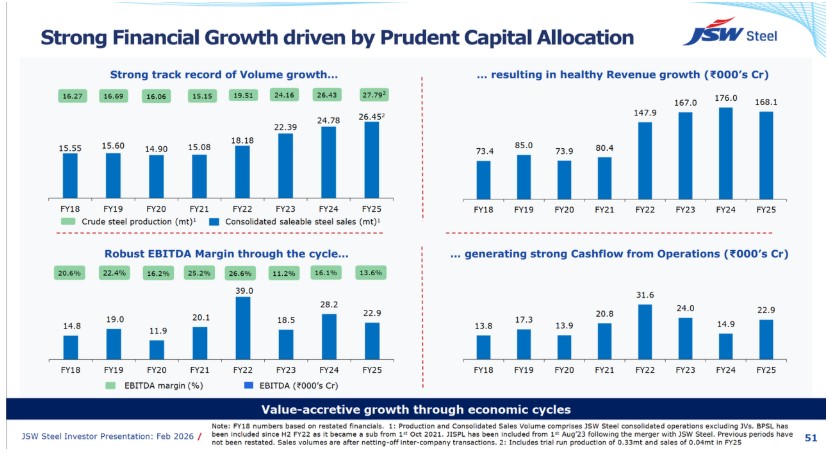

In FY2024-25, JSW achieved record crude steel production of 27.79 MnT, up 5.1% YoY, and steel sales of 26.45 MnT, up 6.7% YoY. Value-added and special products accounted for 62% of total sales, showing that the company is not simply expanding output, but also trying to improve the quality of its sales mix.

However, the year also showed the limit of scale-led growth. Despite higher production and sales, JSW’s revenue and margins declined due to weaker steel realisations. The core issue is therefore not whether JSW can grow larger. The more important question is whether it can convert its scale into stronger, more stable, and higher-quality earnings.

Operational Performance: JSW’s Expansion is Not Just a Volume Race, but a Repositioning of its Production Platform

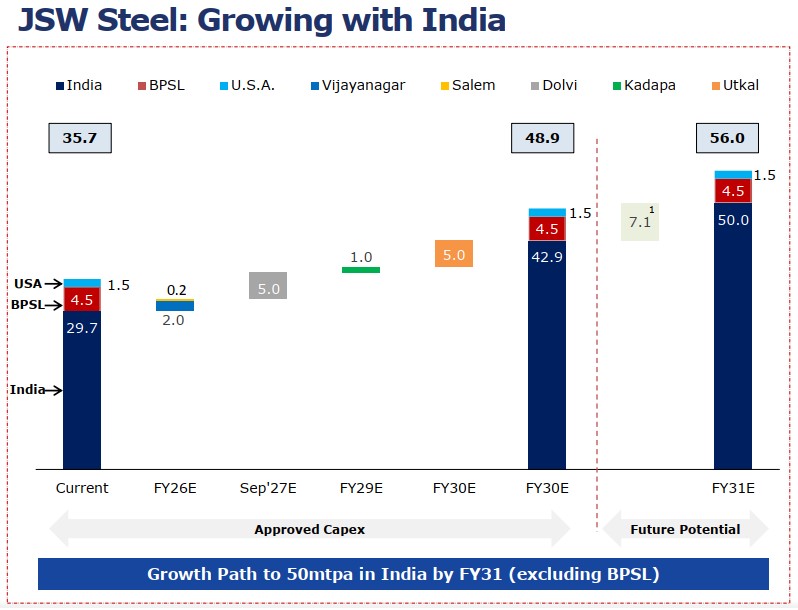

JSW Steel’s capacity strategy is clearly anchored in India. Its current consolidated crude steel capacity is 35.7 MTPA, including 34.2 MTPA in India and 1.5 MTPA in the US. Under approved capex, total JSW Steel capacity is expected to increase to 48.9 MTPA by FY2030E, mainly driven by domestic brownfield and integrated projects. The company’s longer-term ambition is to reach 56.0 MTPA total capacity including BPSL and the US by FY2031E.

The company’s capacity strategy is not random expansion. It is built around three clear directions.

-

First, it is strengthening existing large hubs such as Vijayanagar and Dolvi, where brownfield expansion can deliver faster ramp-up and better capital efficiency.

-

Second, it is building new regional growth platforms such as Utkal in Odisha, which gives JSW better access to eastern India’s raw material base and industrial demand.

-

Third, it is adding future-oriented production routes through Kadapa EAF and the Salav green steel project, which provide flexibility as low-carbon steel demand gradually emerges.

This makes JSW’s capacity expansion more strategic than a simple scale-up story. Vijayanagar and Dolvi protect scale, Utkal improves resource linkage, Kadapa adds EAF optionality, and Salav supports decarbonization positioning. Together, these projects indicate that JSW is trying to build a larger, more regionally balanced and more product-specialised steel platform.

The most important operational signal is the 62% VASP share in FY2024-25. Capacity growth alone does not guarantee earnings growth. JSW’s ability to sustain margins will depend on whether new capacity can be absorbed into higher-value product categories such as coated steel, colour-coated steel, electrical steel, automotive steel, tinplate, and specialized long products.

Therefore, JSW Steel is expanding capacity, but the real strategic goal is to improve the quality of growth. The company is trying to shift from simply producing more steel to producing more differentiated and margin-resilient steel.

Financial Performance: Price Realisation, Not Demand, Drove The Margin Squeeze

Although JSW Steel delivered record production and sales in FY2024-25, its revenue declined because the company sold more steel at lower average realisations. Consolidated crude steel production increased from 26.43 mt in FY2023-24 to 27.79 mt in FY2024-25, while consolidated saleable steel sales rose from 24.78 mt to 26.45 mt. However, consolidated revenue from operations declined from ₹175,006 crore to ₹168,824 crore, while operating EBITDA margin narrowed from 16.1% to 13.6%. This shows that FY2024-25 was a volume-positive but price-negative year for JSW Steel.

In FY2024-25, JSW’s sales volume increased, but at lower average realisations. The positive impact of higher sales volume was more than offset by weaker selling prices. This made FY2024-25 a volume-positive but price-negative year for the company.

At the standalone level, the pressure was even clearer. JSW Steel’s revenue from operations declined 6% YoY to ₹127,702 crore, despite sales volume rising 2.5% YoY. The company directly attributed this decline to a 9% fall in both domestic and export sales realisations, caused by subdued domestic steel pricing, lower international steel prices, and higher steel imports into India. This means the revenue decline was not caused by weaker demand for JSW’s products. In fact, domestic sales remained strong, rising 8.1% YoY to 20.50 mt, supported by infrastructure, housing construction, manufacturing growth, and auto-sector demand. The weakness came from pricing. Export sales also fell sharply by 44.8% YoY to 1.24 MnT, while lower export prices further dragged down overall realisations.

The same pressure flowed through to profitability. Lower selling prices reduced revenue per tonne, while lower iron ore and coking coal prices only partially offset the impact. As a result, standalone operating EBITDA fell 16% YoY to ₹18,381 crore, and the EBITDA margin declined from 16.26% to 14.39%.

JSW’s FY2024-25 margin pressure was not an operational volume problem. It was a price realisation problem. The company produced and sold more steel, but weaker domestic and export prices reduced average revenue per tonne. Therefore, higher sales volumes were not enough to prevent a decline in revenue, EBITDA, and margins. This is why JSW’s next phase cannot rely on capacity expansion alone. To improve earnings quality, the company needs stronger VASP contribution, better raw material security, deeper downstream integration, and more differentiated products.

JSW Steel Mills Overseas: Strategic Assets, but Still Uneven Profit Contributors

JSW Steel’s overseas mills are strategically important, but they are not yet the core earnings driver. The company’s international footprint mainly includes Ohio and Baytown in the US, and Piombino in Italy, making JSW one of India’s more geographically diversified steel producers. However, compared with the Indian business, these assets remain smaller, more volatile, and more exposed to local market cycles.

The US operations show the mixed nature of JSW’s overseas portfolio:

-

Ohio

-

1.5 MTPA EAF, 2.8 MTPA continuous slab caster, and 3.0 MTPA hot strip mill

-

Revenue stood at US$588.36 million, while operating EBITDA was negative at US$54.84 million

-

Capacity utilisation declined to 61%, compared with 66% in FY2023-24, mainly because weaker HRC and slab realisations were not fully offset by lower scrap prices.

-

Baytown Plate & Pipe Mill

-

Generate US$547.78 million revenue and US$20.15 million EBITDA

-

Focus on a more downstream-oriented product base, including plate and pipe

The Italian operation is smaller but more differentiated:

-

Generate €275.72 million revenue and €14.98 million operating EBITDA.

-

Focus on special long steel products, especially rails, supported by a 0.32 MTPA rail mill, a 0.05 MTPA grinding media facility, and a captive industrial port

Overall, JSW’s overseas mills should be viewed as selective capability-building platforms rather than major growth engines. The US business provides market access, slab-to-plate integration and exposure to energy/infrastructure steel demand, but profitability remains volatile. Italy is smaller but more specialised and appears relatively more stable due to its rail-focused positioning. Therefore, overseas assets support JSW’s international presence, but the company’s main earnings and capacity growth story remains firmly anchored in India.

Key Business Activities: How JSW Plans to Turn Scale into Quality Growth?

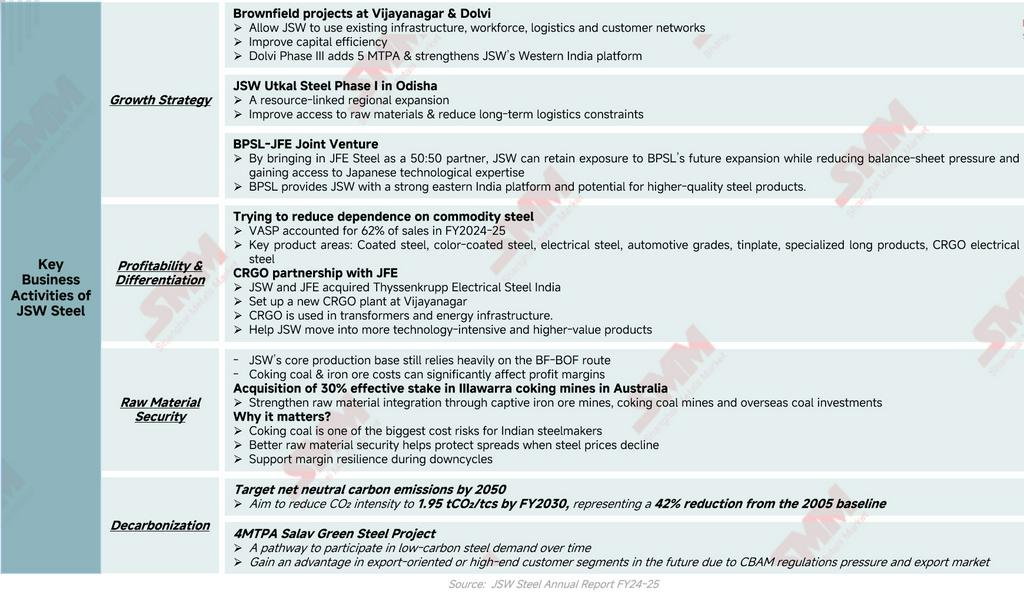

JSW Steel’s key business activities show that the company is trying to move from scale-led growth to quality-led growth. The strategy can be understood through four main directions: capacity expansion, profitability and product differentiation, raw material security, and decarbonization.

First, the growth strategy remains anchored in large-scale capacity additions, especially brownfield projects at Vijayanagar and Dolvi, the Utkal Phase I project in Odisha, and the BPSL-JFE joint venture. These projects allow JSW to expand capacity while improving capital efficiency, regional coverage, raw material access and technological capability. In particular, the BPSL-JFE partnership helps JSW reduce balance-sheet pressure while gaining access to Japanese steelmaking expertise for higher-quality products.

At the same time, JSW is strengthening its profitability through product differentiation. The company is reducing dependence on commodity steel by increasing its exposure to value-added and special products, which accounted for 62% of sales in FY2024-25. Its focus on coated steel, colour-coated steel, electrical steel, automotive grades, tinplate and specialised long products helps improve margin resilience. The CRGO partnership with JFE further supports JSW’s move into more technology-intensive and higher-value electrical steel products used in transformers and energy infrastructure.

Raw material security is another key part of JSW’s strategy to JSW’s earnings resilience. The company’s core production base still relies heavily on the BF-BOF route, making iron ore and coking coal costs critical to profitability. By strengthening captive mines and acquiring a 30% effective stake in Illawarra coking coal mines in Australia, JSW is trying to reduce input-cost volatility and protect margins during steel price downcycles. This upstream strategy is not only about securing supply; it is also about protecting spreads.

Finally, decarbonization is becoming a long-term competitiveness issue rather than only an ESG target. JSW aims to reach net neutral carbon emissions by 2050 and reduce CO₂ intensity to 1.95 tCO₂/tcs by FY2030. The planned 4 MTPA Salav green steel project, together with EAF, DRI/HBI, green hydrogen and renewable energy initiatives, gives JSW optionality in future low-carbon steel demand.

Conclusion: Bigger is No Longer Enough

JSW Steel’s FY2024-25 performance presents a clear growth paradox. The company achieved record crude steel production and sales, but revenue and margins declined because weaker steel realisations outweighed the benefit of higher volumes. This does not mean JSW’s operating fundamentals are weak. On the contrary, the company remains India’s largest steelmaker, with a strong domestic demand base, large integrated assets, high VASP share and an expanding project pipeline. However, FY2024-25 shows that scale alone is not enough in a price-pressured steel market.

The next stage of JSW’s growth will depend on whether the company can convert scale into higher-quality earnings. This requires more than capacity expansion. It requires higher VASP contribution, stronger raw material security, better downstream integration, selective overseas improvement, technology partnerships and decarbonization readiness.

Therefore, JSW Steel should not be viewed simply as a company expanding from one capacity number to another. The more important story is that JSW is trying to transform itself from a large Indian steelmaker into a more integrated, differentiated and carbon-ready steel platform. Its biggest test is no longer production growth. It is margin quality.

![SMM Iron & Steel] ArcelorMittal Kryvyi Rih Suspends Steel Production Due to Severe Logistics Disruptions](https://imgqn.smm.cn/usercenter/JdqON20251217171718.png)

![[SMM Iron & Steel] US Issues Preliminary AD Results for Large Diameter Welded Pipe from India](https://imgqn.smm.cn/usercenter/HbWNv20251217171718.jpg)

![[SMM Iron & Steel] US Steel Mill Shipments Surged 10.9% in March 2026; Q1 Down Slightly](https://imgqn.smm.cn/usercenter/zbJUC20251217171718.jpg)