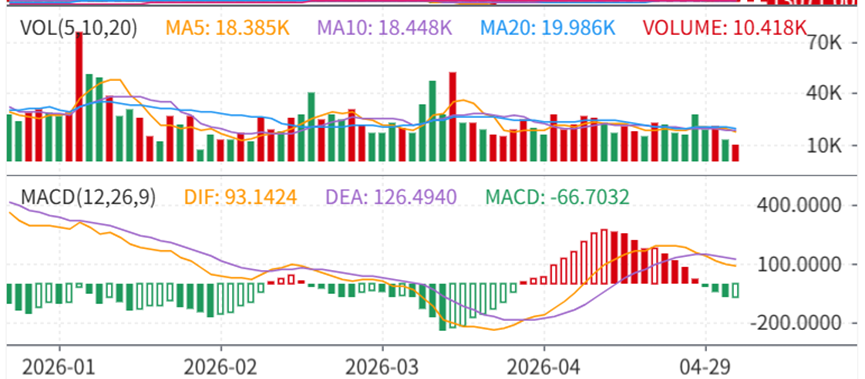

Trong kỳ nghỉ Quốc tế Lao động 2026 (1–5/5), thị trường SHFE Trung Quốc đóng cửa, đồng LME biến động theo xu hướng giảm trước rồi phục hồi sau. Trước kỳ nghỉ, hợp đồng đồng SHFE 2605 đóng cửa ở mức 100.970 nhân dân tệ/tấn, đồng LME đóng cửa ở mức 13.019 USD/tấn vào ngày 30/4. Trong kỳ nghỉ, đồng LME chạm mức cao 13.120 USD/tấn vào ngày 1/5 trước khi trung tâm giá dịch chuyển xuống, chạm đáy 12.780 USD/tấn vào ngày 4/5 rồi phục hồi, đóng cửa ở mức 13.030 USD/tấn vào ngày 5/5, tăng nhẹ 0,64% so với giá mở cửa ngày hôm trước.

I. Về mặt vĩ mô

Trong kỳ nghỉ Quốc tế Lao động khi thị trường Trung Quốc đóng cửa, các diễn biến vĩ mô toàn cầu, thị trường hàng hóa và động thái chính sách ngoài Trung Quốc tiếp tục diễn ra. Nhiều yếu tố bên ngoài đẩy trung tâm giá đồng dịch chuyển giảm nhẹ trong kỳ nghỉ. Một mặt, kỳ vọng thắt chặt chính sách của Fed Mỹ và đối đầu địa chính trị gây áp lực giảm; mặt khác, các yếu tố cơ bản thắt chặt tạo hỗ trợ đáy, khiến giá đồng đi ngang trong trạng thái trầm lắng.

Bất ổn địa chính trị tiếp diễn.Ngày 4/5, chỉ huy cấp cao Vệ binh Cách mạng Hồi giáo Yadollah Javani xác nhận Iran đang kiểm soát eo biển Hormuz và các tàu thù địch cố tình vượt qua sẽ bị xử lý kiên quyết. Cùng ngày, Tổng thống Mỹ Trump từ chối làm rõ liệu thỏa thuận ngừng bắn Mỹ-Iran còn hiệu lực hay không, chỉ cảnh báo Iran sẽ bị "hủy diệt hoàn toàn" nếu tấn công tàu Mỹ. Thị trường đánh giá hai bên đã bước vào giai đoạn đối đầu, việc đi lại bình thường qua eo biển Hormuz khó có thể nối lại trong ngắn hạn, phí bù rủi ro dầu thô duy trì ở mức cao. Trong bối cảnh này, tâm lý chờ đợi quan sát chiếm ưu thế. Đồng LME chạm đáy kỳ nghỉ 12.780 USD/tấn vào ngày 4/5, sau đó đi ngang quanh mức 13.000 USD/tấn, chờ đợi tình hình địa chính trị sáng tỏ.

Phân hóa chính sách Fed Mỹ gia tăng.Cuộc họp lãi suất tháng 4 giữ nguyên lãi suất, nhưng số phiếu phản đối nội bộ đạt bốn, cao nhất kể từ tháng 10/1992. Tại họp báo, Powell thừa nhận thiếu tiến triển thêm về lạm phát nhưng loại trừ rõ ràng khả năng tăng lãi suất, phần nào xoa dịu lo ngại thị trường về việc thắt chặt leo thang. Trong khi đó, GDP quý I của Mỹ tăng trưởng hàng năm hóa đạt 2,0%, phục hồi đáng kể so với mức 0,5% trước đó, dù chi tiêu tiêu dùng chậm lại; PMI sản xuất ISM tháng 4 đạt 52,7%, nhưng chỉ số phụ việc làm suy yếu. Bức tranh tổng thể thể hiện "tăng trưởng ôn hòa kèm lạm phát gia tăng," kỳ vọng cắt giảm lãi suất trong năm hạ nhiệt, và giá đồng tiếp tục chịu áp lực giảm.

Ma sát thương mại Mỹ-EU leo thang.Ngày 4/5, Trump tuyên bố do EU không thực hiện thỏa thuận thương mại song phương đã đạt được, Mỹ sẽ áp thuế bổ sung lên ô tô và xe tải nhập khẩu từ EU vào tuần tới, nâng mức thuế lên 25%. Là phân khúc tiêu thụ cuối cùng quan trọng trong chuỗi ngành đồng, việc tăng thuế sẽ trực tiếp kìm hãm xuất khẩu ô tô châu Âu và nhu cầu đồng trong chuỗi ngành ô tô toàn cầu.

II. Cơ bản

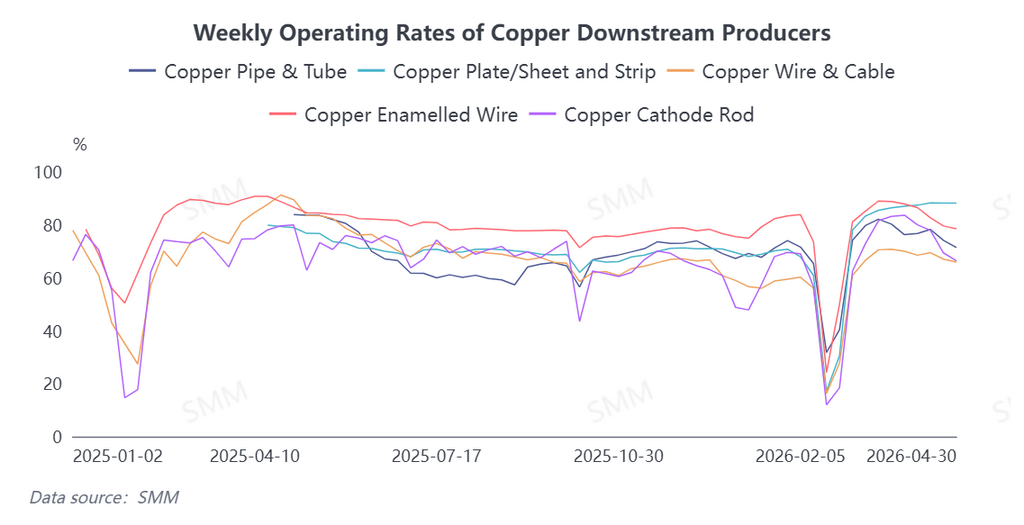

Phía cung, cả LME và COMEX đều ở cấu trúc Contango trước kỳ nghỉ, tồn kho vẫn ở mức cao tương đối so với lịch sử. Tuy nhiên, tồn kho xã hội tại thị trường Trung Quốc tiếp tục giảm, tạo hỗ trợ đáy cho giá đồng. Phía cầu, theo khảo sát SMM, doanh nghiệp hạ nguồn có sự phân hóa trong sắp xếp nghỉ lễ.Doanh nghiệp thanh đồng cathode ghi nhận đơn hàng mới giảm trước kỳ nghỉ, ý muốn tích trữ kém và nhu cầu nhìn chung yếu; thời gian nghỉ Lễ Lao động trung bình năm nay là 1,33 ngày, tăng 0,16 ngày so với cùng kỳ. Hầu hết doanh nghiệp thanh đồng thứ cấp không nghỉ lễ báo cáo thời gian tương đương năm 2025, nhưng một số doanh nghiệp vốn dự định nghỉ lễ đã áp dụng ngừng sản xuất hoàn toàn năm nay để đối phó với thách thức chứng từ tài chính thuế và áp lực nguồn nguyên liệu. Doanh nghiệp dây và cáp phần lớn tiếp tục thông lệ các năm trước duy trì sản xuất trong kỳ nghỉ, trong khi một số chọn ngừng sản xuất do đơn hàng suy yếu nhằm giảm áp lực tồn kho thành phẩm. Chịu ảnh hưởng từ giá đồng cao, doanh nghiệp dây và cáp áp dụng mua sắm thận trọng theo nhu cầu. Ngoài ra, đơn hàng lưới điện giảm do việc mua sắm tập trung trước đó đã kéo trước một phần nhu cầu. Hầu hết doanh nghiệp dây tráng men tiến hành bảo trì thiết bị dựa trên tình hình đơn hàng, giảm tải vận hành tổng thể; số doanh nghiệp chọn ngừng sản xuất trong kỳ nghỉ do đơn hàng suy yếu kéo dài tăng đáng kể so với cùng kỳ. Nhu cầu tiêu dùng cuối phân hóa: nhu cầu trong lĩnh vực lưu trữ năng lượng, năng lượng mới và các ngành khác vẫn mạnh mẽ, ngành xây dựng phục hồi nhẹ khi bước vào mùa cao điểm xây dựng, trong khi nhu cầu trong lĩnh vực điện gia dụng như điều hòa không khí và lĩnh vực lưới điện sắp bước vào mùa thấp điểm.

Nhìn về tháng 5, góc độ vĩ mô vẫn tập trung vào hướng đi của căng thẳng Mỹ-Iran.Mặc dù tín hiệu đàm phán liên tục được phát đi, vấn đề eo biển Hormuz vẫn chưa được giải quyết và sự bất định của thị trường vẫn tồn tại. Đồng thời, cần tiếp tục theo dõi dữ liệu kinh tế Mỹ công bố và tác động đến kỳ vọng thị trường về quyết định lãi suất của Fed. Về cơ bản, tiêu thụ có thể bước vào mùa thấp điểm trong tháng 5. Xu hướng đơn hàng suy yếu và tỷ lệ hoạt động giảm tại các doanh nghiệp hạ nguồn như doanh nghiệp thanh đồng cathode và dây tráng men sẽ khó đảo ngược trong ngắn hạn. Tiêu thụ cuối nhìn chung vẫn yếu ngoài các điểm sáng cơ cấu như năng lượng mới, và nhu cầu dự kiến sẽ giảm. Tuy nhiên, đáng chú ý là phía cung dự kiến sẽ thắt chặt. Một mặt, việc thực thi chính sách hạn chế xuất khẩu axit sulfuric từ Trung Quốc sau tháng 5 có thể làm trầm trọng thêm tình trạng thiếu hụt nguồn cung axit sulfuric ngoài Trung Quốc, từ đó ảnh hưởng đến công suất luyện kim thủy luyện. Mặt khác, các nhà máy luyện kim toàn cầu cũng sẽ bước vào giai đoạn bảo trì tập trung, và lo ngại thiếu hụt nguồn cung sẽ hỗ trợ tăng giá cho giá đồng.Nhìn chung, giá đồng dự kiến có dư địa tăng hạn chế trong ngắn hạn sau kỳ nghỉ, cần chú ý đến ngưỡng hỗ trợ tại các mức thấp trước đó phía dưới.