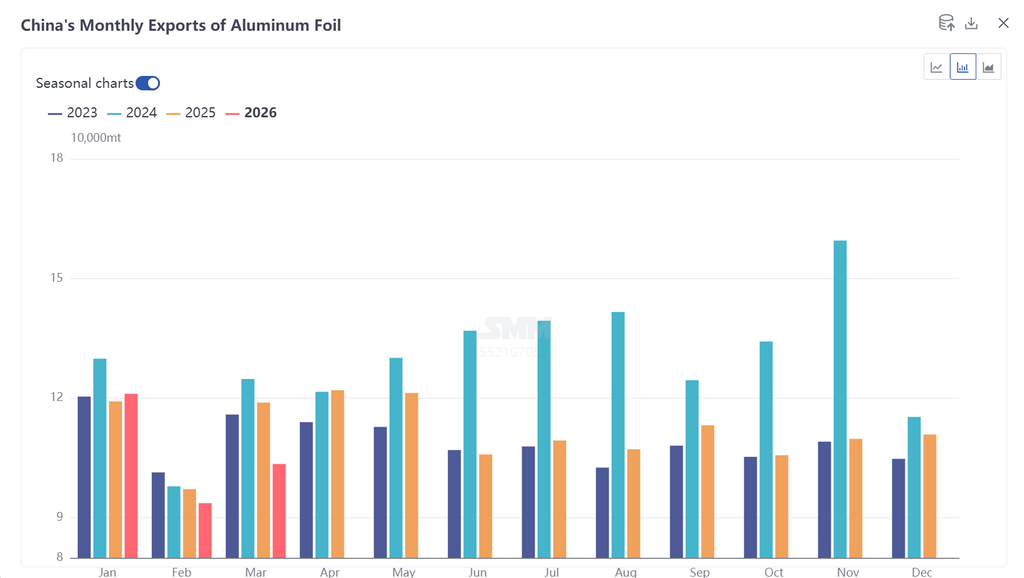

According to customs data, China's aluminum foil (tariff codes 76071110, 76071120, 76071190, 76071900, 76072000) total exports in March 2026 reached 103,500 mt, up 10% MoM but down 13% YoY. The share of exports to the UAE plunged from 6.8% in January-February to 2.5% in March, with the Middle East trade chain nearly severed.

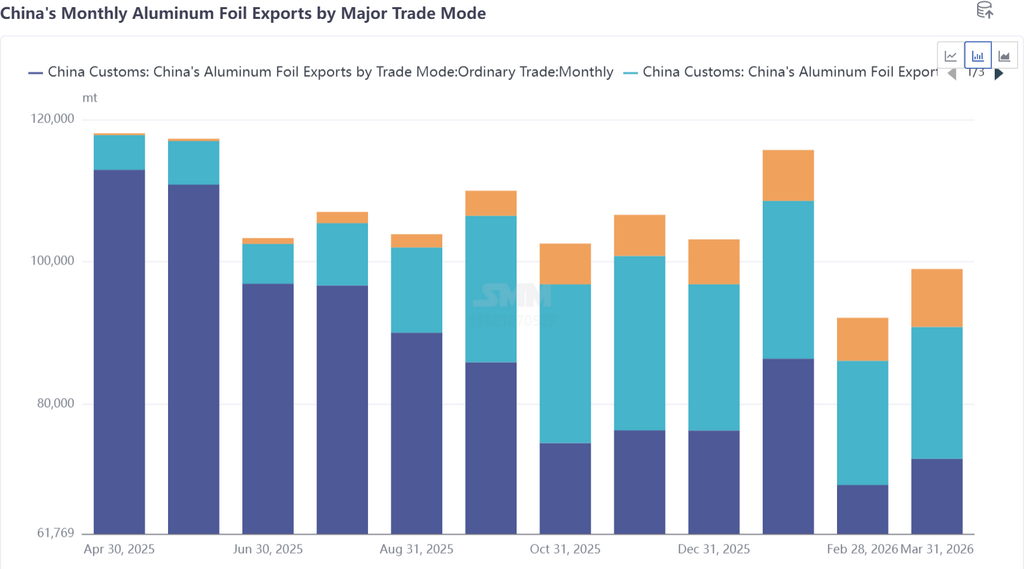

Trade mode: In March 2026, China's aluminum foil exports via processing trade with imported materials were approximately 18,500 mt, accounting for about 17.8%; exports via processing trade with supplied materials were approximately 8,000 mt, accounting for 7.7%.

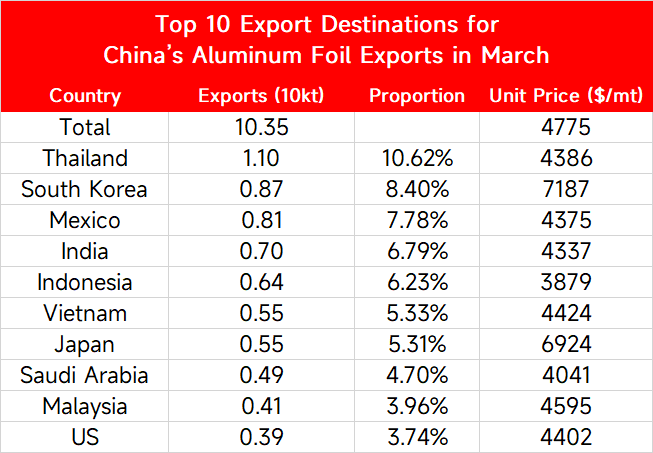

By country, the top 5 destinations for China's aluminum foil exports in March 2026 were Thailand (11,000 mt, 10.62%), South Korea (8,700 mt, 8.4%), Mexico (8,100 mt, 7.78%), India (7,000 mt, 6.8%), and Indonesia (0.64 mt, 6.2%), with the remaining countries accounting for approximately 60% in total.

Since March, the outbreak of the Israel-Iran conflict and the sharp deterioration of the Strait of Hormuz situation have become the most direct shock affecting March and subsequent exports. According to an SMM survey, export schedules of China's aluminum foil enterprises have extended to late June through July, with capacity essentially fully booked. There are two core reasons: first, some double zero foil production lines have shifted to higher-margin power battery foil, creating a gap in traditional packaging foil supply; second, overseas clients, concerned about prolonged strait blockade leading to global aluminum supply tightening, have placed orders in advance to secure supplies. These factors have jointly pushed double zero plain pouch export processing fees to a historically relatively high level of $1,000-1,200/mt. However, feedback suggests that high processing fees themselves have been slowing the rate of additional orders from some clients. Overall, in Q2 2026, China's aluminum foil exports, driven by both the export rush and capacity mismatch, will exhibit a phase of prosperity characterized by full production schedules and elevated processing fees. However, it is worth noting that this round of growth has pronounced geopolitical drivers, and its sustainability remains questionable. Whether full-year exports can recover the ground lost from the 13.4% YoY decline in 2025 (approximately 150,000 mt in incremental volume) remains highly uncertain.