Quặng Niken

Tuần này, giá quặng niken nội địa tại Indonesia đã tăng. Nửa cuối tháng 4, giá chuẩn quặng niken Indonesia (HPM) được ấn định ở mức 16.933,6 USD/tấn khô, giảm 0,93% so với tháng trước. Theo dữ liệu phụ phí quặng niken Indonesia của SMM, mức phụ phí trung bình cho quặng niken laterit hàm lượng 1,4%, 1,5% và 1,6% lần lượt ở mức 40 USD, 44 USD và 44,5 USD/tấn ướt. Trong đó, giá giao tại nhà máy nội địa cho quặng niken hàm lượng 1,6% là 69,2–80,2 USD/tấn ướt. Phụ phí tăng mạnh trong tháng này phản ánh nhu cầu bổ sung tồn kho của các nhà máy luyện kim và kỳ vọng bi quan về việc cắt giảm hạn ngạch RKAB. Đồng thời, giá giao quặng thủy luyện hàm lượng 1,2% cũng tăng lên 27–33 USD/tấn ướt. Mặc dù công thức HPM đã được điều chỉnh đáng kể, hiện tích hợp hàm lượng sản phẩm phụ như sắt, coban và crom, thị trường vẫn đang trong giai đoạn chuyển đổi (chế độ "chờ đợi và quan sát"). Do công thức mới làm tăng mạnh giá cơ sở tính toán cho cả quặng saprolit và limonit, hầu hết các nhà máy luyện kim đang phản đối và từ chối các khái niệm phụ phí này cho đến cuối tháng 4. Hiện tại, họ ưu tiên cơ chế định giá "HPM cũ + Phụ phí" để duy trì ổn định chi phí. Do tính đột ngột của việc ban hành quy định này, các nhà máy luyện kim có rất ít thời gian để điều chỉnh cơ chế định giá nội bộ hoặc đàm phán lại cấu trúc phụ phí. Do đó, các giao dịch trên thị trường vẫn ổn định, chưa có giao dịch mới nào được báo cáo sử dụng công thức đa nguyên tố cập nhật.

- Quặng hỏa luyện:

Từ góc độ cung cầu cơ bản, các trung tâm khai thác chính bao gồm Morowali và Konawe đã chuyển sang điều kiện chủ yếu nhiều mây trong tuần này, giảm bớt so với các đợt mưa lớn liên tục trước đó. Tuy nhiên, độ ẩm địa phương dự kiến vẫn tiệm cận mức bão hòa 99%. Dưới tác động kết hợp của sóng khí quyển hoạt động mạnh và lớp mây dày đặc kéo dài, việc thiếu ánh nắng trực tiếp cùng môi trường cực kỳ ẩm ướt sẽ tiếp tục hạn chế hiệu suất phơi khô quặng của các mỏ lộ thiên. Tốc độ bay hơi chậm này tiếp tục cản trở hoạt động logistics và vận chuyển, làm trầm trọng thêm những khó khăn vận hành trong quản lý độ ẩm cao khi vận chuyển quặng nickel laterit.

Hơn nữa, thị trường đang đối mặt với xu hướng suy giảm rõ rệt về hàm lượng quặng, mặc dù hàm lượng saprolite ở khu vực Sulawesi vẫn tương đối cao hơn so với Halmahera. Trong khi một số nhà máy luyện NPI đã bắt đầu chấp nhận quặng có hàm lượng 1,45% trở xuống, nguồn cung quặng cho luyện kim hỏa luyện vẫn đặc biệt khan hiếm trong tháng 4.

- Quặng cho luyện kim thủy luyện

Ngoài ra, các giao dịch quặng limonite diễn ra thưa thớt. Sau đợt tăng giá mạnh của quặng luyện kim hỏa luyện, giá limonite cũng nhích lên, điều mà các nhà khai thác hy vọng sẽ kích thích doanh số. Tuy nhiên, một chênh lệch giá đáng kể đã xuất hiện: giá HPM mới tính toán cho limonite hiện đã vượt qua giá thị trường CIF cuối cùng. Do đó, mặc dù các nhà khai thác tiếp tục đẩy giá lên cao, hầu hết các nhà máy luyện đều đàm phán quyết liệt để giữ giá mua dưới mức HPM mới, từ đó giữ giá giao dịch limonite thực tế ổn định ở mức trước đó.

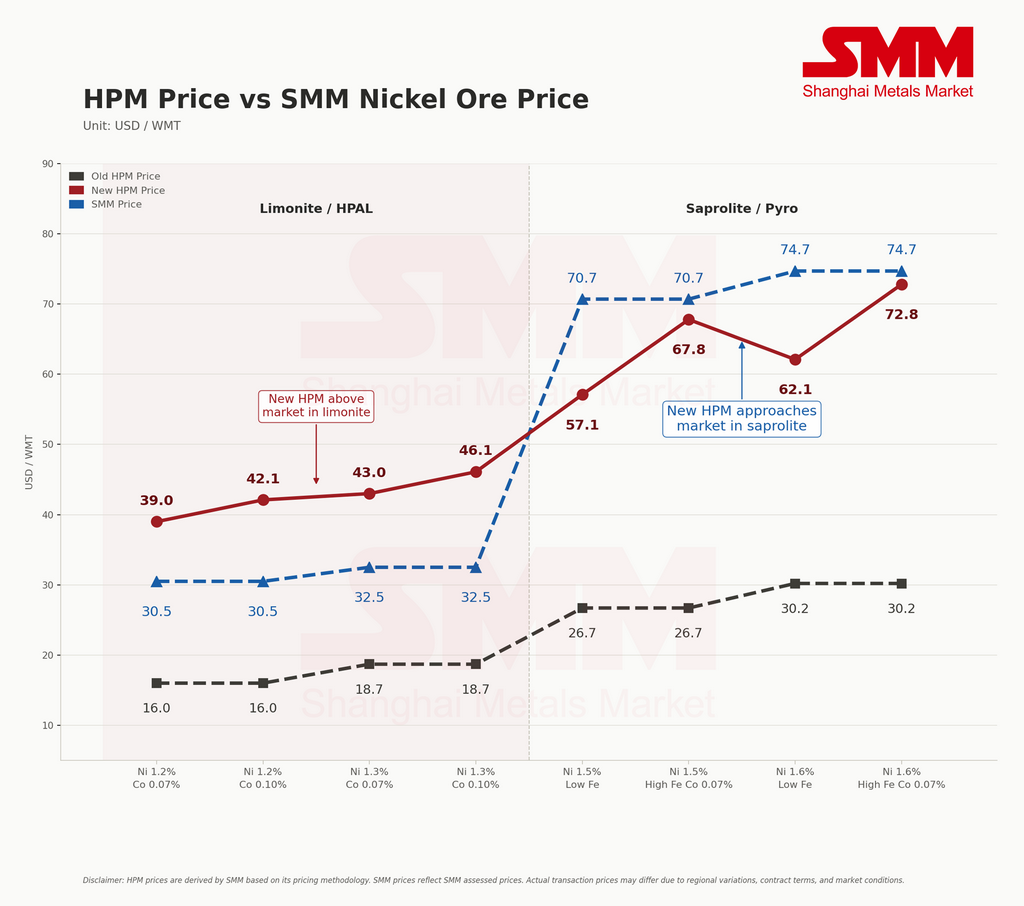

Triển vọng giá HPM (Giả định nội bộ của SMM)

Với ba nguyên tố phụ phẩm hiện được đưa vào công thức định giá quặng nickel, chúng tôi nhận thấy tác động phân hóa đối với tính toán cho saprolite và limonite. Nhìn chung, giá limonite theo HPM mới đang cao hơn giá thị trường do SMM đánh giá. Ngược lại, trong khi giá thị trường hiện hành của saprolite vẫn cao hơn mức chuẩn chính thức, khoảng cách giữa hai mức giá đang thu hẹp dần.

Triển vọng quy định & hạn ngạch (RKAB)

Tổng Giám đốc Khoáng sản và Than đá Tri Winarno cho biết Bộ Năng lượng và Tài nguyên Khoáng sản (ESDM) vẫn đang tích cực xử lý Kế hoạch Công tác và Ngân sách năm 2026 (RKAB) cho các mặt hàng khoáng sản và than đá, với tiến độ phê duyệt đạt khoảng 90% vào giữa tháng 4. Hiện tại, một số doanh nghiệp khai thác đã nhận được thông báo sơ bộ từ chính phủ về các chỉ tiêu hạn ngạch mới nhất, nhưng phần lớn vẫn chưa có dữ liệu phê duyệt chính thức cuối cùng. Thị trường nhìn chung kỳ vọng hạn ngạch RKAB 2026 sẽ được chính thức hoàn tất vào cuối tháng 4.

Về phía cầu, do sự bất định về nguồn tài nguyên mà các nhà máy luyện tại Indonesia phải đối mặt và khó khăn kéo dài trong việc đảm bảo nguồn quặng nickel hàm lượng cao, giá đã duy trì diễn biến mạnh. Để đảm bảo nguồn cung nguyên liệu ổn định, một số nhà máy luyện kim thậm chí đã bắt đầu đề xuất tăng phí thưởng thương mại và phí bảo hiểm để đảm bảo nguồn hàng.

Niken thô (NPI)

"Thị trường NPI hàm lượng cao giảm trước khi phục hồi trong bối cảnh nhu cầu hồi phục và tác động từ chính sách HPM mới của Indonesia"

Giá trung bình NPI 10-12% của SMM giảm 5,15 NDT/đơn vị niken so với tuần trước, xuống còn 1.085,4 NDT/đơn vị niken (giá xuất xưởng, đã bao gồm thuế), trong khi chỉ số FOB NPI Indonesia tăng 1,5 USD/đơn vị niken, đạt trung bình 138,51 USD/đơn vị niken. Điều kiện thị trường NPI hàm lượng cao nhìn chung duy trì ổn định.

Tuần này, thị trường NPI hàm lượng cao thể hiện xu hướng "giảm trước rồi phục hồi". Đầu tuần, giá giảm nhẹ do nhu cầu tiêu thụ cuối nguồn trì trệ. Tuy nhiên, sau đó được thúc đẩy bởi nhiều yếu tố thuận lợi, hoạt động thị trường tăng đáng kể và mức giá trung tâm dần dịch chuyển lên. Giữa tuần, chính sách HPM mới của Indonesia được triển khai, khiến giá HPM quặng niken tăng mạnh. Điều này củng cố quyết tâm giữ giá của các nhà máy luyện kim thượng nguồn. Đồng thời, được hỗ trợ bởi đà tăng liên tục của giá niken, ý muốn chống đỡ giá và mua hàng của các thương nhân cũng được kích thích.

Về phía cầu, khi thị trường kỳ hạn tăng mạnh, giá thép không gỉ giao ngay cũng tăng theo, giá thép phế liệu cũng đi lên. Với biên lợi nhuận hạ nguồn và hiệu quả kinh tế phục hồi, mức chấp nhận giá NPI hàm lượng cao của các nhà máy thép tăng đồng bộ, dẫn đến hoạt động giao dịch thị trường tăng trưởng so với tháng trước. Tóm lại, được hỗ trợ bởi chi phí và sự phục hồi hoạt động thị trường, mức giá trung tâm NPI hàm lượng cao đã dịch chuyển lên cao hơn. Nhìn về phía trước, với sự hỗ trợ từ chi phí và cân bằng cung cầu thắt chặt, giá NPI hàm lượng cao dự kiến sẽ tiếp tục xu hướng tăng.

![[SMM Flash News] Giá cước vận tải quặng niken Philippines giảm mạnh, tuyến Surigao-Lianyungang giảm xuống $13,5-14/wmt](https://imgqn.smm.cn/usercenter/vSdFt20251217171732.jpg)