Tin SMM ngày 13/4:

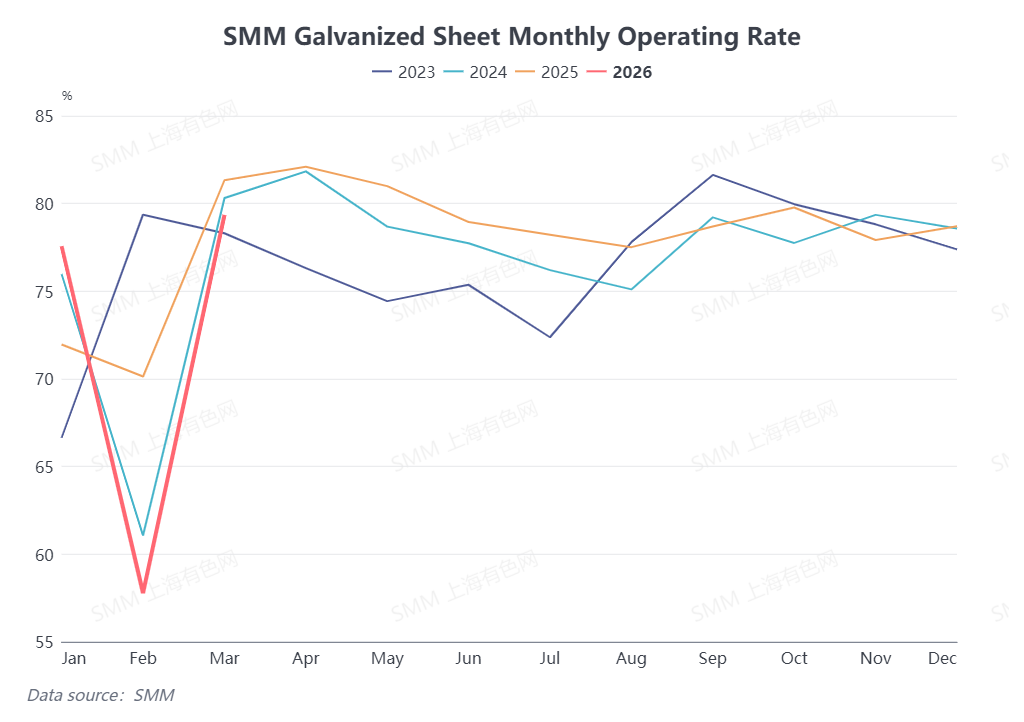

Quý I đã kết thúc. Từ góc độ đơn hàng, đơn hàng tháng 1 suy yếu theo mùa, tháng 2 trùng với kỳ nghỉ Tết Nguyên đán khi hầu hết các nhà sản xuất tôn mạ kẽm tại Trung Quốc nghỉ lễ, và mặc dù các doanh nghiệp tôn mạ kẽm dần khôi phục sản xuất vào tháng 3, tỷ lệ sử dụng công suất tổng thể vẫn thấp hơn so với cùng kỳ năm ngoái. Đơn hàng tôn mạ kẽm quý I tại Trung Quốc khá ảm đạm. Kỳ vọng cho quý II như thế nào?

Ngành xây dựng. Trong quý I năm nay, số liệu lũy kế khởi công mới và hoàn thành bất động sản so với cùng kỳ tiếp tục duy trì tăng trưởng âm, nhu cầu sụt giảm liên quan tiếp tục kéo giảm đơn hàng tôn mạ kẽm xây dựng tại Trung Quốc. Được biết, đơn hàng từ tháng 1 đến tháng 2 kém do mùa thấp điểm và kỳ nghỉ lễ. Tháng 3, các dự án của người dùng cuối tại Trung Quốc dần triển khai, nhưng tốc độ phục hồi tổng thể chậm, đơn hàng tôn mạ kẽm tháng 3 kém hơn so với năm ngoái. Nhìn về quý II, tiêu thụ nội địa tháng 4 dự kiến tiếp tục cải thiện so với tháng 3 với nhiều đơn hàng tôn xây dựng hơn, trong khi tháng 6 là mùa mưa mai điển hình. Tổng thể đơn hàng quý II dự kiến tăng trước rồi giảm sau.

Ngành ô tô. Theo dữ liệu của CAAM, từ tháng 1 đến tháng 3/2026, sản lượng và doanh số ô tô Trung Quốc đạt lần lượt 7,039 triệu xe và 7,048 triệu xe, giảm lần lượt 6,9% và 5,6% so với cùng kỳ. Trong đó, sản lượng và doanh số xe năng lượng mới giảm lần lượt 6,8% và 3,7% so với cùng kỳ, doanh số xe năng lượng mới chiếm 42% tổng doanh số xe mới. Sản lượng và doanh số ô tô quý I kém hơn so với cùng kỳ năm ngoái, đồng thời ảnh hưởng đến nhu cầu tôn ô tô liên quan. Nhìn về quý II, dữ liệu sản lượng và doanh số ô tô thường tương đối ổn định trong quý II, đơn hàng tôn ô tô liên quan dự kiến vận hành ổn định.

Ngành gia dụng. Từ tháng 1 đến tháng 2/2026, sản lượng lũy kế tủ lạnh gia dụng tăng 6,5% so với cùng kỳ, điều hòa tăng 0,7% so với cùng kỳ, máy giặt giảm 0,8% so với cùng kỳ. Sản xuất gia dụng quý I có kết quả trái chiều, hiệu suất đơn hàng tổng thể ở mức trung bình, nhu cầu tiêu dùng cuối tiếp tục thúc đẩy đơn hàng tôn mạ kẽm. Thông thường, tháng 4 đến tháng 5 vẫn là mùa cao điểm sản xuất và tiêu thụ gia dụng tại Trung Quốc, nhưng mùa hè đến sau đó dự kiến ảnh hưởng đến sản xuất của các nhà máy gia dụng. Đơn hàng tôn mạ kẽm gia dụng quý II dự kiến mạnh trước rồi yếu sau.

Phía xuất khẩu. Theo số liệu của Tổng cục Hải quan, xuất khẩu tôn mạ kẽm tháng 1/2026 đạt 926.600 tấn, tháng 2 đạt 1,1677 triệu tấn. Xuất khẩu lũy kế từ tháng 1 đến tháng 2 đạt tổng cộng 2,0942 triệu tấn, giảm 0,14% so với cùng kỳ năm trước. Tổng xuất khẩu tôn mạ kẽm của Trung Quốc từ tháng 1 đến tháng 2 năm nay về cơ bản ngang bằng với năm ngoái. Đối với quý II, mặc dù căng thẳng Trung Đông gần đây đã ảnh hưởng đến một phần nhu cầu xuất khẩu, với các đơn hàng liên quan trong tháng 3 và tháng 4 bị tác động, nhưng xét đến nhu cầu tại Đông Nam Á vẫn mạnh mẽ, xuất khẩu tôn mạ kẽm quý II dự kiến sẽ không sụt giảm đáng kể.

(Thông tin trên dựa trên thu thập thị trường và đánh giá tổng hợp của nhóm nghiên cứu SMM. Thông tin trong bài viết này chỉ mang tính tham khảo. Bài viết không cấu thành lời khuyên trực tiếp cho nghiên cứu và ra quyết định đầu tư. Khách hàng nên đưa ra quyết định thận trọng và không nên thay thế đánh giá độc lập của mình bằng thông tin này. Mọi quyết định của khách hàng không liên quan đến SMM.)

![Biến động địa chính trị kết hợp với gián đoạn thương mại đẩy giá trên SHFE và LME tăng cao [Bình luận thị trường SMM - Nhận định giá kẽm tuần]](https://imgqn.smm.cn/usercenter/nGzXc20251217171754.jpg)

![Các nhà máy luyện kim không cắt giảm sản lượng đáng kể trong tháng 5, phí gia công tinh quặng kẽm tiếp tục giảm [SMM Báo cáo tuần tinh quặng kẽm]](https://imgqn.smm.cn/usercenter/PEqzX20251217171755.jpg)

![Sản lượng kẽm oxit tương đối ổn định nhưng biên lợi nhuận doanh nghiệp thu hẹp [SMM Báo cáo tuần kẽm oxit]](https://imgqn.smm.cn/usercenter/EviJV20251217171754.jpg)